Develop a chart of Director's financial presentation based on the Case Example, displayed in our text in Appendix Chapter 9-A, for Harris Memorial Hospital and Harris Community Foundation's Audited Financial Statements and Footnotes. In preparing your analysis, be sure to use the format in Chapter 13, (Table13-7) and (Figure13-4) to display your analysis and explanation for the comparative years December 31, 20X7 and 20X6.

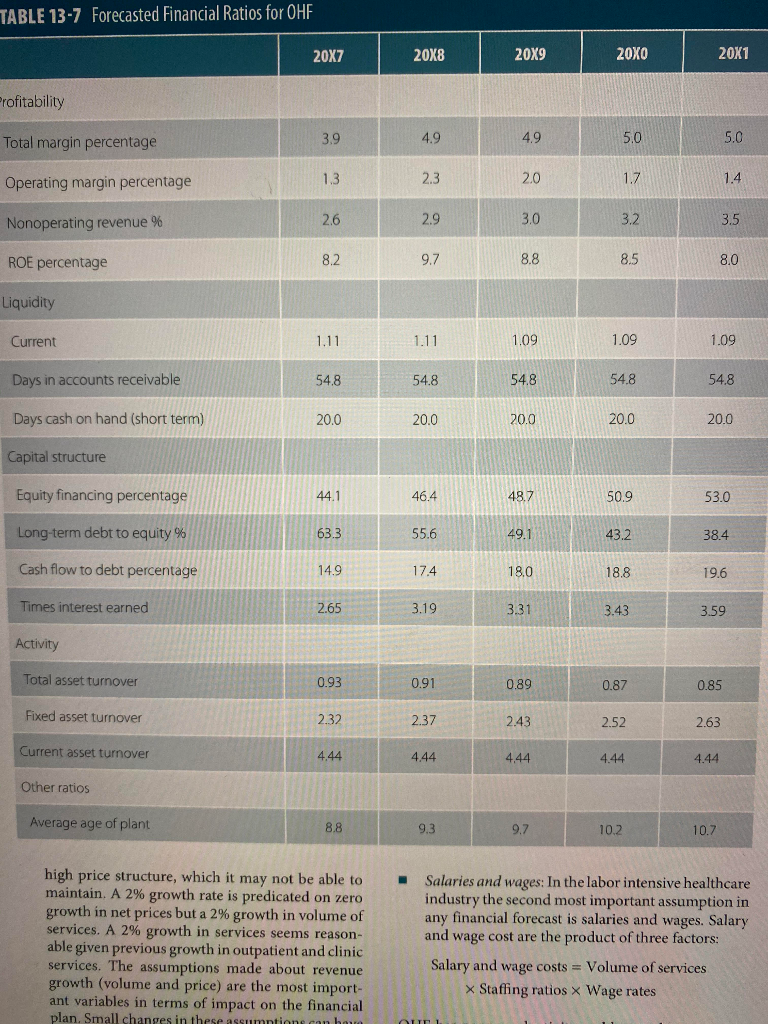

The images below are of the Appendix 9-A, Table 13-7 and Figure 13-4. All information has been included.

