Answered step by step

Verified Expert Solution

Question

1 Approved Answer

d) What are multiple-element contracts and why do they pose revenue recognition problems for companies? Apple Inc.-Revenue Recognition Apple Inc. designs, manufactures, and markets personal

d) What are multiple-element contracts and why do they pose revenue recognition problems for companies?

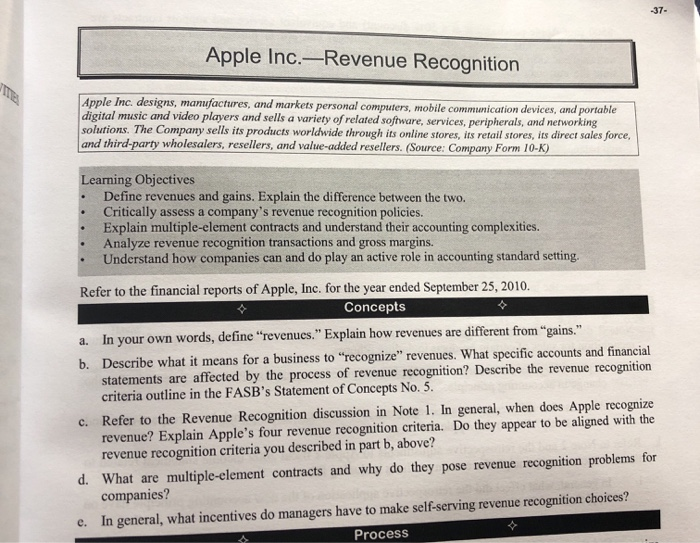

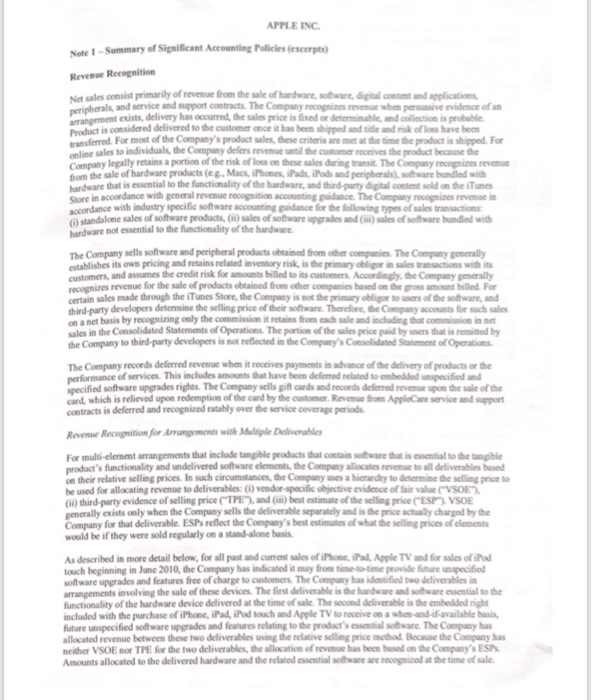

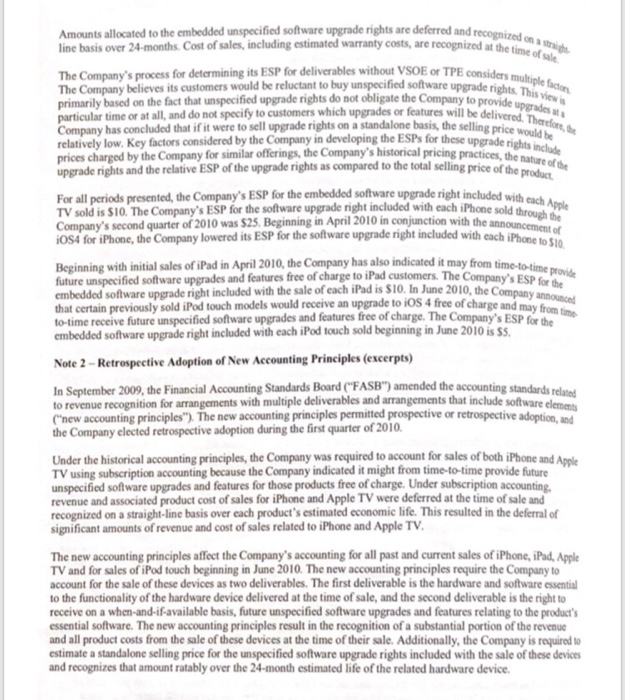

Apple Inc.-Revenue Recognition Apple Inc. designs, manufactures, and markets personal computers, mobile communication devices, and portable digital music and video players and sells a variety of related software, services, peripherals, and networking solutions. The Company sells its products worldwide through its online stores, its retail stores, its direct sales force, and third-party wholesalers, resellers, and value-added resellers. (Source: Company Form 10-K) Learning Objectives Define revenues and gains. Explain the difference between the two. Critically assess a company's revenue recognition policies. Explain multiple-element contracts and understand their accounting con Analyze revenue recognition transactions and gross margins. Understand how companies can and do play an active role in accounting standard setting. Refer to the financial reports of Apple, Inc. for the year ended September 25, 2010. Concepts a. In your own words, define "revenues." Explain how revenues are different from "gains." b. Describe what it means for a business to "recognize" revenues. What specific accounts and financial statements are affected by the process of revenue recognition? Describe the revenue recognition criteria outline in the FASB's Statement of Concepts No. 5. c. Refer to the Revenue Recognition discussion in Note 1. In general, when does Apple recognize revenue? Explain Apple's four revenue recognition criteria. Do they appear to be aligned with the revenue recognition criteria you described in part b, above? d. What are multiple-element contracts and why do they pose revenue recognition problems for companies? e. In general, what incentives do managers have to make self-serving revenue recognition choices? Process APPLE INC Note 1 - Summary of Significant Accounting Policies excerpts) Rere Recognition Na sales consist primarily of revenue from the sale of hardware, software, digital content and applications als and service and support contract. The Company recomes whene v e evidence of an rangement exists, delivery has occurred, the sales price is fixed or determinable, and collection is probable Product is considered delivered to the customer once it has been shipped and title and risk of loss have been ansferred. For most of the Company's product sales, these criteria are met at the time the product is shipped. For online sales to individuals, the Company defers revenue until the customer receives the product because the Company legally retains a portion of the risk of loss on these sales during transit. The Company recognizes revenue Gior the sale of hardware products (eg, Mac, iPhone, iPad, iPods and peripherals, software bundled with hardware that is essential to the functionality of the hardware, and third-party digital content sold on the iTunes Store in accordance with general revenue recognition accounting guidance. The Company recognizes revenue in accordance with industry specific software accounting guidance for the following types of sales transactions standalone sales of software products, (i) sales of software upgrades and sales of software bundled with hardware not essential to the functionality of the hardware The Company sells software and peripheral products obtained from other companies. The Company generally establishes its own pricing and retains related inventory risk is the primary obligor in sales transactions with its customers, and assumes the credit risk for