Answered step by step

Verified Expert Solution

Question

1 Approved Answer

d. What would happen to Daniella's group life insurance if she leaves her present job? (Select the best choice below.) A. If Daniella left her

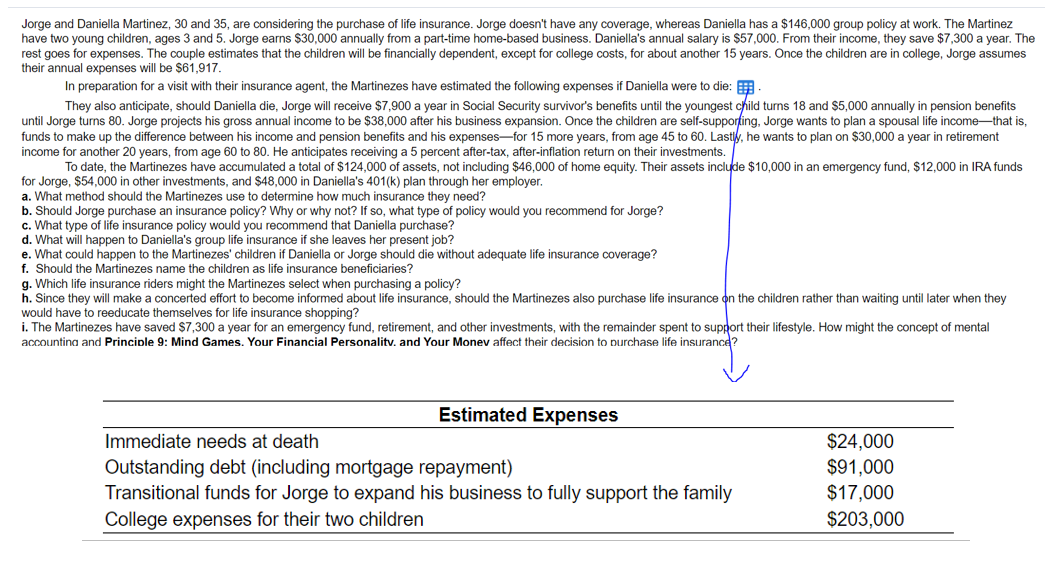

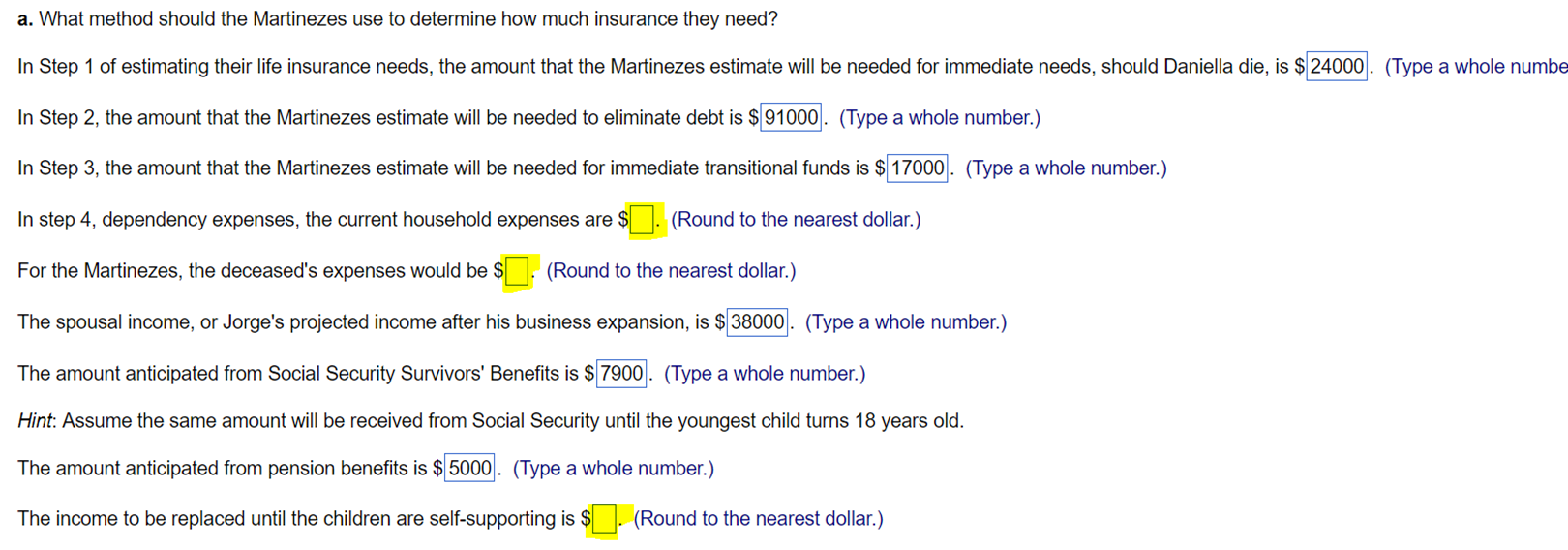

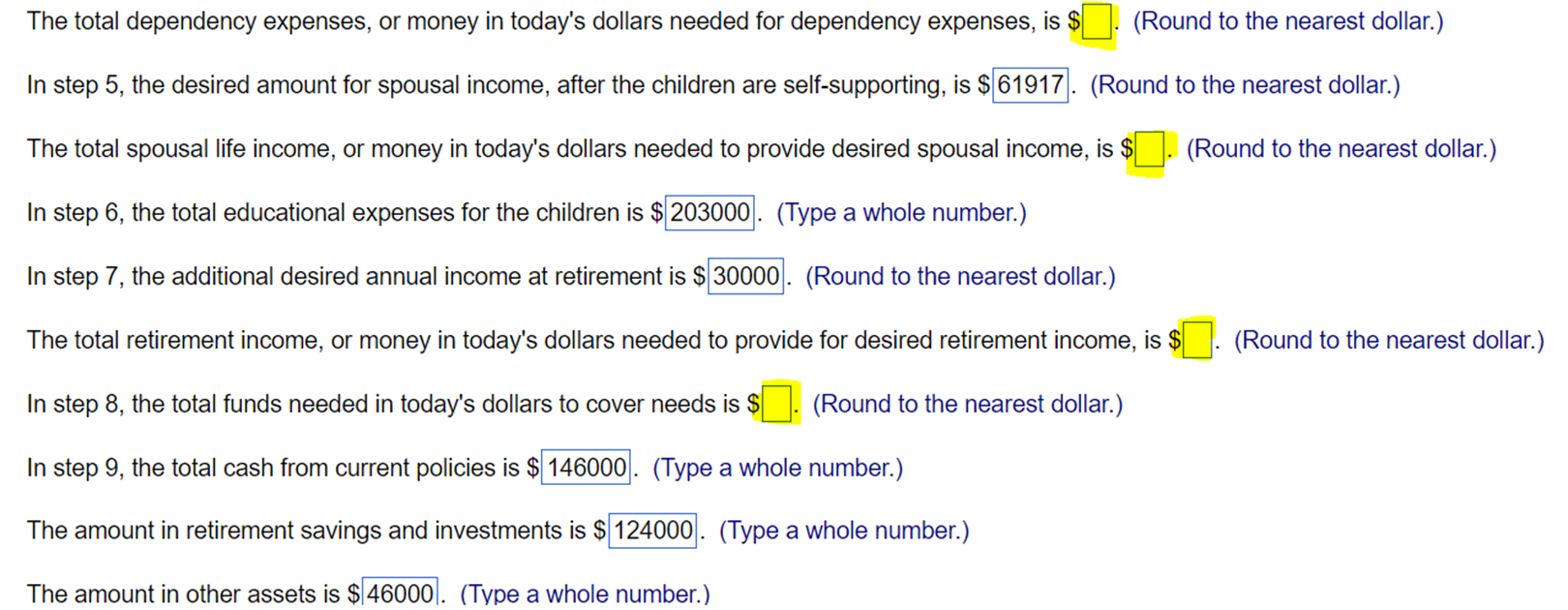

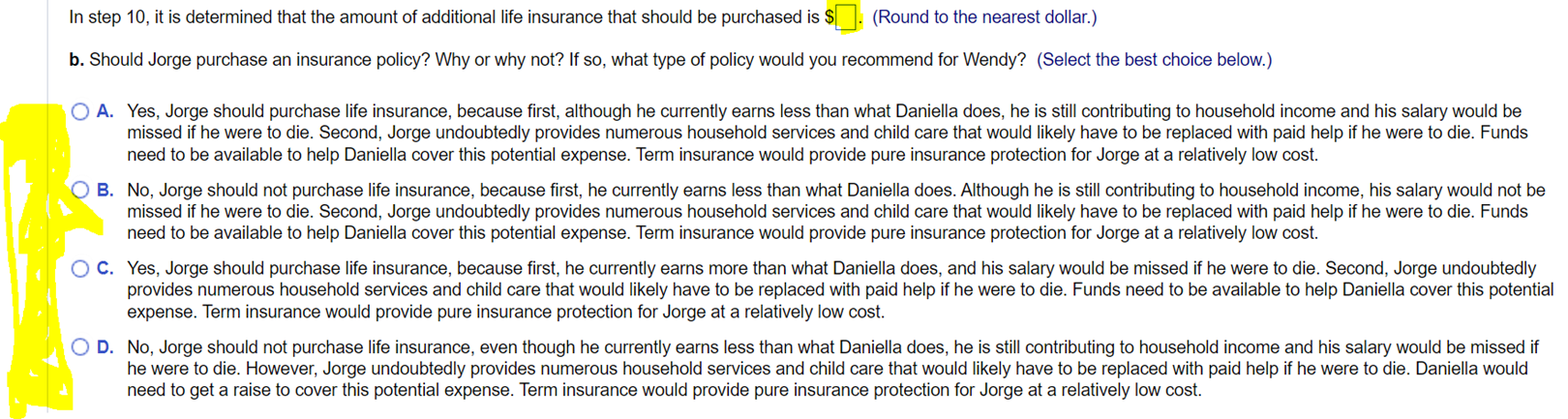

d. What would happen to Daniella's group life insurance if she leaves her present job? (Select the best choice below.) A. If Daniella left her present job, her employer-provided life insurance would continue until she found a new job with a group policy. This risk is a reason to have an emplyer-provided life insurance policy to avoid the greater risk of death occurring with no life insurance protection. B. If Daniella left her present job, her employer-provided life insurance would end. This risk is a reason to have a risk pooling policy to avoid the greater risk of death occurring with no life insurance protection. C. If Daniella left her present job, her employer-provided life insurance would end. This risk is a reason to have a renewable or convertible term policy to avoid the greater risk of death occurring with no life insurance protection. D. If Daniella left her present job, her employer-provided life insurance would continue until her death. This is a reason not to have a renewable or convertible term policy, because it would be spending more money than necessary. g. Which life insurance riders might the Martinezes select when purchasing a policy? Life insurance riders the Martinezes might select when purchasing a policy are: (Select all the choices that apply.) A. a waiver of premium for disability rider. B. a change of policy rider. C. a living benefits rider. D. a guaranteed insurability rider. E. a cost of living adjustment (COLA) rider. F. a lump-sum settlement rider. c. What type of life insurance policy would you recommend that Daniella purchase? (Select the best choice below.) A. Daniella should purchase a universal life insurance policy. It will provide the most protection for the least amount of premium cost. Since Daniella needs to purchase about $300,000 o additional insurance, she needs to find an affordable policy. B. Daniella should purchase a variable life insurance policy. It will provide the most protection for the least amount of premium cost. Since Daniella needs to purchase about $300,000 of additional insurance, she needs to find an affordable policy. C. Daniella should purchase a whole life insurance policy. It will provide the most protection for the least amount of premium cost. Since Daniella needs to purchase about $300,000 of additional insurance, she needs to find an affordable policy. D. Daniella should purchase a term insurance policy. It will provide the most protection for the least amount of premium cost. Since FranDaniellak needs to purchase about $300,000 of additional insurance, she needs to find an affordable policy. a. What method should the Martinezes use to determine how much insurance they need? In Step 1 of estimating their life insurance needs, the amount that the Martinezes estimate will be needed for immediate needs, should Daniella die, is $ (Type a whole numbe In Step 2, the amount that the Martinezes estimate will be needed to eliminate debt is $ (Type a whole number.) In Step 3, the