Dear Expert, If font size is still too small, please feel free to zoom in to view the text; as there is no other way to screenshot/capture this problem. Also, right clicking image, selecting opening image in new tab also works great. Thank you.

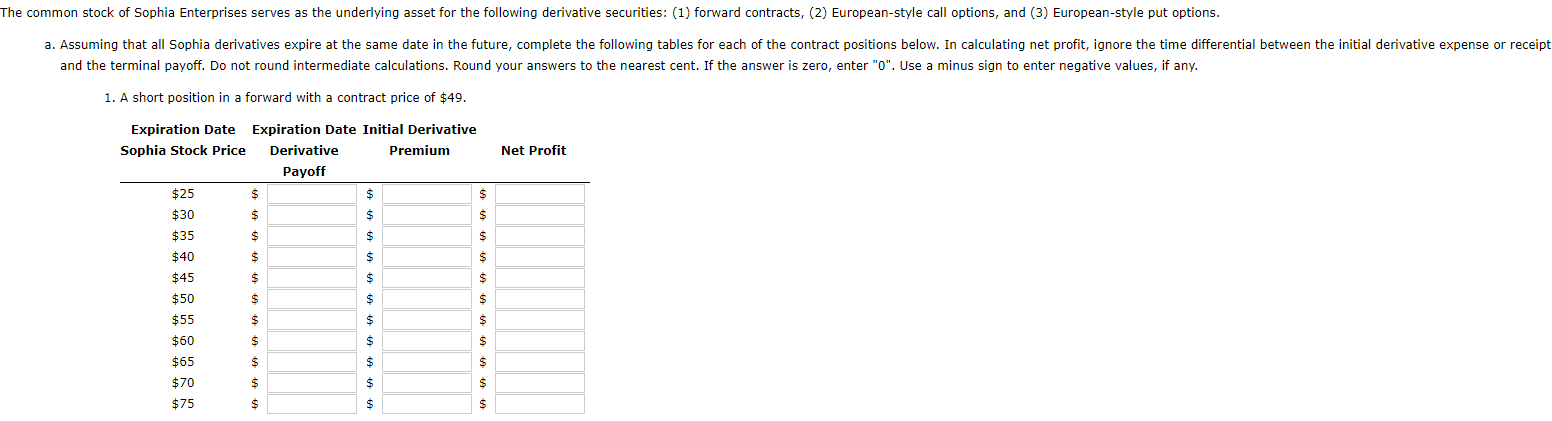

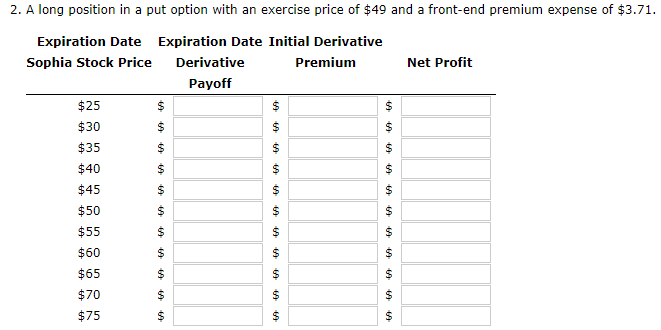

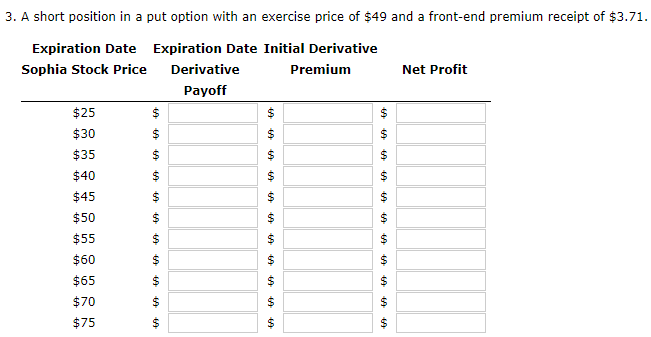

The common stock of Sophia Enterprises serves as the underlying asset for the following derivative securities: (1) forward contracts, (2) European-style call options, and (3) European-style put options. a. Assuming that all Sophia derivatives expire at the same date in the future, complete the following tables for each of the contract positions below. In calculating net profit, ignore the time differential between the initial derivative expense or receipt and the terminal payoff. Do not round intermediate calculations. Round your answers to the nearest cent. If the answer is zero, enter "0". Use a minus sign to enter negative values, if any. 1. A short position in a forward with contract price of $49. Net Profit Expiration Date Expiration Date Initial Derivative Sophia Stock Price Derivative Premium Payoff $25 $ $ $ $30 $ $ $ $35 $ $ $ $40 $ $ $45 $ $ $ $50 $ $ $ $55 $ $ $ $60 $ $ $ $65 $ $ $ $70 S $ $ $75 $ $ S 2. A long position in a put option with an exercise price of $49 and a front-end premium expense of $3.71. Net Profit $ $ Expiration Date Expiration Date Initial Derivative Sophia Stock Price Derivative Premium Payoff $25 $ $ $ $30 $ $ $ $35 $ $40 $ $ $ $45 S $ $50 $ S $55 S $60 S $ $65 S $70 S $75 S S $ VF ) $ $ 69 S 3. A short position in a put option with an exercise price of $49 and a front-end premium receipt of $3.71. Expiration Date Expiration Date Initial Derivative Sophia Stock Price Derivative Premium Net Profit Payoff $25 $ $ $ $30 $ $ $ $35 $ $ $40 $ $45 S $50 $55 $60 $ $ $65 S $ $70 $ $75 $ $ S $ $ $ $ $ S S S The breakeven (i.e., zero profit) point is $ c. What is the belief about the expiration date price of Sophia stock that an investor using each of these three positions implicitly holds? A short position in a forward with a contract price of $49: To be profitable for the seller, the price of Sophia Enterprises stock should be -Select- A long position in a put option with an exercise price of $49 and a front-end premium expense of $3.71: To be profitable for the buyer of the put, the price of Sophia Enterprises stock should be -Select- A short position in