amounts billed to its customers. Accordingly, the Company generally recognizes revenue for the sale of products obtained from other companies based on the gross amount billed. For certain sales made through the iTunes Store, the Company is not the primary obliger towers of the software, and third-party developers determine the selling price of their software. Therefore, the Company accounts for such sales on a net basis by recognizing only the commission it rains from each sale and including that commission in net sales in the Consolidated Statements of Operations. The portion of the sales price paid by users that is remitted by the Company to third-party developers is not reflected in the Company's Consolidated Statement of Operations The Company records deferred revenue when it receives payments in advance of the delivery of products or the performance of services. This includes amounts that have been deferred related to embedded unspecified and specified software upgrades rights. The Company sells gift cards and records deferred revenue upon the sale of the card, which is relieved upon redemption of the card by the customer Revenue from AppleCare service and support centracts is deferred and recognized atably over the service coverage periods Race Recognition for Arrangement with Multiple Deliverables For multi-clement arrangements that include tangible products that contain software that is essential to the tangible product's functionality and undelivered software clements, the Company allocates revenue to all deliverables based on their relative selling prices. In such circumstances, the Company uses a hierarchy to determine the selling price to be used for allocating revenue to deliverables vendor-specific objective evidence of value (VSOE (ii) third-party evidence of selling price (TPE) and (m) best estimate of the selling price C'ESP) VSOE generally exists only when the Company sells the deliverable separately and is the price actually charged by the Company for that deliverable. ESPs reflect the Company's best estimates of what the selling prices of elements would be if they were sold regularly on a stand-alone basis As described in more detail below, for all past and current sales of iPhone, iPad, Apple TV and for sales of iPod touch beginning in June 2010, the Company has indicated it may from time to time provide future specified software upgrades and features free of charge to customers. The Company has identified to deliverables in arrangements involving the sale of these devices. The first deliverable is the hardware and software essential to the functionality of the hardware device delivered at the time of sale. The second deliverable is the embedded right included with the purchase of iPhone, iPad, iPod touch and Apple TV t ives when ad-favailable basis future unspecified software upgrades and features relating to the products are. The Company has allocated revenue between these two deliverables using the relative selling price that Because the Company has neither VSOE nor TPE for the the deliverables, the allocation of revenue has been based on the Company's ESP Amounts allocated to the delivered hardware and the related essential software are o n e at the time of sale Amounts allocated to the embedded unspecified software upgrade rights are deferred and reco line basis over 24-months. Cost of sales, including estimated warranty costs, are recognized recognized on the ved at the time of sale sides multiple face de rights. This views to provide upgrades delivered. Therefore, The Company's process for determining its ESP for deliverables without VSOE or TPE conside The Company believes its customers would be reluctant to buy unspecified software upgrade rieh primarily based on the fact that unspecified upgrade rights do not obligate the Company to provide particular time or at all, and do not specify to customers which upgrades or features will be deli Company has