Answered step by step

Verified Expert Solution

Question

1 Approved Answer

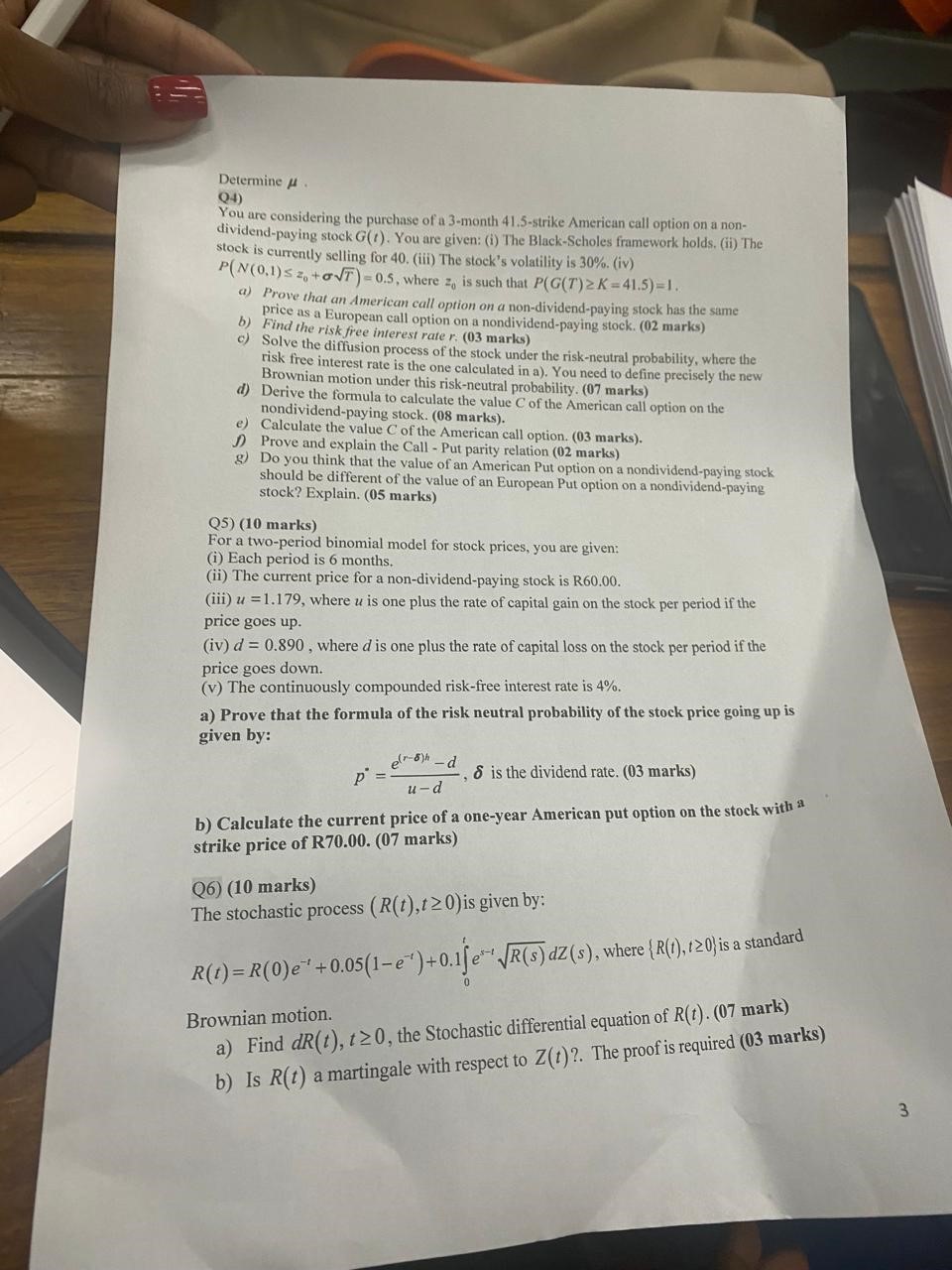

Determine . Q 4 ) You are considering the purchase of a 3 - month 4 1 . 5 - strike American call option on

Determine

Q

You are considering the purchase of a month strike American call option on a non

dividendpaying stock You are given: i The BlackScholes framework holds. ii The

stock is currently selling for iii The stock's volatility is iv

where is such that

a Prove that an American call option on a nondividendpaying stock has the same

price as a European call option on a nondividendpaying stock. marks

b Find the risk free interest rate marks

c Solve the diffusion process of the stock under the riskneutral probability, where the

risk free interest rate is the one calculated in a You need to define precisely the new

Brownian motion under this riskneutral probability. marks

d Derive the formula to calculate the value of the American call option on the

nondividendpaying stock. marks

e Calculate the value of the American call option. marks

J Prove and explain the Call Put parity relation marks

g Do you think that the value of an American Put option on a nondividendpaying stock

should be different of the value of an European Put option on a nondividendpaying

stock? Explain. marks

Q marks

For a twoperiod binomial model for stock prices, you are given:

i Each period is months.

ii The current price for a nondividendpaying stock is R

iii where is one plus the rate of capital gain on the stock per period if the

price goes up

iv where is one plus the rate of capital loss on the stock per period if the

price goes down.

v The continuously compounded riskfree interest rate is

a Prove that the formula of the risk neutral probability of the stock price going up is

given by:

the dividend rate. marks

b Calculate the current price of a oneyear American put option on the stock with

strike price of marks

Q marks

The stochastic process is given by:

where a standard

Brownian motion.

a Find the Stochastic differential equation of mark

b Is a martingale with respect to The proof is required marks

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Fundamentals Of Healthcare Finance

Authors: Paula H. Song, Kristin L. Reiter

4th Edition

1640553223, 978-1640553224