Answered step by step

Verified Expert Solution

Question

1 Approved Answer

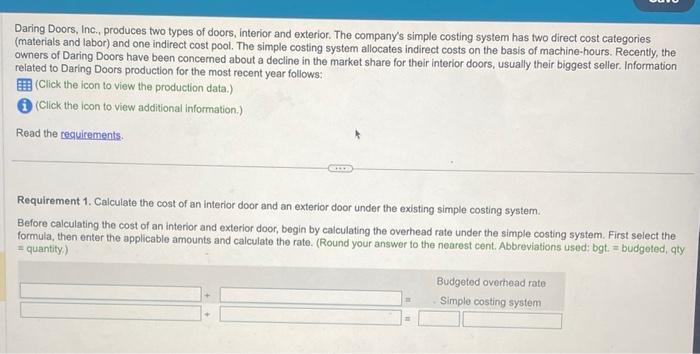

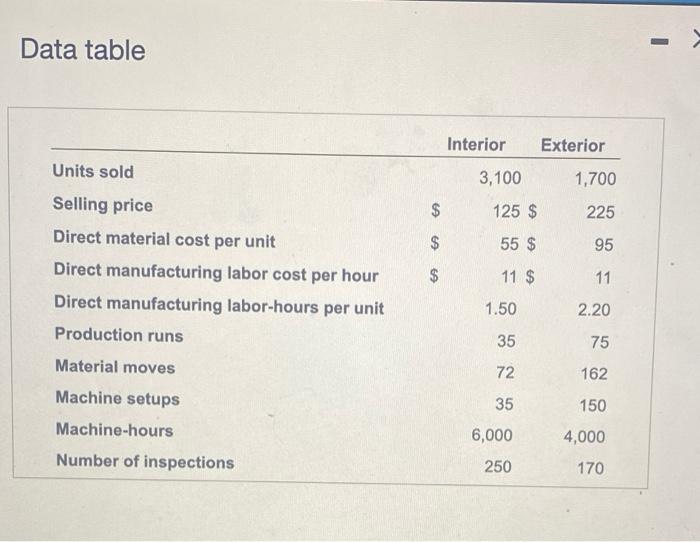

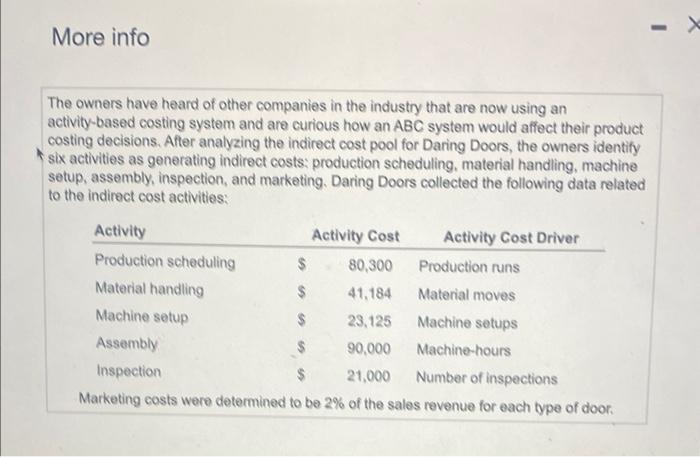

Daring Doors, Inc., produces two types of doors, interior and exterior. The company's simple costing system has two direct cost categories (materials and labor) and

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Managerial Accounting Wileyplus Blackboard Student Package

Authors: Charles E. Davis, Elizabeth Davis

3rd Edition

1119342511, 978-1119342519