concluded that if it were to sell upgrade rights on a standalone basis, the selline relatively low. Key factors considered by the Company in developing the ESPs for these upgrade i prices charged by the Company for similar offerings, the Company's historical pricing practices th upgrade rights and the relative ESP of the upgrade rights as compared to the total selling price of the sis, the selling price would be upgrade rights include actices, the nature of the selling price of the product ided with each Apple hehe sold through the For all periods presented, the Company's ESP for the embedded software upgrade right included with TV sold is $10. The Company's ESP for the software upgrade night included with each iPhone sold Company's second quarter of 2010 was $25. Beginning in April 2010 in conjunction with the iOS4 for iPhone, the Company lowered its ESP for the software upgrade right included with each i action with the announcement of ded with cach iPhone to $10 ay from time to time provide Beginning with initial sales of iPad in April 2010, the Company has also indicated it may from time future unspecified software upgrades and features free of charge to iPad customers. The Company's ESP embedded software upgrade right included with the sale of each iPad is Slo. In June 2010, the Come that certain previously sold iPod touch models would receive an upgrade to iOS 4 free of charge and to-time receive future unspecified software upgrades and features free of charge. The Company's ESP embedded software upgrade right included with each iPod touch sold beginning in June 2010 is SS 2010, the Company announ of charge and may from time Note 2 - Retrospective Adoption of New Accounting Principles (excerpts) In September 2009, the Financial Accounting Standards Board ("FASB") amended the accounting standarde to revenue recognition for arrangements with multiple deliverables and arrangements that include software ("new accounting principles"). The new accounting principles permitted prospective or retrospective adoption the Company elected retrospective adoption during the first quarter of 2010. Under the historical accounting principles, the Company was required to account for sales of both iPhone and Apple TV using subscription accounting because the Company indicated it might from time to time provide future unspecified software upgrades and features for those products free of charge. Under subscription accounting, revenue and associated product cost of sales for iPhone and Apple TV were deferred at the time of sale and recognized on a straight-line basis over each product's estimated economic life. This resulted in the deferral of significant amounts of revenue and cost of sales related to iPhone and Apple TV. The new accounting principles affect the Company's accounting for all past and current sales of iPhone, iPad, Apple TV and for sales of iPod touch beginning in June 2010. The new accounting principles require the Company to account for the sale of these devices as two deliverables. The first deliverable is the hardware and software essential to the functionality of the hardware device delivered at the time of sale, and the second deliverable is the right to receive on a when-and-if available basis, future unspecified software upgrades and features relating to the product's essential software. The new accounting principles result in the recognition of a substantial portion of the revenue and all product costs from the sale of these devices at the time of their sale. Additionally, the Company is required to estimate a standalone selling price for the unspecified software upgrade rights included with the sale of these devices and recognizes that amount ratably over the 24-month estimated life of the related hardware device Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Security Risk Handbook Assess Survey Audit

Authors: Charles Swanson

1st Edition

1032030356, 978-1032030357