Profitability

Total margin percentage: ____________

Operating margin percentage: ____________

Nonoperating revenue %: ____________

ROE percentage: ____________

Liquidity

Current: ____________

Days in accounts receivable: ____________

Days cash on hand (short term): ____________

Capital structure

Equity financing percentage: ____________

Long-term debt to equity %: ____________

Cash flow to debt percentage: ____________

Times interest earned: ____________

Activity

Total asset turnover: ____________

Fixed asset turnover: ____________

Current asset turnover: ____________

Other ratios

Average age of plant: ____________

CASE 9A

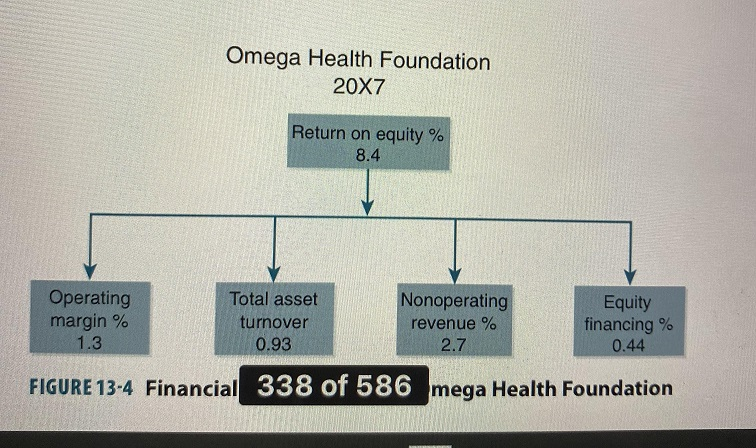

Table 13-7

Figure 13-4

provide a basis for our audit opinion. In our opinion, the financial statements referred to above present fairly, in all material respects, the combined financial position of Harris Memorial subsidiaries at December 31, 20X7 and 20X6, and the combined changes in their net assets and their cash flows for the years then ended in conformity with U.S. generally accepted accounting principles. TABLE 9A-1 Harris Memorial Hospital and Harris Community Foundation Combined Balance Sheets (in Thousands) December 31, 20X7 December 31, 20X6 Assets Current assets Cash and cash equivalents $82,815 $59,696 Assets limited as to use, current portion 5,327 5,088 Accounts receivable Patients, less allowance for doubtful accounts ($25,302 in 20X7 and $23,014 in 20X6) 70,025 59,939 Other 28,990 24,995 Supplies 7,078 6,663 Total current assets 194,235 156,381 Assets limited as to use For donor-restricted purposes 84,440 67,826 Board designated for specific purposes 382,835 378,413 Held by trustees under bond agreements 51,038 25,937 518,313 472,176 Less current portion 5,327 5,088 512,986 467,088 Property and equipment, net 563,349 458,829 Other assets 34,476 34,302 Total assets $1,305,046 $1,116,600 Liabilities and net assets Current liabilities Accounts payable $32,572 $24,631 Accrued expenses and other liabilities 58,878 53,725 Due to third-party payers 7,380 12,633 Current maturities of long-term debt 4,692 5,908 Total current liabilities 103,522 96,897 Long-term debt, less current maturities 439,597 332,354 Contingent professional liabilities 33,260 48,487 Due to broker 15,128 19,608 Other liabilities 20,713 5,298 Postretirement benefit obligation, other than pensions 8,207 7,694 Total liabilities 620,427 510,338 Net assets Unrestricted 538,436 Temporarily restricted 55,213 40,393 Permanently restricted 29,227 27,433 Total net assets 684,619 606,262 Total liabilities and net assets $1,305,046 $1,116,600 TABLE 9A-2 Harris Memorial Hospital and Harris Community Foundation Combined Statements of Operations (in Thousands) December 31, 20X7 December 31, 20X6 Operating revenues and other support $829,005 $774,662 Net patient service revenue (55,851) (57,975) Provision for doubtful accounts 773,154 716,687 Net patient service revenue less provision for doubtful accounts 27,055 29,334 Other operating revenue 800,209 746,021 Total operating revenue (continues) TABLE 9A-2 Harris Memorial Hospital and Harris Community Foundation Combined Statements of Operations (in Thousands) (continued) Operating expenses Salaries and wages $371,449 $329,668 Employee benefits 81,532 77,231 Supplies and purchased services 228,244 225,497 Advertising 3,072 2,376 Staff enrichment 10,767 8,591 Occupancy cost 14,346 13,442 Depreciation 44,392 41,627 Interest 10,974 6,145 Operating expenses 764,776 704,577 Excess of revenue over expenses 35,433 41,444 Nonoperating gains (lesses) Contributions, gifts, and bequests 3,189 1,318 Net assets released from restrictions for research expenditures 14,070 14,474 Research, education, and other nonoperating expenses (22,980) (24,773) Change in interest rate swap value and put agreements 1,578 9,397 Investment income 30,453 18,402 26,310 18,818 Excess of revenues and gains over expenses and losses $61,743 $60.262 TABLE 9A-3 Harris Memorial Hospital and Harris Community Foundation Combined Statements of Changes in Net Assets (in Thousands) December 31, 20X7 December 31, 20X6 Unrestricted net assets Excess of revenues and gains over expenses and losses $61,743 $60,262 Net assets released from restrictions for capital expenditures 119 239 of 586 Cumulative effect of change in accounting principle (3,943) Increase in unrestricted net assets 61,743 56,438 Temporarily restricted net assets Contributions, gifts, and bequests 20,435 15,512 Investment income 8,455 3,972 Net assets released from restrictions for research expenditures (14,070) (14,474) Net assets released from restrictions for capital expenditures (119) Increase in temporarily restricted net assets 14,820 4,891 Permanently restricted net assets Contributions, gifts, and bequests 1,794 3,218 Increase in permanently restricted net assets 1,794 3,218 Net assets at beginning of year 606,262 541,715 Net assets at end of year $684,619 $606,262 TABLE 9A-4 Harris Memorial Hospital and Harris Community Foundation Combined Statements of Cash Flows in Thousands) December 31, 20X7 December 31, 20X6 Operating activities $78,357 $ 64,547 Increase in nel assets Adjustments to reconcile increase in net assets to net cash provided by operating activities (26,358) 11,432 Change in net unrealized gains and losses on investment securities (3,943) Cumulative effect of change in accounting principle 44,392 41,627 Depreciation (6,119) Gain on sale or disposal of assets, net 55,851 57,975 Provision for bad debts (1,578) (9,397) Change in interest rate swap value and put agreements (continues TABLE 9A-4 Harris Memorial Hospital and Harris Community Foundation Combined Statements of Cash Flows in Thousands) (continued) December 31, 20X7 December 31, 20X6 Changes in operating assets and liabilities Assets limited as to use (19,779) (14,274) Accounts receivable (65,937) (51,251) Other assets (7,071) (43) Supplies (415) 840 Accounts payable 7,941 10,613 Accrued expenses and other liabilities 20,568 8,430 Due to third-party payers (5,253) (4,877) Contingent professional liabilities (15,227) 3,743 Postretirement benefit