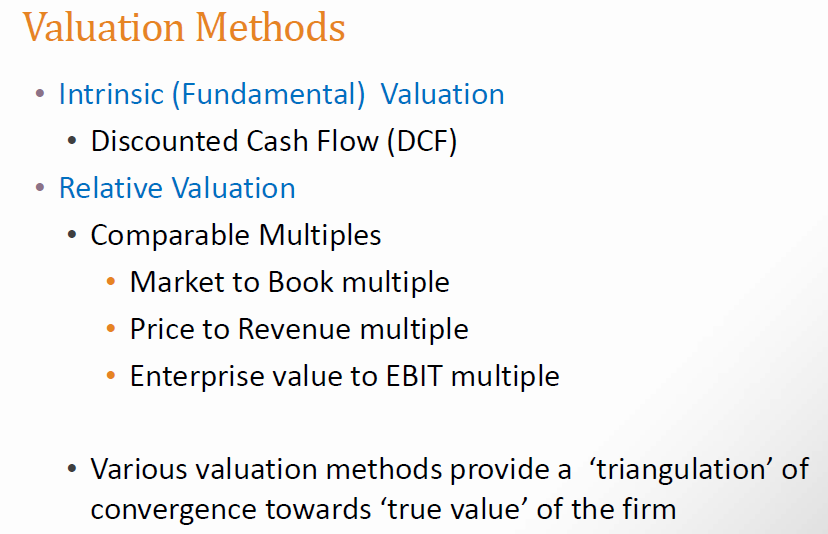

Determine the Value of the firm PNC using Discount CashFlow.

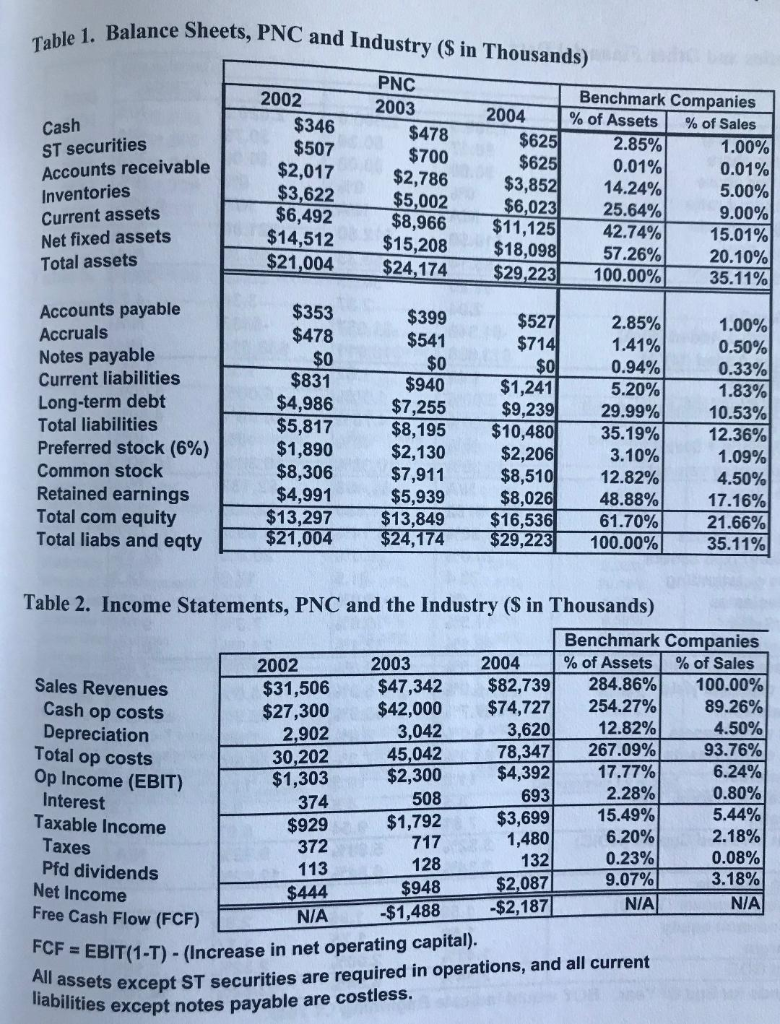

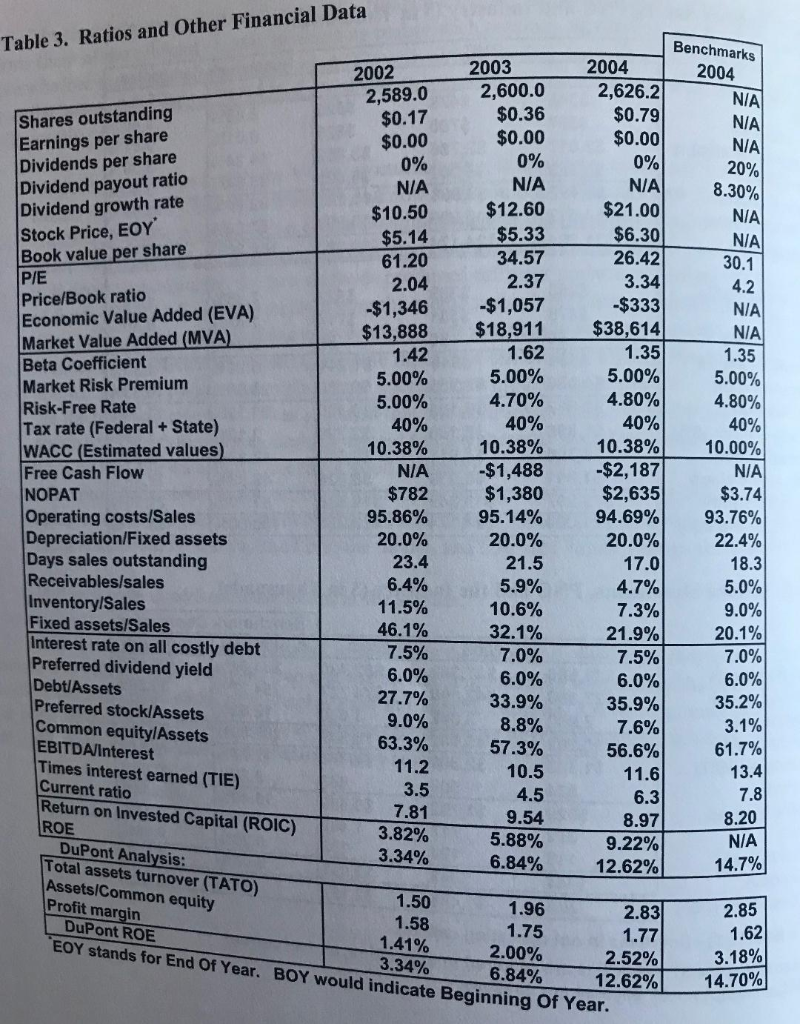

Table 1. Balance Sheets, PNC and Industry ($ in Thousands) PNC Benchmark Companies % of Assets 2002 2003 2004 $346 $507 $2,017 $3,622 $6,492 $14,512 $21,004 Cash ST securities Accounts receivable Inventories Current assets Net fixed assets Total assets % of Sales $478 $700 $2,786 $5,002 $8,966 $15,208 $24,174 $625 $625 $3,852 $6,023 $11,125 $18,098 $29,223 2.85% 1.00% 0.01% 5.00% 9.00% 15.01% 20.10% 0.01% 14.24% 25.64% 42.74% 57.26% 100.00% 35.11% Accounts payable Accruals Notes payable Current liabilities $353 $478 $399 $541 $0 $940 $7,255 $8,195 $2,130 $7,911 $5,939 $13,849 $24,174 $527 $714 $0 $1,241 $9,239 $10,480 $2,206 $8,510 $8,026 $16,536 $29,223 2.85% 1.41% 0.94% 1.00% 0.50% $0 $831 $4,986 $5,817 $1,890 $8,306 $4,991 $13,297 $21,004 0.33% 5.20% 29.99% 35.19% 3.10% 12.82% 1.83% Long-term debt Total liabilities 10.53% 12.36% 1.09% 4.50% 17.16% 21.66% 35.11% Preferred stock (6%) Common stock Retained earnings Total com equity Total liabs and eqty 48.88% 61.70% 100.00% Table 2. Income Statements, PNC and the Industry (S in Thousands) Benchmark Companies % of Assets 284.86% 254.27% 2004 % of Sales 2003 2002 $82,739 $74,727 3,620 