amount that the Martinezes estimate will be needed for immediate transitional funds is $ (Type a whole number.) In step 4, dependency expenses, the current household expenses are $ (Round to the nearest dollar.) For the Martinezes, the deceased's expenses would be (Round to the nearest dollar.) The spousal income, or Jorge's projected income after his business expansion, is $ (Type a whole number.) The amount anticipated from Social Security Survivors' Benefits is (Type a whole number.) Hint: Assume the same amount will be received from Social Security until the youngest child turns 18 years old. The amount anticipated from pension benefits is ? (Type a whole number.) The income to be replaced until the children are self-supporting is (Round to the nearest dollar.) In step 10, it is determined that the amount of additional life insurance that should be purchased is (Round to the nearest dollar.) b. Should Jorge purchase an insurance policy? Why or why not? If so, what type of policy would you recommend for Wendy? (Select the best choice below.) A. Yes, Jorge should purchase life insurance, because first, although he currently earns less than what Daniella does, he is still contributing to household income and his salary would be missed if he were to die. Second, Jorge undoubtedly provides numerous household services and child care that would likely have to be replaced with paid help if he were to die. Funds need to be available to help Daniella cover this potential expense. Term insurance would provide pure insurance protection for Jorge at a relatively low cost. B. No, Jorge should not purchase life insurance, because first, he currently earns less than what Daniella does. Although he is still contributing to household income, his salary would not be missed if he were to die. Second, Jorge undoubtedly provides numerous household services and child care that would likely have to be replaced with paid help if he were to die. Funds need to be available to help Daniella cover this potential expense. Term insurance would provide pure insurance protection for Jorge at a relatively low cost. C. Yes, Jorge should purchase life insurance, because first, he currently earns more than what Daniella does, and his salary would be missed if he were to die. Second, Jorge undoubtedly provides numerous household services and child care that would likely have to be replaced with paid help if he were to die. Funds need to be available to help Daniella cover this potentia expense. Term insurance would provide pure insurance protection for Jorge at a relatively low cost. D. No, Jorge should not purchase life insurance, even though he currently earns less than what Daniella does, he is still contributing to household income and his salary would be missed if he were to die. However, Jorge undoubtedly provides numerous household services and child care that would likely have to be replaced with paid help if he were to die. Daniella would need to get a raise to cover this potential expense. Term insurance would provide pure insurance protection for Jorge at a relatively low cost. Jorge and Daniella Martinez, 30 and 35, are considering the purchase of life insurance. Jorge doesn't have any coverage, whereas Daniella has a $146,000 group policy at work. The Martinez have two young children, ages 3 and 5 . Jorge earns $30,000 annually from a