Answered step by step

Verified Expert Solution

Question

1 Approved Answer

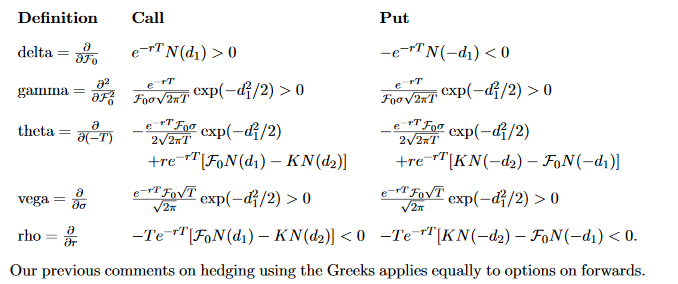

Definition Put delta-o e-r TM (d) > 0 gamma theta _w2fy ) exp(-di/2 2V2TI x/2)0 T F Our previous comments on hedging using the Greeks

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Misbehavior Of Markets A Fractal View Of Financial Turbulence

Authors: Benoit Mandelbrot, Richard L Hudson

1st Edition

0465043577, 978-0465043576