obligation, other thari pensions 513 456 Net cash provided by operating activities 59,885 115,878 Investing activities Property and equipment acquired (142,793) (159,943) Cash used in investing activities (142,793) (159,943) Financing activities Repayment of long-term debt (177,294) (5,545) Proceeds from borrowing 283,321 57,614 106,027 52,069 Net cash provided by financing activities 23,119 8,004 Net increase in cash and cash equivalents 59,696 51,692 Cash and cash equivalents at beginning of ye $82,815 $59,696 Cash and cash equivalents at end of year Harris Memorial Hospital and Harris Community Foundation Notes to Combined Financial Statements December 31, 20X7 1. Organization and Significant Accounting Policies Organization and Basis of Combination Harris Memorial Hospital (the Hospital) and Har- ris Community Foundation (the Foundation) are a hospital and charitable foundation located in Jersey, Ohio. The Hospital and Foundation are exempt from federal income taxes under Section 501(c)(3) of the Internal Revenue Code (IRC). The Hospital and Foundation are collectively referred to herein as the Foundation, The Foundation owns and operates the Renee Center, which has 27 skilled nursing beds; Harris Assurance, Ltd. (Assurance), a for-profit, wholly owned insurance subsidiary; and Harris Properties (Condit Inn), a for-profit, wholly owned subsidi- ary. During 20X6, the Foundation formed the Har- ris Community Hospital Corporation (dba Harris Hospital) located in Oldstone, Ohio and the Harris Long Term Acute Care Hospital Corporation (dba Harris Continuing Care Hospital) located in Jersey, Ohio. The 60-bed Harris Continuing Care Hospi- tal opened in May 20X7. Harris Hospital, with 92 beds, opened in late July 20X7. At December 31, 20x7, the Foundation has remaining commitments totaling approximately $7,360,000 under construc- tion contracts for these and other capital projects. The Foundation is affiliated with the Harris Health Plan (the Health Plan). The Health Plan's financial statements are not included in these combined financial statements. The Foundation provides healthcare services in the central Ohio region. All appropriate intercompany accounts have been eliminated in combination. Cash Equivalents The Foundation considers all undesignated highly liquid investments with maturities of 3 months or less when purchased to be cash equivalents. Supplies Supplies are stated at cost (first-in, first-out method), which is not in excess of market value. patient accounts receivable were 20% and 19% at December 31, 20X7 and 20X6, respectively, from government-related programs. Patient accounts receivable from the Health Plan were 25% and 29% at December 31, 20X7 and 20X6, respectively. The Foundation maintains allowances for uncollectable accounts for estimated losses result ing from a payer's inability to make payments on accounts. The Foundation uses a balance sheet approach to value the allowance account based on historical write-offs,payer type, and the aging of the accounts. Accounts are written off when collection efforts have been exhausted. Management contin- ually monitors and adjusts, as necessary, allow- ances associated with its receivables. The majority of uncollectable accounts are from uninsured and the patient portion of accounts receivable. Assets Limited as to Use Assets limited as to use at December 31, 20X7, include 76% and 9% held under master trust agreements with Liberty Fagle Trust and Highbanks, respectively, and 15% held in government-insured time deposits and other financial instruments. Assets limited as to use at December 31, 20X6, include 78% and 5% held under master trust agree- ments with Liberty Eagle Trust and Highbanks, respectively, and 17% held in government-insured time deposits and other financial instruments. The investments held under the master trust agree- ments are diversified among equity, debt, and money market instruments and are reported at estimated fair value. The fair value of these invest- ments is generally based on quoted market prices on national exchanges. Property and Equipment Property and equipment are recorded at cost at the date of acquisition or estimated fair value at the date of donation. Depreciation is computed on the straight-line method using the estimated economic lives of the depreciable assets, gener- ally ranging from 3 to 40 years. Expenditures that materially increase values, change capacities, or extend useful lives are capitalized. Routine main- tenance and repair items are charged to operating expenses. The Foundation evaluates whether events and circumstances have occurred that indicate the remaining estimated useful life of long-lived assets may warrant revision or that the remaining balance of an asset may not be recoverable. The assessment of possible impairment is based on Patient Accounts Receivable Patient accounts receivable are stated at estimated net realizable value. Significant concentrations of whether the carrying amount of the asset exceeds the expected total undiscounted value of cash flows expected to result from the use of the assets and their eventual disposition. No amounts were recognized in 20X6. In 20X7, the Foundation recorded a charge of $4,000,000, net of reimbursement, for unrecover- able costs incurred in connection with repair and maintenance costs of the Condit Inn. Derivative Financial Instruments The Foundation accounts for its derivatives under Statement of Financial Accounting Stan- dards No. 133, Accounting for Derivative Instru- ments and Hedging Activities, or SFAS No. 133. SFAS No. 133 requires that all derivative finan- cial instruments that qualify for hedge account- ing be recognized in the financial statements and measured at fair value regardless of the purpose or intent for holding them. Changes in the fair value of derivative financial instruments are rec- ognized periodically either in operations or in changes in unrestricted net assets. The Founda- tion's policy is to not hold or issue derivatives for trading purposes and to avoid derivatives with leverage features. Restricted Support The Foundation records unconditional