part-time home-based business. Daniella's annual salary is $57,000. From their income, they save $7,300 a year. The rest goes for expenses. The couple estimates that the children will be financially dependent, except for college costs, for about another 15 years. Once the children are in college, Jorge assumes their annual expenses will be $61,917. In preparation for a visit with their insurance agent, the Martinezes have estimated the following expenses if Daniella were to die: They also anticipate, should Daniella die, Jorge will receive $7,900 a year in Social Security survivor's benefits until the youngest child turns 18 and $5,000 annually in pension benefits until Jorge turns 80 . Jorge projects his gross annual income to be $38,000 after his business expansion. Once the children are self-supporfing, Jorge wants to plan a spousal life income-that is, funds to make up the difference between his income and pension benefits and his expenses-for 15 more years, from age 45 to 60 . Lasthy, he wants to plan on $30,000 a year in retirement income for another 20 years, from age 60 to 80 . He anticipates receiving a 5 percent after-tax, after-inflation return on their investments. To date, the Martinezes have accumulated a total of $124,000 of assets, not including $46,000 of home equity. Their assets include $10,000 in an emergency fund, $12,000 in IRA funds for Jorge, $54,000 in other investments, and $48,000 in Daniella's 401(k) plan through her employer. a. What method should the Martinezes use to determine how much insurance they need? b. Should Jorge purchase an insurance policy? Why or why not? If so, what type of policy would you recommend for Jorge? c. What type of life insurance policy would you recommend that Daniella purchase? d. What will happen to Daniella's group life insurance if she leaves her present job? e. What could happen to the Martinezes' children if Daniella or Jorge should die without adequate life insurance coverage? f. Should the Martinezes name the children as life insurance beneficiaries? g. Which life insurance riders might the Martinezes select when purchasing a policy? h. Since they will make a concerted effort to become informed about life insurance, should the Martinezes also purchase life insurance on the children rather than waiting until later when they would have to reeducate themselves for life insurance shopping? i. The Martinezes have saved $7,300 a year for an emergency fund, retirement, and other investments, with the remainder spent to support their lifestyle. How might the concept of mental accountina and Princible 9: Mind Games. Your Financial Personalitv. and Your Monev affect their decision to nurchase life insurance? The total dependency expenses, or money in today's dollars needed for dependency expenses, is : (Round to the nearest dollar.) In step 5, the desired amount for spousal income, after the children are self-supporting, is $ (Round to the nearest dollar.) The total spousal life income, or money in today's dollars needed to provide desired spousal income, is \{ (Round to the nearest dollar.) In step 6, the total educational expenses for the children is \$ (Type a whole number.) In step 7 , the additional desired annual income at retirement is $ (Round to the nearest dollar.) The total retirement income, or money in today's dollars needed to provide for desired retirement