78,347 $4,392 693 $3,699 1,480 132 Sales Revenues Cash op costs Depreciation Total op costs Op Income (EBIT) Interest Taxable Income $47,342 $42,000 3,042 45,042 $2,300 508 100.00% 89.26% 4.50% $31,506 $27,300 2,902 30,202 $1,303 12.82% 267.09% 17.77% 2.28% 93.76% 6.24% 0.80% 5.44% 374 15.49% 6.20% $1,792 717 $929 372 2.18% 0.08% Taxes 0.23% 128 Pfd dividends Net Income Free Cash Flow (FCF) 113 9.07% 3.18% $2,087 $948 $444 N/A N/A $2,187 $1,488 N/A FCF = EBIT(1-T) - (Increase in net operating capital). All assets except ST securities are required in operations, and all current labilities except notes payable are costless. Table 3. Ratios and Other Financial Data Benchmarks 2004 2003 2004 2002 2,589.0 $0.17 $0.00 0% 2,626.2 $0.79 $0.00 0% N/A $21.00 $6.30 26.42 2,600.0 $0.36 $0.00 N/A N/A N/A 20% 8.30% Shares outstanding Earnings per share Dividends per share Dividend payout ratio Dividend growth rate Stock Price, EOY Book value per share P/E Price/Book ratio Economic Value Added (EVA) Market Value Added (MVA) Beta Coefficient Market Risk Premium Risk-Free Rate Tax rate (Federal + State) WACC (Estimated values) Free Cash Flow NOPAT Operating costs/Sales Depreciation/Fixed assets Days sales outstanding Receivables/sales Inventory/Sales Fixed assets/Sales Interest rate on all costly debt Preferred dividend yield Debt/Assets