promises of cash or other assets at estimated fair value on the date the promises are received. The Foun- dation reports gifts of cash and other assets as restricted support if they are received with donor stipulations that limit the use of the donated assets. When a donor restriction expires, that is, when a stipulated time restriction ends or a purpose of restriction is accomplished, temporarily restricted net assets are reclassified to unrestricted net assets and reported in the combined statements of oper- ations or combined statements of changes in net assets (based on nature of restriction) as net assets released from restrictions. The Foundation reports gifts of land, build- ings, and equipment as unrestricted support unless explicit donor stipulations specify how the donated assets must be used. Gifts of long- lived assets with explicit restrictions that specify how the assets are to be used and gifts of cash or other assets that must be used to acquire long- lived assets are reported as restricted support. The Foundation reports expirations of donor restric- tions when the donated or acquired long-lived assets are placed in service. Permanently restricted net assets have been restricted by donors to be maintained by the Foundation in perpetuity. The income from permanently restricted net assets is recorded as unrestricted unless explicitly restricted by donors. Donor-restricted income on permanently restricted net assets is generally available to sup- port research and education and is reported as temporarily restricted. The Foundation's temporarily restricted net assets are restricted primarily for research, educa- tion, capital projects, and medical care programs and its permanently restricted net assets are pri- marily restricted for endowment purposes. Net Patient Service Revenue Net patient service revenue is reported at esti- mated net realizable amounts from patients, third-party payers, and others for services ren- dered and includes estimated retroactive revenue adjustments due to future audits, reviews, and investigations. Retroactive adjustments are con- sidered in the recognition of revenue on an esti- mated basis in the period the related services are rendered, and such amounts are adjusted in future periods as adjustments become known or as years are no longer subject to such audits, reviews, and investigations. Charity Care The Foundation provides care without charge or at amounts less than its established rates to patients who meet certain criteria under its charity policy. Because the Foundation does not pursue collec- tion of amounts determined to qualify as charity care, they are not reported as revenue. Hospital charges foregone for charity care, based on estab- lished rates, were approximately $35,200,000 in 20X7, prior to application of disproportion- ate share funds of approximately $4,800,000 received from the State of Ohio, and $35,300,000 in 20X6, prior to application of disproportionate share funds of approximately $5,800,000 received from the State of Ohio. Clinic charges forgone for charity care, based on established rates, were $12,525,000 and $10,216,000 in 20X7 and 20X6, respectively. Health Insurance Program Reimbursement Revenue from the Medicare and Medicaid pro- grams accounted for approximately 45% and 8%, respectively, of the Foundation's net patient service revenue for the year ended December unrealized gains and losses on investments other than trading investment securities, and invest- ment returns restricted by donors. Use of Estimates The preparation of financial statements in con- formity with accounting principles generally accepted in the United States requires manage- ment to make estimates and assumptions that affect the amounts reported in the combined financial statements and accompanying notes. Actual results could differ from those estimates. 31, 20X7, and 51% and 11%, respectively, for the year ended December 31, 20X6. Laws and reg- ulations governing the Medicare and Medicaid programs are extremely complex and are subject to interpretation. Federal regulations require the submission of annual cost reports covering med ical costs and expenses associated with services provided to program beneficiaries. Medicare and Medicaid cost report settlements are estimated in the period services are provided to benefi- ciaries. As a result, there is at least a reasonable possibility that recorded estimates will change by a material amount in the near term. The 20X7 and 20X6 net patient service revenue increased (decreased) approximately $10,340,000 and $(1,332,000), respectively, due to changes in allowances previously estimated as a result of the final settlements for years that are no longer subject to audits, reviews, and investigations. The Foundation believes that it is in compli- ance with all applicable laws and regulations and is not aware of any pending or threatened investigations involving allegations of potential wrongdoing Medicare cost reports filed by the Hospital for all years before 20X4 have been audited and settled as of December 31, 20X7. Medicare cost reports filed by the Clinic for all years before 20x0 have been audited and settled as of December 31, 20X7. Amounts due to the Medicare and Medic- aid programs totaled approximately $7,380,000 and $12,633,000 at December 31, 20X7 and 20X6, respectively, and are included in due to third- party payers in the accompanying combined bal- ance sheets. Nonoperating Gains and Losses Nonoperating gains and losses include unre- stricted contributions, gifts and bequests, interest earnings on investments, net assets released from restrictions for research and education expendi- tures (net of contributions for such expenditures), change in interest rate swap value and put agree- ments, and other gains and losses unrelated to the Foundation's primary operations, Excess of Revenues and Gains over Expenses and Losses Included in excess of revenues and gains over expenses and losses in the accompanying com- bined statements of operations are all changes in unrestricted net assets other than net assets released from restrictions for capital