income, is : (Round to the nearest dollar.) In step 8, the total funds needed in today's dollars to cover needs is $ (Round to the nearest dollar.) In step 9, the total cash from current policies is \$ (Type a whole number.) The amount in retirement savings and investments is $ (Type a whole number.) The amount in other assets is $ (Type a whole number.) h. Since they will make a concerted effort to become informed about life insurance, should the Martinezes also purchase life insurance on the children, rather than waiting until later when they would have to reeducate themselves for life insurance shopping? (Select the best choice below.) A. Although the children do not provide income, life insurance would be necessary. The primary needs are adequate protection on Daniella and Jorge to replace income in the event of their deaths; however, it doesn't hurt to have insurance on the children. B. Given that the children do not provide income, life insurance would not be necessary. The primary needs are adequate protection on Daniella and Jorge to replace income in the event of their deaths. C. Although the children provide income, life insurance would not be necessary. The primary needs are adequate income replacement in the event of Daniella or Jorge's deaths; the children do not contribute enough to the household income to warrant insuring them. D. Given that the children provide income, life insurance would be necessary. The primary needs are adequate income replacement in the event of any family member's death. f. Should the Martinezes name the children as life insurance beneficiaries? (Select the best choice below.) A. No. Minor children are generally paid only half the life insurance proceeds directly. The other half is kept by the insurance company, due to all the legal forms that must be filed to pay minor children. The policy should be set up to provide income to whoever will raise the children in the event of premature death, either the surviving spouse or guardian(s) for the children. B. Yes. Minor children generally can be paid life insurance proceeds directly. The policy should be set up to provide the same amount of income to each of the children. C. No. Minor children generally cannot be paid life insurance proceeds directly. The policy should be set up to provide income to whoever will raise the children in the event of premature death, either the surviving spouse or guardian(s) for the children. D. Yes. Minor children generally can be paid life insurance proceeds directly, as long as either the surviving spouse or guardian(s) for the children, know the children are receiving the money directly. The policy should be set up to deposit equal amounts in each child's bank account, and send a letter to either the surviving spouse or guardian(s) stating it has been done. e. What could happen to the Martinezes' children if Daniella or Jorge should die without adequate life insurance coverage? (Select the best choice below.) A. In the event of the death of Jorge or Daniella, without adequate life insurance coverage there would be limited funds provided for the children's living expenses, or for the achievement of specific financial goals (e.g., a college education). This would improve the children's standard of living. B. In the event of the death of Jorge or Daniella, without adequate life insurance coverage