Answered step by step

Verified Expert Solution

Question

1 Approved Answer

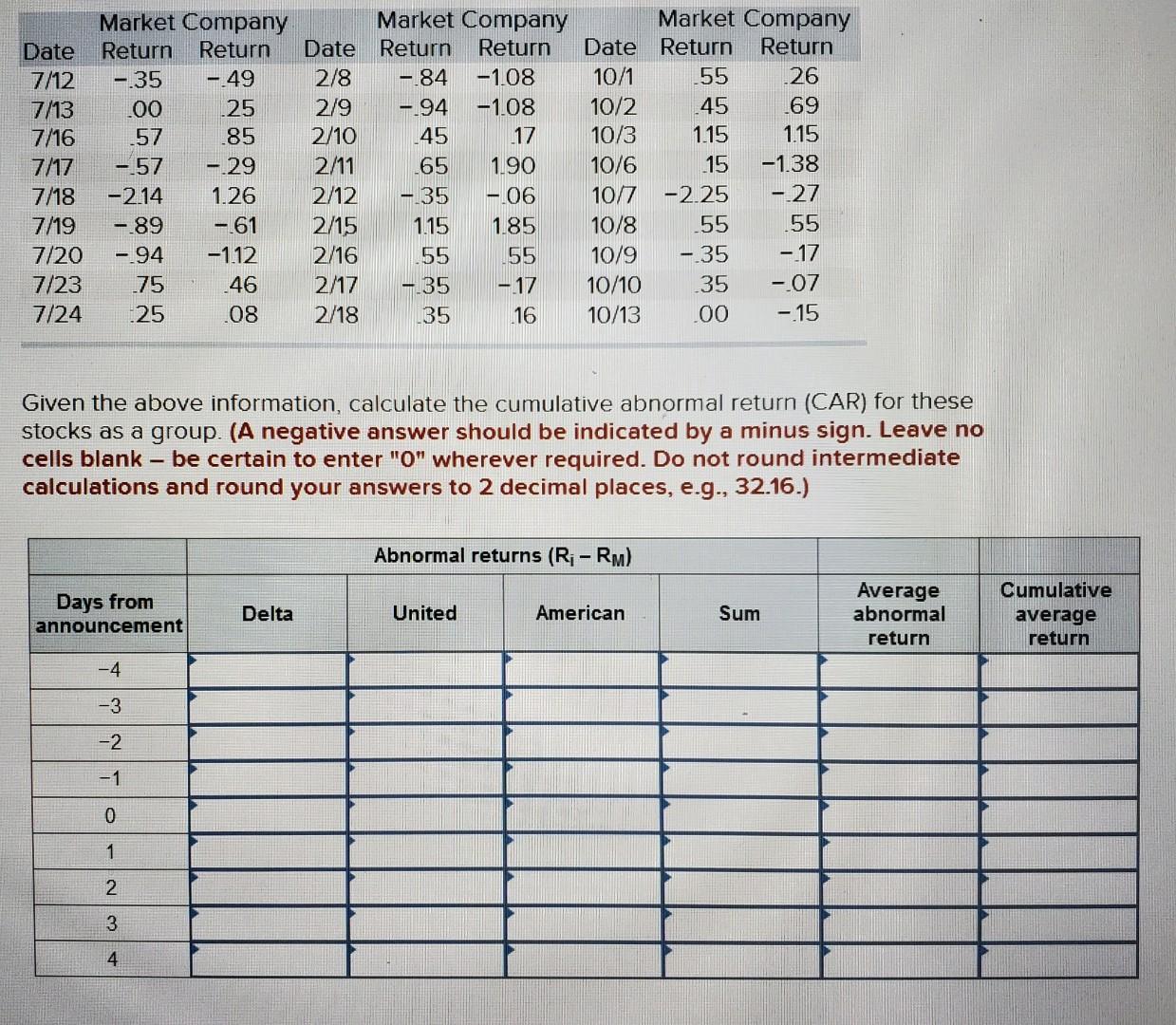

Date 7/12 7/13 7/16 7/17 7/18 7/19 7/20 7/23 7/24 Market Company Return Return - 35 - 49 00 25 57 85 -57 - 29

Date 7/12 7/13 7/16 7/17 7/18 7/19 7/20 7/23 7/24 Market Company Return Return - 35 - 49 00 25 57 85 -57 - 29 -2.14 1.26 -89 - 61 - 94 -1.12 75 46 25 08 Market Company Date Return Return 2/8 -.84 -1.08 2/9 -.94 -1.08 2/10 45 .17 2/11 65 1.90 2/12 - 35 -06 2/15 1.15 1.85 2/16 55 155 2/17 - 35 -17 2/18 35 .16 Market Company Date Return Return 10/1 55 .26 10/2 45 _69 10/3 1.15 1.15 10/6 .15 -1.38 10/7 -2.25 - 27 10/8 55 .55 10/9 - 35 -17 10/10 35 -07 10/13 00 -15 Given the above information, calculate the cumulative abnormal return (CAR) for these stocks as a group. (A negative answer should be indicated by a minus sign. Leave no cells blank be certain to enter "0" wherever required. Do not round intermediate calculations and round your answers to 2 decimal places, e.g., 32.16.) Abnormal returns (Ri - RM) Days from announcement Delta United American Sum Average abnormal return Cumulative average return -4 -3 -2 -1 0 1 2 3 4

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Sustainable Finance And Banking

Authors: Marcel Jeucken

1st Edition

1853837660, 978-1853837661