expenditures, Other Certain reclassifications of donor trust liabilities, previously included in assets limited as to use, were made to the 20x6 combined financial state- ments to conform to the 20x7 presentation. Additionally, in previous years, the Foun- dation's investment portfolio (see Note 7) was classified as other than trading. As such, unreal- ized gains and losses that were considered tem- porary were excluded from excess of revenues and gains over expenses and losses. During fiscal year 20X7, the Foundation determined that substantially all of its investment portfolio was more accurately classified as trading with unrealized gains and losses included in excess of revenues and gains over expenses and losses. Therefore, a reclassification was made in the accompanying 20X6 combined financial state- ments to reflect this change in classification. A net unrealized loss of approximately $9,183,000 was reclassified from change in net unrealized gains and losses on investment securities to investment income. 2. Contingent Professional Liabilities The Foundation self-insures substantially all of its professional liability risk through its wholly owned insurance subsidiary. A commercial insur- ance policy is maintained to insure claims exceed- ing $7,000,000 individually or $35,000,000 in the aggregate in 20X7 on a claims-made basis. Con- tingent professional liabilities are recorded for incurred but not reported claims and reported claims based on estimates by independent actu- aries. Management established a fund for the purpose of setting aside assets based on estimates made by independent actuaries, and these funds are reported in the combined balance sheets as assets limited as to use. TABLE 9A-5 Property and Equipment and Related Accumulated Depreciation (in Thousands) December 31, 20X7 December 31, 20X6 $26,945 $26,610 Land and improvements 447,897 265,965 Buildings and improvements expenditures 469,441 427,882 Fixed and movable equipment 112,880 189,807 Construction-in-progress 1,057,163 910,264 493,814 451,435 Less accumulated depreciation $563,349 $458,829 4. Long-Term Debt In July 20X7, the Foundation issued the Series 20X7 LTACH Revenue Bonds totaling $15,700,000. The Series 20X7 LTACH Revenue Bonds are due July 20X2 with principal and interest payments due monthly. Interest accrues at 65% of LIBOR plus 100 basis points. Effective with the issuance of the bonds, the Foundation entered into a fixed rate swap agreement for the amount of the bonds by which the Foundation pays a fixed rate of interest of 4.55%. The change in fair value for the period ended December 31, 20X7 was not significant to the increase in net assets. In November 20X6, the Foundation issued Series 20X6 Revenue Bonds with a par amount of $233,350,000. Proceeds were used to advance refund $31,280,000 of the Series 20XOA Revenue Bonds, current refund $58,410,000 of the Series 20X1 Revenue Bonds, and finance and/or refi- nance expansion projects. The Series 20X6 Bonds were issued as Auction Rate Securities and gen- erally bear interest for successive 7-day auction periods at interest rates determined through Dutch auctions on the business day preceding the auction period. Any series or subseries of the Series 20X6 Revenue Bonds may be converted at the option of the Foundation, subject to certain restrictions, to bonds that bear interest in differ- ent rate periods, including daily, weekly, flexible, term, or fixed rate periods. The Series 20X6 Rev- enue Bonds contain certain restrictive covenants, including minimum levels of debt service cover- age. Management believes the Foundation is in compliance with all covenants TABLE 9A-6 Long-Term Debt (in Thousands) December 31, 20X7 December 31, 20X6 $15,679 Revenue bonds, LTACH Series 20X7; interest at 65% of LIBOR plus 100 basis points (4.647% at December 31, 20X7); principal and interest payable monthly through July 20X2 42,375 Revenue bonds, Series 20X6A 1; interest accrues for successive 7-day auction periods at interest rates determined through Dutch auctions (3.800% at December 31, 20X7) 42,400 Revenue bonds, Series 20X6A-2; interest accrues for successive 7-day auction periods at interest rates determined through Dutch auctions (3.800% at December 31, 20X7) 56,550 Revenue bonds Series 20X6B;interest accrues for successive 7-day auction periods at interest rates determined through Dutch auctions (3.850% at December 31, 20X7) 55,275 Revenue bonds, Series 20X6C; interest accrues for successive 7-day auction periods at interest rates determined through Dutch auctions (3.850% at December 31, 20X7) 36,750 Revenue bonds, Series 20X6D; interest accrues for successive 7-day auction periods at interest rates determined through Dutch auctions (3.900% at December 31, 20X7) 90,360 151,800 Revenue bonds. Series 20X1; interest accrues at a daily rate determined by the remarketing agent (3.960% at December 31, 20X7); interest and principal payable annually through 20X1 (principal payments began in 20X6) 2,700 35,230 Revenue bonds, Series 20XOA: Interest at 5.375%; interest and principal payable annually through 20X9 83,200 84,500 Revenue bonds, Series 20X0B; interest accrues at a daily rate determined by the remarketing agent (3.960% at December 31, 20x7); interest and principal payable annually through 20X9 19,000 46,686 Line of credit 7,000 Interim construction loan 13,046 Other 444,289 338,262 4,692 5,908 Less current maturities $439,597 $332,354 In January 20X6, the Foundation entered into a revolving line of credit with Bank of Central Ohio to fund interim construction costs and provide for liquidity and other short-term needs. In accordance with terms of the loan agreement, the total available for borrowing was decreased from $70,000,000 to $30,000,000 30 days following the issuance of the Series 20X6 Revenue Bonds. The total amount drawn as of December 31, 20X7 was $19,000,000. Interest is payable quarterly at a rate equal to the lesser of the maximum lawful LIBOR plus 15 basis points (5.71% at December 31, 20X7). Amounts drawn are due in full June 25, 20X9. The Foundation issued Series 20X1 Revenue Bonds with a par amount