Answered step by step

Verified Expert Solution

Question

1 Approved Answer

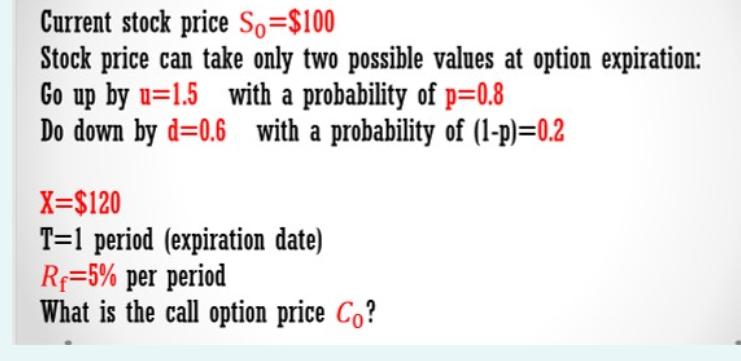

Current stock price So=$100 Stock price can take only two possible values at option expiration: Go up by u=1.5 with a probability of p=0.8

Current stock price So=$100 Stock price can take only two possible values at option expiration: Go up by u=1.5 with a probability of p=0.8 Do down by d=0.6 with a probability of (1-p)=0.2 X=$120 T=1 period (expiration date) R=5% per period What is the call option price Co?

Step by Step Solution

★★★★★

3.48 Rating (155 Votes )

There are 3 Steps involved in it

Step: 1

1 Define the parameters Current stock price So 100 Upward movement factor u 15 Downw...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Statistics

Authors: Robert S. Witte, John S. Witte

10th Edition

9781118805350, 1118450531, 1118805356, 978-1118450536