Preferred stock/Assets Common equity/Assets EBITDA/Interest Times interest earned (TIE) Current ratio Return on Invested Capital (ROIC) ROE DuPont Analysis: Total assets turnover (TATO) Assets/Common equity Profit margin DuPont ROE EOY stands for End Of Year. BOY would indicate Beginning Of Year. 0% N/A N/A $12.60 $5.33 $10.50 $5.14 N/A N/A 30.1 34.57 61.20 2.37 3.34 2.04 4.2 -$333 $38,614 -$1,057 -$1,346 $13,888 N/A $18,911 N/A 1.62 1.35 1.35 1.42 5.00% 5.00% 5.00% 5.00% 4.80% 4.70% 5.00% 40% 4.80% 40% 40% 40% 10.00% 10.38% 10.38% 10.38% -$2,187 $2,635 94.69% -$1,488 $1,380 95.14% N/A N/A $3.74 $782 95.86% 93.76% 20.0% 20.0% 20.0% 22.4% 23.4 21.5 17.0 18.3 6.4% 5.9% 4.7% 5.0% 11.5% 9.0% 20.1 % 10.6% 7.3% 46.1% 32.1% 21.9% 7.5% 7.0% 6.0% 7.5% 7.0% 6.0% 27.7% 6.0% 6.0% 33.9% 8.8% 57.3% 35.9% 7.6% 35.2% 9.0% 3.1% 63.3% 61.7% 13.4 56.6% 11.6 11.2 10.5 3.5 7.81 7.8 8.20 N/A 4.5 6.3 9.54 5.88% 6.84% 8.97 3.82% 9.22% 3.34% 14.7% 12.62% 1.50 1.58 1.41% 3.34% 1.96 2.83 2.85 1.75 2.00% 6.84% 1.62 1.77 3.18% 14.70% 2.52% 12.62% Valuation Methods Intrinsic (Fundamental) Valuation Discounted Cash Flow (DCF) Relative Valuation Comparable Multiples Market to Book multiple Price to Revenue multiple Enterprise value to EBIT multiple Various valuation methods provide a 'triangulation' of convergence towards 'true value' of the firm