there would be limited funds provided for the children's living expenses. However, their college education would be paid for in full through Social Security Survivors' Benefits. This could cause a drop in the children's standard of living, until they went to college. C. In the event of the death of Jorge or Daniella, without adequate life insurance coverage there would be limited funds provided for the children's living expenses, or for the achievement of specific financial goals (e.g., a college education). This could cause a drop in the children's standard of living. D. In the event of the death of Jorge or Daniella, even without adequate life insurance coverage, there would be unlimited funds provided for the children's living expenses. However, once they reached age 18 , they would no longer receive any money to help with living expenses or college. This could cause a drop in the children's standard of living upon reaching age 18. i. The Martinezes have saved $7,300 a year for an emergency fund, retirement, and other investments, with the remainder spent to support their lifestyle. How might the concept of mental accounting and Principle 9: Mind Games, Your Financial Personality, and Your Money affect their decision to purchase life insurance? (Select the best choice below.) A. The Martinezes could assume that the current annual savings of $7,300 is required, and unless they can increase other living expenses or reduce income, then there simply is no money to fund additional life insurance for Jorge or Daniella. Despite the acknowledged need, they may agree that the mental account of savings is a more important goal than buying life insurance without conceding that affordable term insurance would provide immediate protection. The savings, albeit important, will accumulate a sufficient balance to protect the family in case of premature death. B. The Martinezes could assume that the current annual savings of $7,300 is required, and unless they can reduce other living expenses or increase income, then there simply is no money to fund additional life insurance for Jorge or Daniella. Despite the acknowledged need, they may agree that the mental account of savings is a more important goal than buying life insurance without conceding that affordable term insurance would provide immediate protection. The savings, albeit important, will not rapidly accumulate a sufficient balance to protect th family in case of premature death. C. The Martinezes could assume that the current annual savings of $7,300 is required, and unless they can reduce other living expenses or increase income, then they will simply have to stop contributing to Daniella's 401(k) to fund additional life insurance for Jorge or Daniella. Despite the acknowledged need, they may agree that the mental account of savings and purchasing insurance are more important goals than contributing to Daniella's 401(k) plan, because the 401(k) plan money would not be given to the family in case of Daniella's prematur death. D. The Martinezes could assume that the current annual savings of $7,300 is not required, but that there simply is no need to fund additional life insurance for Jorge or Daniella. Despite the actual need, they may agree that the mental account of savings is a more important goal and that they are young and do not need to be concerned with premature death

