Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Describe how this analyst justifies the price target. D15-48. Interpreting Analysts Reports that Use Valuation with Multiples Refer to the following excerpts from an analysts'

Describe how this analyst justifies the price target.

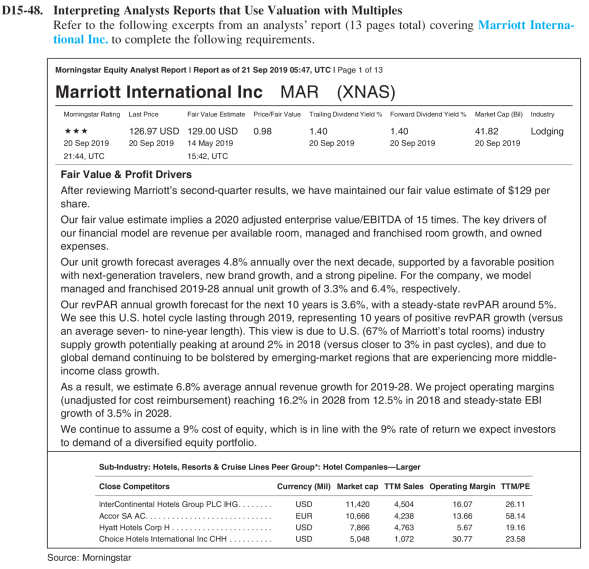

D15-48. Interpreting Analysts Reports that Use Valuation with Multiples Refer to the following excerpts from an analysts' report (13 pages total) covering Marriott Interna- tional Inc. to complete the following requirements. Morningstar Equity Analyst Report | Report as of 21 Sep 2019 05:47, UTC I Page 1 of 13 Marriott International Inc MAR (XNAS) Morningstar Rating Last Price Fair Value Estimate PriceFar Value Trailing Dividend Yield Forward Dividend Yield Market Cap (4) Industry 126,97 USD 129.00 USD 0.98 1.40 1.40 41.82 Lodging 20 Sep 2019 20 Sep 2019 14 May 2019 20 Sep 2019 20 Sep 2019 20 Sep 2019 21:44 UTC 15:42, UTC Fair Value & Profit Drivers After reviewing Marriott's second-quarter results, we have maintained our fair value estimate of $129 per share. Our fair value estimate implies a 2020 adjusted enterprise value/EBITDA of 15 times. The key drivers of our financial model are revenue per available room, managed and franchised room growth, and owned expenses. Our unit growth forecast averages 4.8% annually over the next decade, supported by a favorable position with next-generation travelers, new brand growth, and a strong pipeline. For the company, we model managed and franchised 2019-28 annual unit growth of 3.3% and 6.4%, respectively. Our revPAR annual growth forecast for the next 10 years is 3.6%, with a steady-state revPAR around 5%. We see this U.S. hotel cycle lasting through 2019, representing 10 years of positive revPAR growth (versus an average seven- to nine-year length). This view is due to U.S. (67% of Marriott's total rooms) industry supply growth potentially peaking at around 2% in 2018 (versus closer to 3% in past cycles), and due to global demand continuing to be bolstered by emerging-market regions that are experiencing more middle- income class growth. As a result, we estimate 6.8% average annual revenue growth for 2019-28. We project operating margins (unadjusted for cost reimbursement) reaching 16.2% in 2028 from 12.5% in 2018 and steady-state EBI growth of 3.5% in 2028 We continue to assume a 9% cost of equity, which is in line with the 9% rate of return we expect investors to demand of a diversified equity portfolio. Sub-Industry: Hotels, Resorts & Cruise Lines Peer Group: Hotel Companies-Larger Close Competitors Currency (Min) Market cap TTM Sales Operating Margin TTMPE InterContinental Hotels Group PLC HG. 11,420 4,504 16.07 26.11 Accor SA AC EUR 10,686 Hyatt Hotels Corp 4.763 Choice Hotels Interational Inc CHH USD 4.238 USD USD 7.866 5,048 13.66 5.67 30.77 58.14 19.16 23.58 1,072 Source: Morningstar D15-48. Interpreting Analysts Reports that Use Valuation with Multiples Refer to the following excerpts from an analysts' report (13 pages total) covering Marriott Interna- tional Inc. to complete the following requirements. Morningstar Equity Analyst Report | Report as of 21 Sep 2019 05:47, UTC I Page 1 of 13 Marriott International Inc MAR (XNAS) Morningstar Rating Last Price Fair Value Estimate PriceFar Value Trailing Dividend Yield Forward Dividend Yield Market Cap (4) Industry 126,97 USD 129.00 USD 0.98 1.40 1.40 41.82 Lodging 20 Sep 2019 20 Sep 2019 14 May 2019 20 Sep 2019 20 Sep 2019 20 Sep 2019 21:44 UTC 15:42, UTC Fair Value & Profit Drivers After reviewing Marriott's second-quarter results, we have maintained our fair value estimate of $129 per share. Our fair value estimate implies a 2020 adjusted enterprise value/EBITDA of 15 times. The key drivers of our financial model are revenue per available room, managed and franchised room growth, and owned expenses. Our unit growth forecast averages 4.8% annually over the next decade, supported by a favorable position with next-generation travelers, new brand growth, and a strong pipeline. For the company, we model managed and franchised 2019-28 annual unit growth of 3.3% and 6.4%, respectively. Our revPAR annual growth forecast for the next 10 years is 3.6%, with a steady-state revPAR around 5%. We see this U.S. hotel cycle lasting through 2019, representing 10 years of positive revPAR growth (versus an average seven- to nine-year length). This view is due to U.S. (67% of Marriott's total rooms) industry supply growth potentially peaking at around 2% in 2018 (versus closer to 3% in past cycles), and due to global demand continuing to be bolstered by emerging-market regions that are experiencing more middle- income class growth. As a result, we estimate 6.8% average annual revenue growth for 2019-28. We project operating margins (unadjusted for cost reimbursement) reaching 16.2% in 2028 from 12.5% in 2018 and steady-state EBI growth of 3.5% in 2028 We continue to assume a 9% cost of equity, which is in line with the 9% rate of return we expect investors to demand of a diversified equity portfolio. Sub-Industry: Hotels, Resorts & Cruise Lines Peer Group: Hotel Companies-Larger Close Competitors Currency (Min) Market cap TTM Sales Operating Margin TTMPE InterContinental Hotels Group PLC HG. 11,420 4,504 16.07 26.11 Accor SA AC EUR 10,686 Hyatt Hotels Corp 4.763 Choice Hotels Interational Inc CHH USD 4.238 USD USD 7.866 5,048 13.66 5.67 30.77 58.14 19.16 23.58 1,072 Source: MorningstarStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Day Trading Profit Kit Beast Mode Support And Resistance Trading Strategy T That Lets You Profit From Loosing Traders

Authors: Profit King

1st Edition

979-8389011557