Answered step by step

Verified Expert Solution

Question

1 Approved Answer

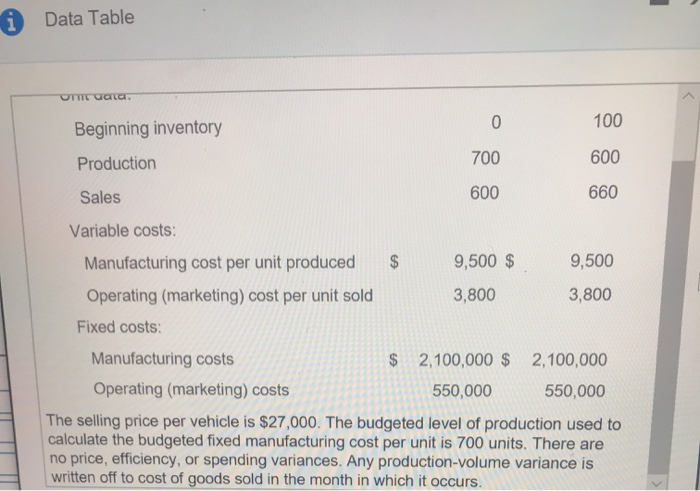

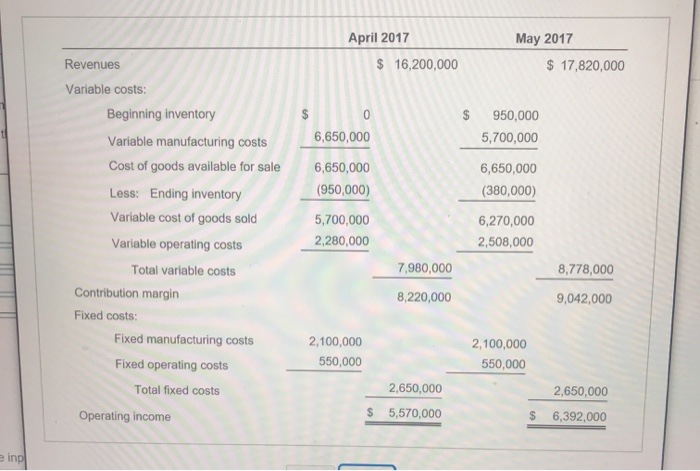

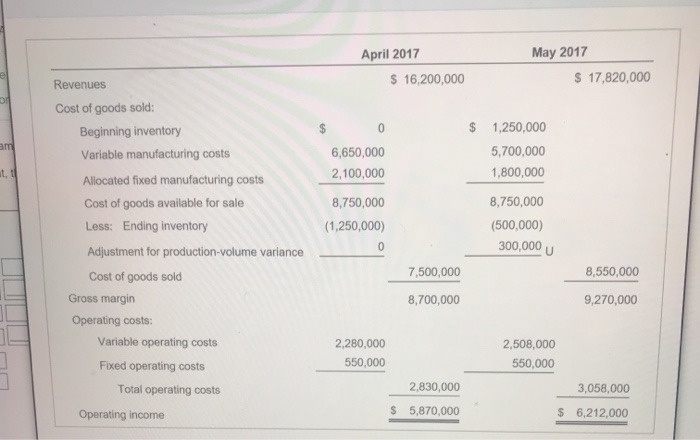

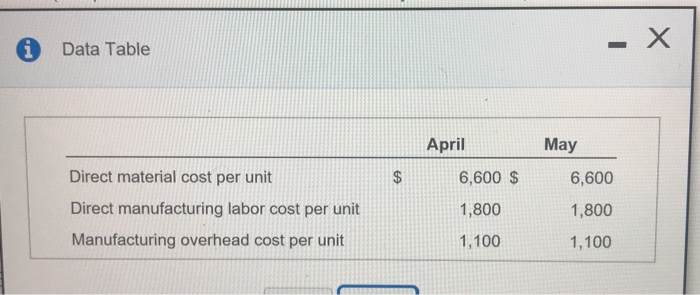

Data Table telr - OT aata 100 0 Beginning inventory 600 700 Production 660 600 Sales Variable costs: 9,500 $ 9,500 Manufacturing cost per unit

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Winning Your Audit Prepare Diligently Be Realistic Then Stand Your Ground

Authors: Holmes F. Crouch

2nd Edition

0944817319, 978-0944817315