d. What would happen to Daniella's group life insurance if she leaves her present job? (Select the best choice below.) A. If Daniella left her present job, her employer-provided life insurance would continue until she found a new job with a group policy. This risk is a reason to have an emplyer-provided life insurance policy to avoid the greater risk of death occurring with no life insurance protection. B. If Daniella left her present job, her employer-provided life insurance would end. This risk is a reason to have a risk pooling policy to avoid the greater risk of death occurring with no life insurance protection. C. If Daniella left her present job, her employer-provided life insurance would end. This risk is a reason to have a renewable or convertible term policy to avoid the greater risk of death occurring with no life insurance protection. D. If Daniella left her present job, her employer-provided life insurance would continue until her death. This is a reason not to have a renewable or convertible term policy, because it would be spending more money than necessary. g. Which life insurance riders might the Martinezes select when purchasing a policy? Life insurance riders the Martinezes might select when purchasing a policy are: (Select all the choices that apply.) A. a waiver of premium for disability rider. B. a change of policy rider. C. a living benefits rider. D. a guaranteed insurability rider. E. a cost of living adjustment (COLA) rider. F. a lump-sum settlement rider. c. What type of life insurance policy would you recommend that Daniella purchase? (Select the best choice below.) A. Daniella should purchase a universal life insurance policy. It will provide the most protection for the least amount of premium cost. Since Daniella needs to purchase about $300,000 o additional insurance, she needs to find an affordable policy. B. Daniella should purchase a variable life insurance policy. It will provide the most protection for the least amount of premium cost. Since Daniella needs to purchase about $300,000 of additional insurance, she needs to find an affordable policy. C. Daniella should purchase a whole life insurance policy. It will provide the most protection for the least amount of premium cost. Since Daniella needs to purchase about $300,000 of additional insurance, she needs to find an affordable policy. D. Daniella should purchase a term insurance policy. It will provide the most protection for the least amount of premium cost. Since FranDaniellak needs to purchase about $300,000 of additional insurance, she needs to find an affordable policy. a. What method should the Martinezes use to determine how much insurance they need? In Step 1 of estimating their life insurance needs, the amount that the Martinezes estimate will be needed for immediate needs, should Daniella die, is $ (Type a whole numbe In Step 2, the amount that the Martinezes estimate will be needed to eliminate debt is $ (Type a whole number.) In Step 3, the amount that the Martinezes estimate will be needed for immediate transitional funds is $ (Type a whole number.) In step 4, dependency expenses, the current household expenses are $ (Round to the nearest dollar.) For the Martinezes, the deceased's expenses would be (Round to the nearest dollar.) The spousal income, or Jorge's projected income after his business expansion, is $ (Type a whole number.) The amount anticipated from Social Security Survivors' Benefits is (Type a whole number.) Hint: Assume the same amount will be received from Social Security until the youngest child turns 18 years old. The amount anticipated from pension benefits is ? (Type a whole number.) The income to be replaced until the children are self-supporting is (Round to the nearest dollar.) In step 10, it is determined that the amount of additional life insurance that should be purchased is (Round to the nearest dollar.) b. Should Jorge purchase an insurance policy? Why or why not? If so, what type of policy would you recommend for Wendy? (Select the best choice below.) A. Yes, Jorge should purchase life insurance, because first, although he currently earns less than what Daniella does, he is still contributing to household income and his salary would be missed if he were to die. Second, Jorge undoubtedly provides numerous household services and child care that would likely have to be replaced with paid help if he were to die. Funds need to be available to help Daniella cover this potential expense. Term insurance would provide pure insurance protection for Jorge at a relatively low cost. B. No, Jorge should not purchase life insurance, because first, he currently earns less than what Daniella does. Although he is still contributing to household income, his salary would not be missed if he were to die. Second, Jorge undoubtedly provides numerous household services and child care that would likely have to be replaced with paid help if he were to die. Funds need to be available to help Daniella cover this potential expense. Term insurance would provide pure insurance protection for Jorge at a relatively low cost. C. Yes, Jorge should purchase life insurance, because first, he currently earns more than what Daniella does, and his salary would be missed if he were to die. Second, Jorge undoubtedly provides numerous household services and child care that would likely have to be replaced with paid help if he were to die. Funds need to be available to help Daniella cover this potentia expense. Term insurance would provide pure insurance protection for Jorge at a relatively low cost. D. No, Jorge should not purchase life insurance, even though he currently