Answered step by step

Verified Expert Solution

Question

1 Approved Answer

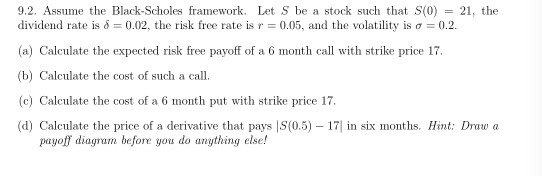

D pls 9.2. Assume the Black-Scholes framework. Let S be a stock such that S(0) = 21, the dividend rate is 8 = 0.02, the

D pls

9.2. Assume the Black-Scholes framework. Let S be a stock such that S(0) = 21, the dividend rate is 8 = 0.02, the risk free rate is r = 0.05, and the volatility is a = 0.2. (a) Calculate the expected risk free payoff of a 6 month call with strike price 17. (b) Calculate the cost of such a call. (c) Calculate the cost of a 6 month put with strike price 17. (d) Calculate the price of a derivative that pays S(0.5) - 17| in six months. Hint: Draw a payoff diagram before you do anything else! 9.2. Assume the Black-Scholes framework. Let S be a stock such that S(0) = 21, the dividend rate is 8 = 0.02, the risk free rate is r = 0.05, and the volatility is a = 0.2. (a) Calculate the expected risk free payoff of a 6 month call with strike price 17. (b) Calculate the cost of such a call. (c) Calculate the cost of a 6 month put with strike price 17. (d) Calculate the price of a derivative that pays S(0.5) - 17| in six months. Hint: Draw a payoff diagram before you do anything elseStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Times Guide To Finance For Non Financial Managers

Authors: Jo Haigh

1st Edition

0273756206, 978-0273756200