Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Describe the difference between strictly stationary processes and weakly stationary processes. Explain why weakly stationary multivariate normal processes are also strictly stationary. Show that

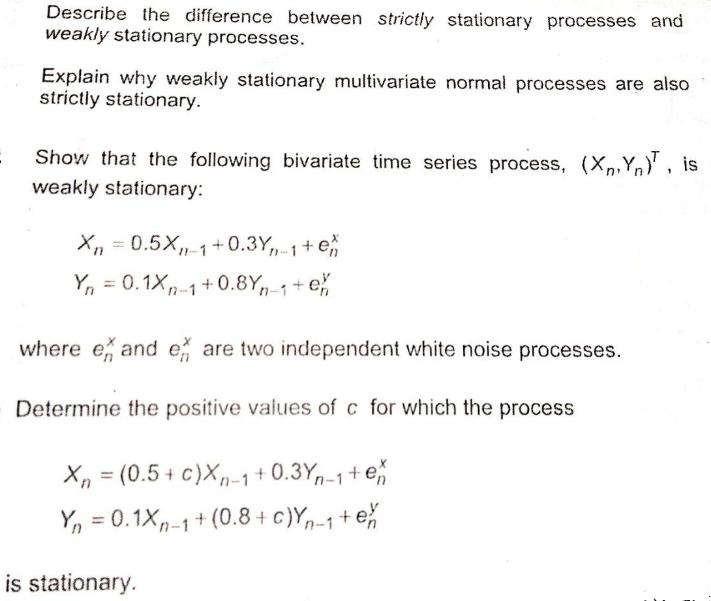

Describe the difference between strictly stationary processes and weakly stationary processes. Explain why weakly stationary multivariate normal processes are also strictly stationary. Show that the following bivariate time series process, (X,Y), is weakly stationary: 1 Xn=0.5X, 1+0.3Y,, 1+e Yn = 0.1Xn-1+0.8Yn 1+e where e and e are two independent white noise processes. Determine the positive values of c for which the process X = (0.5+ c)Xn-1 +0.3Yn-1+en Yn = 0.1Xn-1+ (0.8+ c)Y-1+ex is stationary.

Step by Step Solution

★★★★★

3.30 Rating (147 Votes )

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Reporting Financial Statement Analysis And Valuation A Strategic Perspective

Authors: James M Wahlen, Stephen P Baginskl, Mark T Bradshaw

7th Edition

9780324789423, 324789416, 978-0324789416