of $158,000,000 that were partially refunded in November 20X6. The net proceeds were used to fund expansion projects. The Foundation issued Series 20XOA Rev- enue Bonds with a par amount of $42,025,000 that were partially refunded in November 20x6 and Series 20XOB Revenue Bonds with a par amount of $91,200,000. The majority of the proceeds from the Series 20X0A and Series 20XOB Revenue Bonds were used to refund the current Series 19X8 Revenue Bonds with an outstanding balance of $19,147,000 and a note payable with an outstanding par amount of $88,000,000 The Series 20XOA and Series 20XOB Revenue Bonds and the Series 20X1 Revenue Bonds con- tain certain restrictive covenants, including mini- mum levels of debt service coverage. Management believes the Foundation is in compliance with all covenants. respectively. Interest paid during fiscal 20X7 and 20X6 was $16,937,249 and $9,084,500, respec- tively, net of amounts capitalized. 5. Concentrations of Credit Risk Harris Memorial grants credit without collateral to its patients, most of whom are local residents and are insured under third-party payer agree- ments. The mix of receivables from patients and third-party payers was as follows: TABLE 9A-7 Mix of Receivables December 31, December 31, 20X7 20X6 The Series 20XOB Revenue Bonds and the Series 20X1 Revenue Bonds are variable rate bonds in a daily mode and can be tendered by holders upon demand. A remarketing agent selected by the Foundation determines the inter- est rates and remarkets both series of bonds The Series 20XOB Revenue Bonds and the Series 20X1 Revenue Bonds are supported by Standby Bond Purchase Agreements (the Agreements) with liquidity providers pursuant to which the providers will purchase any bonds the remar- keting agent is unable to market. The termina- tion date of the two Agreements related to the Series 20XOB Revenue Bonds was December 6, 20X7. On October 18, 20X7, these Agreements were extended to December 4, 20X8. There are also two Agreements associated with the Series 20X1 Revenue Bonds. The termination date of the first Agreement related to the Series 20X1 Revenue Bonds was December 6, 20X7, and on October 18, 20X7, was extended to December 4, 20X8. The termination date of the second Agreement related to the Series 20X1 Revenue Bonds is December 15, 20X5, as extended in November 20X4. All Agreements include cov- enants that are customary in credit agreements of this nature. Repayment of bonds purchased under the Agreements is subject to a 5-year pay- out beginning July 20X6, if other liquidity facil- ities, as defined in the bond agreements, are not executed. The maturities of long-term debt, net of unamortized premium, as of December 31, 20X7, are shown below (in thousands): Medicare 21% 19% Medicaid 2 2 Major payer 1 15 15 Major payer 2 11 11 Major payer 3 11 13 28 28 Other third party payers Privale pay 12 12 Total 100% 10096 20x8 $4,692 20XG 23,902 20X0 5,136 20X1 5,353 20X2 19,896 6. Interest Rate Swap Agreements Effective December 20X1, the Foundation entered into an interest rate swap agreement with an ini- tial notional amount of $150,000,000. The interest rate swap agreement converts a notional amount of $150,000,000 of floating rate borrowings to fixed rate borrowings. The Foundation pays a fixed rate of interest (5.17%) and receives, from the counterparty, a variable rate of interest based on the SIFMA Municipal Swap Index (SIFMA Index) on the outstanding principal balance of the Series 20X1 Revenue Bonds until 2031. The Foundation has elected not to apply hedge accounting: therefore, the change in fair value is included in nonoperating (gains) losses. The fair value of the interest rate swap at December 31, 20X7 and 20X6, is a liability of approximately $9,498,000 and $16,530,000, respectively, and is included in due to broker in the accompanying Thereafter 385,310 $444,289 Total interest costs incurred during fiscal 20X7 and 20x6 were $16,779,140 and $9,339,000 respectively, including $5,805,140 and $3,194,000 of capitalized interest costs in 20X7 and 20X6, Appendix 9-A 237 combined balance sheets. The change in the fair value of the interest rate swap is included in non- operating gains (losses) and totaled approximately $(7,032,000) and $(6,885,000) for the years ended December 31, 20X7 and 20X6, respectively. The change in fair value for the year ended December 31, 20X7 includes the amendment fee paid to the counterparty of $7,037,000, realized as a part of the Series 20X1 Revenue Bond refunding. Simultaneous with entering into the interest rate swap agreement, the Foundation also entered into a put agreement with the counterparty. The counterparty may exercise this put agreement if the daily weighted average of the SIFMA Index is greater than 7.00% for the 180-day period end- ing on the day the counterparty exercises the put option. Under this agreement, the Founda- tion pays a variable rate of interest, based on the SIFMA Index, on the outstanding principal bal- ance of the proposed bonds until 2031. For this put agreement, the counterparty pays the Founda- tion an annual premium of 77.30 basis points on an initial notional amount of $150,000,000 over the term of the put agreement, for a net effective combined annual payment by the Foundation to the counterparty for the swap agreement and the put agreement of approximately 4.39%. The pre- mium payment, however, will cease upon exer- cise of the put agreement. This put agreement, if exercised, will offset the cash flows of the interest rate swap agreement noted above. The fair value of the put agreement at December 31, 20X7 and 20X6, is an asset of $4,200,000 and $7,016,000, respectively, and has been included in other assets. The change in the fair value of S(2,816,000) and $(552,000) for the years ended December 31, 20X7 and 20X6, respectively, has been included in nonoperating gains (losses) since the put agree- ment is not a hedge and must be adjusted to fair value through the performance indicator. A por- tion of the change in fair value for the year ended December 31, 20X7 includes the amount related to the partial refunding of the Series 