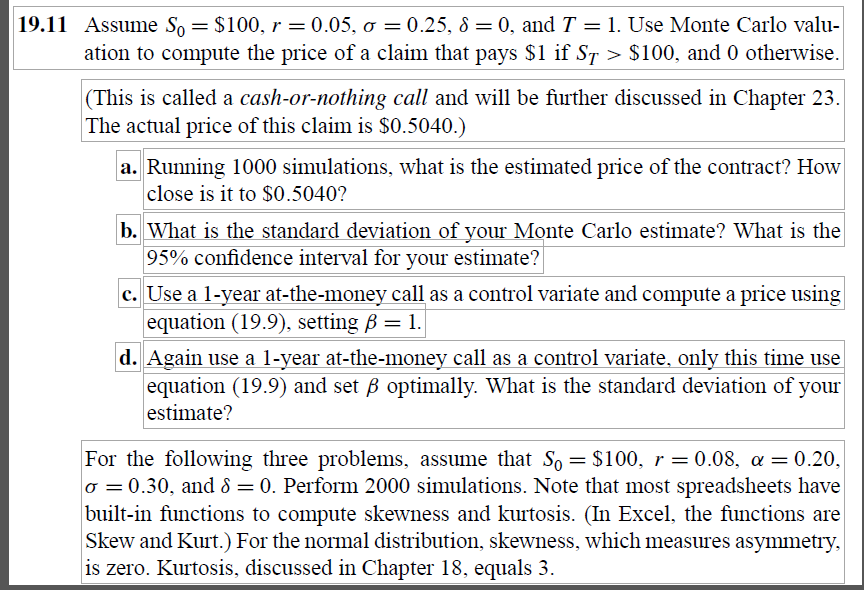

Derivatives Markets |(3rd Edition) Chapter 19, Problem 11P Bookmark Show all steps: ON Step-by-step solution There is no solution to this problem yet. Get help from a Chegg subject expert. Ask an expert 19.11 Assume So = $100, r = 0.05, 0 = 0.25, 8=0, and T =1. Use Monte Carlo valu- ation to compute the price of a claim that pays $1 if St > $100, and 0 otherwise. (This is called a cash-or-nothing call and will be further discussed in Chapter 23. The actual price of this claim is $0.5040.) a. Running 1000 simulations, what is the estimated price of the contract? How close is it to $0.5040? What is the standard deviation of your Monte Carlo estimate? What is the 95% confidence interval for your estimate? c. Use a 1-year at-the-money call as a control variate and compute a price using equation (19.9), setting B = 1. d. Again use a 1-year at-the-money call as a control variate, only this time use equation (19.9) and set B optimally. What is the standard deviation of your estimate? For the following three problems, assume that So = $100, r = 0.08, a=0.20, O=0.30, and S=0. Perform 2000 simulations. Note that most spreadsheets have built-in functions to compute skewness and kurtosis. (In Excel, the functions are Skew and Kurt.) For the normal distribution, skewness, which measures asymmetry, is zero. Kurtosis, discussed in Chapter 18, equals 3. Derivatives Markets |(3rd Edition) Chapter 19, Problem 11P Bookmark Show all steps: ON Step-by-step solution There is no solution to this problem yet. Get help from a Chegg subject expert. Ask an expert 19.11 Assume So = $100, r = 0.05, 0 = 0.25, 8=0, and T =1. Use Monte Carlo valu- ation to compute the price of a claim that pays $1 if St > $100, and 0 otherwise. (This is called a cash-or-nothing call and will be further discussed in Chapter 23. The actual price of this claim is $0.5040.) a. Running 1000 simulations, what is the estimated price of the contract? How close is it to $0.5040? What is the standard deviation of your Monte Carlo estimate? What is the 95% confidence interval for your estimate? c. Use a 1-year at-the-money call as a control variate and compute a price using equation (19.9), setting B = 1. d. Again use a 1-year at-the-money call as a control variate, only this time use equation (19.9) and set B optimally. What is the standard deviation of your estimate? For the following three problems, assume that So = $100, r = 0.08, a=0.20, O=0.30, and S=0. Perform 2000 simulations. Note that most spreadsheets have built-in functions to compute skewness and kurtosis. (In Excel, the functions are Skew and Kurt.) For the normal distribution, skewness, which measures asymmetry, is zero. Kurtosis, discussed in Chapter 18, equals 3