a put option with an exercise price of $49 and a front-end premium receipt of $3.71: To be profitable for the seller of the put, the price of Sophia Enterprises stock should be -Select- The common stock of Sophia Enterprises serves as the underlying asset for the following derivative securities: (1) forward contracts, (2) European-style call options, and (3) European-style put options. a. Assuming that all Sophia derivatives expire at the same date in the future, complete the following tables for each of the contract positions below. In calculating net profit, ignore the time differential between the initial derivative expense or receipt and the terminal payoff. Do not round intermediate calculations. Round your answers to the nearest cent. If the answer is zero, enter "0". Use a minus sign to enter negative values, if any. 1. A short position in a forward with contract price of $49. Net Profit Expiration Date Expiration Date Initial Derivative Sophia Stock Price Derivative Premium Payoff $25 $ $ $ $30 $ $ $ $35 $ $ $ $40 $ $ $45 $ $ $ $50 $ $ $ $55 $ $ $ $60 $ $ $ $65 $ $ $ $70 S $ $ $75 $ $ S 2. A long position in a put option with an exercise price of $49 and a front-end premium expense of $3.71. Net Profit $ $ Expiration Date Expiration Date Initial Derivative Sophia Stock Price Derivative Premium Payoff $25 $ $ $ $30 $ $ $ $35 $ $40 $ $ $ $45 S $ $50 $ S $55 S $60 S $ $65 S $70 S $75 S S $ VF ) $ $ 69 S 3. A short position in a put option with an exercise price of $49 and a front-end premium receipt of $3.71. Expiration Date Expiration Date Initial Derivative Sophia Stock Price Derivative Premium Net Profit Payoff $25 $ $ $ $30 $ $ $ $35 $ $ $40 $ $45 S $50 $55 $60 $ $ $65 S $ $70 $ $75 $ $ S $ $ $ $ $ S S S The breakeven (i.e., zero profit) point is $ c. What is the belief about the expiration date price of Sophia stock that an investor using each of these three positions implicitly holds? A short position in a forward with a contract price of $49: To be profitable for the seller, the price of Sophia Enterprises stock should be -Select- A long position in a put option with an exercise price of $49 and a front-end premium expense of $3.71: To be profitable for the buyer of the put, the price of Sophia Enterprises stock should be -Select- A short position in a put option with an exercise price of $49 and a front-end premium receipt of $3.71: To be profitable for the seller of the put, the price of Sophia Enterprises stock should be -Select