earns less than what Daniella does, he is still contributing to household income and his salary would be missed if he were to die. However, Jorge undoubtedly provides numerous household services and child care that would likely have to be replaced with paid help if he were to die. Daniella would need to get a raise to cover this potential expense. Term insurance would provide pure insurance protection for Jorge at a relatively low cost. Jorge and Daniella Martinez, 30 and 35, are considering the purchase of life insurance. Jorge doesn't have any coverage, whereas Daniella has a $146,000 group policy at work. The Martinez have two young children, ages 3 and 5 . Jorge earns $30,000 annually from a part-time home-based business. Daniella's annual salary is $57,000. From their income, they save $7,300 a year. The rest goes for expenses. The couple estimates that the children will be financially dependent, except for college costs, for about another 15 years. Once the children are in college, Jorge assumes their annual expenses will be $61,917. In preparation for a visit with their insurance agent, the Martinezes have estimated the following expenses if Daniella were to die: They also anticipate, should Daniella die, Jorge will receive $7,900 a year in Social Security survivor's benefits until the youngest child turns 18 and $5,000 annually in pension benefits until Jorge turns 80 . Jorge projects his gross annual income to be $38,000 after his business expansion. Once the children are self-supporfing, Jorge wants to plan a spousal life income-that is, funds to make up the difference between his income and pension benefits and his expenses-for 15 more years, from age 45 to 60 . Lasthy, he wants to plan on $30,000 a year in retirement income for another 20 years, from age 60 to 80 . He anticipates receiving a 5 percent after-tax, after-inflation return on their investments. To date, the Martinezes have accumulated a total of $124,000 of assets, not including $46,000 of home equity. Their assets include $10,000 in an emergency fund, $12,000 in IRA funds for Jorge, $54,000 in other investments, and $48,000 in Daniella's 401(k) plan through her employer. a. What method should the Martinezes use to determine how much insurance they need? b. Should Jorge purchase an insurance policy? Why or why not? If so, what type of policy would you recommend for Jorge? c. What type of life insurance policy would you recommend that Daniella purchase? d. What will happen to Daniella's group life insurance if she leaves her present job? e. What could happen to the Martinezes' children if Daniella or Jorge should die without adequate life insurance coverage? f. Should the Martinezes name the children as life insurance beneficiaries? g. Which life insurance riders might the Martinezes select when purchasing a policy? h. Since they will make a concerted effort to become informed about life insurance, should the Martinezes also purchase life insurance on the children rather than waiting until later when they would have to reeducate themselves for life insurance shopping? i. The Martinezes have saved $7,300 a year for an emergency fund, retirement, and other investments, with the remainder spent to support their lifestyle. How might the concept of mental accountina and Princible 9: Mind Games. Your Financial Personalitv. and Your Monev affect their decision to nurchase life insurance? The total dependency expenses, or money in today's dollars needed for dependency expenses, is : (Round to the nearest dollar.) In step 5, the desired amount for spousal income, after the children are self-supporting, is $ (Round to the nearest dollar.) The total spousal life income, or money in today's dollars needed to provide desired spousal income, is \{ (Round to the nearest dollar.) In step 6, the total educational expenses for the children is \$ (Type a whole number.) In step 7 , the additional desired annual income at retirement is $ (Round to the nearest dollar.) The total retirement income, or money in today's dollars needed to provide for desired retirement income, is : (Round to the nearest dollar.) In step 8, the total funds needed in today's dollars to cover needs is $ (Round to the nearest dollar.) In step 9, the total cash from current policies is \$ (Type a whole number.) The amount in retirement savings and investments is $ (Type a whole number.) The amount in other assets is $ (Type a whole number.) h. Since they will make a concerted effort to become informed about life insurance, should the Martinezes also purchase life insurance on the children, rather than waiting until later when they would have to reeducate themselves for life insurance shopping? (Select the best choice below.) A. Although the children do not provide income, life insurance would be necessary. The primary needs are adequate protection on Daniella and Jorge to replace income in the event of their deaths; however, it doesn't hurt to have insurance on the children. B. Given that the children do not provide income, life insurance would not be necessary. The primary needs are adequate protection on Daniella and Jorge to replace income in the event of their deaths. C. Although the children provide income, life insurance would not be necessary. The primary needs are adequate income replacement in the event of Daniella or Jorge's deaths; the children do not contribute enough to the household income to warrant insuring them. D. Given that the children provide income, life insurance would be necessary. The primary needs are adequate income replacement in the event of any family member's death. f. Should the Martinezes name the