20X1 Reve- nue Bonds. The amendment fee received from the counterparty was $2,005,000. On October 30, 20X2, the Foundation entered into an interest rate swap agreement with an ini- tial notional amount of $96,400,000 ($88,400,000 Series 20X0A and Series 20X0B and $8,000,000 Series 20X1). The interest rate swap agreement converts a notional amount of $96,400,000 of float- ing rate borrowings to fixed rate borrowings. The Foundation pays a fixed rate of interest (4.34)% and receives, from the counterparty, a variable rate of interest based on the SIFMA Index on the out- standing principal balance of the Revenue Bonds until 2031. The Foundation has elected not to apply hedge accounting; therefore, the change in fair value is included in nonoperating (gains) losses. The fair value of the interest rate swap at December 31, 20X7 and 20X6, is a liability of approximately $3,020,000 and $3,078,000, respectively, and is included in due to broker in the accompanying combined balance sheets. The change in the fair value of the inter- est rate swap is included in nonoperating gains (losses) and totaled approximately $(58,000) and $(3,639,000) for the years ended December 31, 20X7 and 20X6, respectively. The change in fair value includes the amendment fee of $176,000 paid to the counterparty to terminate the portion of the interest rate swap agreement associated with the Series 20x1 Revenue Bonds. Simultaneous with entering into the interest rate swap agreement, the Foundation also entered into a put agreement with the counterparty. The counterparty may exercise this put agreement if the daily weighted average of the SIFMA Index is greater than 6.00% for the 180-day period ending on the day the counterparty exercises the put option. Under this agreement, the Foundation pays a variable rate of interest, based on the SIFMA Index, on the outstanding principal balance of the related bonds until 2031. For this put agreement, the counterparty pays the Foun- dation an annual premium of 110.10 basis points on an initial notional amount $96,400,000 over the term of the put agreement, for a net effective com- bined annual payment by the Foundation to the counterparty for the swap agreement and the put agreement of approximately 3.24%. The premium payment, however, will cease upon exercise of the put agreement. This put agreement, if exercised, will offset the cash flows of the interest rate swap agreement noted above. The fair value of the put agreement at December 31, 20X7 and 20X6, is an asset of approximately $4.970,000 and $5,056,000, respectively, and has been included in other assets. This change in fair value of $(86,000) and $(575,000) for the years ended December 31, 20X7 and 20X6, respectively, has been included in non- operating gains (losses) since the put agreement is not a hedge and must be adjusted to fair value through the performance indicator. The change in fair value includes the amendment fee of $198.000 received from the counterparty to terminate the portion of the put agreement associated with the Series 20X1 Revenue Bonds. In anticipation of the issuance of the Series 20x6 Bonds, the Foundation entered into five inter- est rate swap transactions in October 20X6 with an initial notional amount totaling $233,350,000. The swap transactions serve to substantially fix the expected net interest expense associated with the Series 20x6 Bonds by converting float- ing rate borrowings with a notional amount of $233,350,000 to fixed rate borrowings. For the swaps related to the Series 20X6A and 20X6B Bonds, the Foundation pays a fixed rate of 3.502% per annum, and the counterparty pays a vari able rate of interest at a rate equal to 57.4% of the 1-month LIBOR rate plus a spread of 0.33%. For the swaps related to the Series 20X6C Bonds and 20X6D Bonds, the Foundation pays a fixed rate of 3.496% per annum, and the counterparty pays a variable rate of interest at a rate equal to 57.4% of the 1-month LIBOR rate plus a spread of 0.33%. The Foundation has elected not to apply hedge accounting; therefore, the change in fair value is included in nonoperating (gains) losses. The fair value of the interest rate swaps at December 31, 20X7 is a liability of approximately $2,610,000, which equates to the change in fair value from inception of the swaps through the year ended December 31, 20X7. The Foundation can terminate any of these agreements at any time at current market value. The Foundation would make or receive a pay- ment depending on market value on the date of termination. The Foundation is exposed to credit losses in the event of nonperformance by the counterparty to the agreements. The counterparty is a credit- worthy financial institution, and the Foundation anticipates that the counterparty will be able to fully satisfy its obligation under the agreements. 7. Pension Plans The Foundation implemented a 401(a) defined contribution plan and a 403(b) voluntary savings plan covering substantially all employees. The Foundation contributes from 6% to 13% of par- ticipating employees' compensation. Prior to Jan- uary 1, 20X6, the Foundation's contributions were based on participating employees' age. The plan was amended January 1, 20X6 and these contribu- tions are now based on years of service. The Foun- dation's contribution expense was approximately $28,495,000 and $26,121,000 in 20X7 and 20X6, respectively. The Foundation sponsors a defined benefit postretirement plan that provides medical and dental benefits to retirees who meet specific eli- gibility requirements upon termination of active service. The plan is unfunded and requires cov- ered retirees to contribute a portion of the cost of benefits. The Foundation uses an incremental cost approach in estimating the annual accrued cost related to postretirement benefits other than pensions, which is based on estimates by indepen- dent actuaries. Such an approach is considered appropriate since substantially all of the health- care benefits are provided by the Foundation to retirees, using the Health Plan to manage the care provided. Plan expenses incurred by the Foun- dation were $880,000 and $822,000 for the years ended December 31, 20X7 and 20X6, respectively. 