children as life insurance beneficiaries? (Select the best choice below.) A. No. Minor children are generally paid only half the life insurance proceeds directly. The other half is kept by the insurance company, due to all the legal forms that must be filed to pay minor children. The policy should be set up to provide income to whoever will raise the children in the event of premature death, either the surviving spouse or guardian(s) for the children. B. Yes. Minor children generally can be paid life insurance proceeds directly. The policy should be set up to provide the same amount of income to each of the children. C. No. Minor children generally cannot be paid life insurance proceeds directly. The policy should be set up to provide income to whoever will raise the children in the event of premature death, either the surviving spouse or guardian(s) for the children. D. Yes. Minor children generally can be paid life insurance proceeds directly, as long as either the surviving spouse or guardian(s) for the children, know the children are receiving the money directly. The policy should be set up to deposit equal amounts in each child's bank account, and send a letter to either the surviving spouse or guardian(s) stating it has been done. e. What could happen to the Martinezes' children if Daniella or Jorge should die without adequate life insurance coverage? (Select the best choice below.) A. In the event of the death of Jorge or Daniella, without adequate life insurance coverage there would be limited funds provided for the children's living expenses, or for the achievement of specific financial goals (e.g., a college education). This would improve the children's standard of living. B. In the event of the death of Jorge or Daniella, without adequate life insurance coverage there would be limited funds provided for the children's living expenses. However, their college education would be paid for in full through Social Security Survivors' Benefits. This could cause a drop in the children's standard of living, until they went to college. C. In the event of the death of Jorge or Daniella, without adequate life insurance coverage there would be limited funds provided for the children's living expenses, or for the achievement of specific financial goals (e.g., a college education). This could cause a drop in the children's standard of living. D. In the event of the death of Jorge or Daniella, even without adequate life insurance coverage, there would be unlimited funds provided for the children's living expenses. However, once they reached age 18 , they would no longer receive any money to help with living expenses or college. This could cause a drop in the children's standard of living upon reaching age 18. i. The Martinezes have saved $7,300 a year for an emergency fund, retirement, and other investments, with the remainder spent to support their lifestyle. How might the concept of mental accounting and Principle 9: Mind Games, Your Financial Personality, and Your Money affect their decision to purchase life insurance? (Select the best choice below.) A. The Martinezes could assume that the current annual savings of $7,300 is required, and unless they can increase other living expenses or reduce income, then there simply is no money to fund additional life insurance for Jorge or Daniella. Despite the acknowledged need, they may agree that the mental account of savings is a more important goal than buying life insurance without conceding that affordable term insurance would provide immediate protection. The savings, albeit important, will accumulate a sufficient balance to protect the family in case of premature death. B. The Martinezes could assume that the current annual savings of $7,300 is required, and unless they can reduce other living expenses or increase income, then there simply is no money to fund additional life insurance for Jorge or Daniella. Despite the acknowledged need, they may agree that the mental account of savings is a more important goal than buying life insurance without conceding that affordable term insurance would provide immediate protection. The savings, albeit important, will not rapidly accumulate a sufficient balance to protect th family in case of premature death. C. The Martinezes could assume that the current annual savings of $7,300 is required, and unless they can reduce other living expenses or increase income, then they will simply have to stop contributing to Daniella's 401(k) to fund additional life insurance for Jorge or Daniella. Despite the acknowledged need, they may agree that the mental account of savings and purchasing insurance are more important goals than contributing to Daniella's 401(k) plan, because the 401(k) plan money would not be given to the family in case of Daniella's prematur death. D. The Martinezes could assume that the current annual savings of $7,300 is not required, but that there simply is no need to fund additional life insurance for Jorge or Daniella. Despite the actual need, they may agree that the mental account of savings is a more important goal and that they are young and do not need to be concerned with premature death Step by Step Solution

There are 3 Steps involved in it

Step: 1

To address the questions a What method should the Martinezes use to determine how much insurance they need Human Life Value Approach This method calcu...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Finance And Economics Discussion Series How Fast Do Personal Computers Depreciate Concepts And New Estimates

Authors: United States Federal Reserve Board, Mark E. Doms

1st Edition

1288712561, 9781288712564