8. Assets Limited as to Use Certain cash and investments, where their use is limited due to board designations or other pur- poses as set forth below, are reported as assets lim- ited as to use. The carrying values (in thousands) are at estimated fair values, which are summarized in TABLE 9A-8. es war nuen the years TABLE 9A-8 Assets Limited as to Use December 31, 20X7 December 31, 20X6 Assets limited as to use and long-term investments $84,440 $67,826 For donar restricted purposes, such as research, lectureships, and capital projects Board designated for specific purposes 133,028 118,618 Funded depreciation 33,357 46,566 Contingent professional liabilities 18,072 16,241 Institutional research 19,925 16,019 Investments held by subsidiary 178,453 180,969 Other board designated 382,835 378,413 51,038 25,937 Held by trustees under bond agreements 518,313 472,176 5,327 5,088 Less current portion of assets limited as to use $512,986 $467,088 Investment income or loss is included in the excess of revenues and gains over expenses and losses, and includes realized and unrealized gains and losses, interest, and dividends. 9. Commitments and Contingencies The Foundation leases equipment and a medi- cal office building under operating leases. These payments are due monthly through Decem- ber 2012. Rent expense totaled approximately $7,426,000 and $8,715,000 in 20X7 and 20X6, TABLE 9A-9 The Foundation's Assets Limited as to Use at December 31 (in Thousands) respectively. December 31, December 31, 20X7 Future minimum lease commitments under operating leases that have initial or remaining lease terms in excess of 1 year are as follows as of December 31, 20X7 (in thousands): 20X6 Carried at fair value $83,900 $58,833 Money market accounts 20X8 $3,410 20x9 3,544 1,651 2,151 Certificates of deposit 20X0 3,252 U.S. Treasury securities 74,896 75,195 20X1 2,886 2,287 20X2 53,412 82,657 Corporate debt securities $15,379 Equity securities 304,454 253,340 518,313 472,176 5,327 5,088 Less current portion of assets limited as to use Sale of Medical Office Building On December 29, 20X7, the Foundation sold a medical office building to Ross Acquisition of Alexandria (RA) for approximately $22,200,000. The building had a book value of approximately $10,900,000. The transaction included a ground lease with a term of 50 years and HR prepaid $512,986 $467,088 the rent totaling approximately $900,000. The Foundation entered into lease-back agreements for space within the building. The Foundation recognized an immediate gain of approximately $6,100,000 and a deferred gain of approximately $4,300,000 to be recognized over a period equal to the operating lease term. Other The Foundation is a defendant in various legal proceedings arising in the ordinary course of business. Although the results of litigation cannot be predicted with certainty, management believes the outcome of pending litigation will not have a material adverse effect on the Foundation's com- bined financial statements. On February 21, 20X3, the Foundation entered into a 10-year Master Customer Agree- ment with COTC, for the provision of services, supplies, and equipment. The agreement pro- vides a platform for the development of the Zuber Center as a fully integrated, all-digital facility. COTC will support the Foundation in five core areas: healthcare information technology appli- cations and infrastructure, medical equipment, telecommunications power, and "smart" build- ing technologies. The agreement provides for a commitment of approximately $200,000,000 from the Foundation to purchase certain goods and services at favorable prices. The Foundation has certain minimum yearly purchase commitments ranging from $10,000,000 to $25,000,000 over the 10-year term of the agreement. For the years ended December 31, 20X7 and 20X6, the Foun- dation purchased approximately $22,353,000 and $26,372,000, respectively, in goods and services from Siemens and affiliated companies, which exceeded the purchase commitments in those years. Goods and services purchased under the contract total approximately $137,400,000. The Foundation invests in short-term instru- ments as part of its money management program. These instruments include short-term govern- ment securities and investment grade commer- cial paper. Generally, an investment firm on behalf of the Foundation manages these invest- ments, and the Foundation has invested in a num- ber of short-term investment grade commercial papers over the years. On October 29, 20X1, the Foundation sold approximately $10,000,000 in MGMTMatrix commercial paper prior to matu- rity. MGMTMatrix filed a voluntary petition for relief under Chapter 11 on February 17, 20X1. On October 6, 20X3, the Foundation learned that the bankruptcy counsel for MGMT Matrix filed, in U.S. Bankruptcy Court in the District of New York, an attempt to nullify the redemp- tion of certain MGMTMatrix commercial paper including that divested by the Foundation. The case was settled in December 20X7 for approx- imately $3,900,000 and is included in accrued expenses and other liabilities in the accompany- ing combined balance sheets. The Foundation paid the settlement amount in October 20X7. 10. Fair Values of Financial Instruments Generally accepted accounting principles estab- lished a framework for measuring fair value that provides a fair value hierarchy that prioritizes the inputs to valuation techniques used to measure fair value. The hierarchy gives the highest prior- ity to unadjusted quoted prices in active markets for identical assets or liabilities (Level 1 measure- ments) and the lowest priority to unobservable inputs (Level 3 measurements) The three levels of the fair value hierarchy under Accounting Standar Codification (ASC) 820-10-50, Fair Value Measurement-Overall, are described here: Level 1: Valuation is based on quoted prices for identical instruments traded in active markets. Level 1 securities include primarily overnight repurchase agreements, money market funds, and mutual funds. Level 2: Valuation is based on quoted prices for similar instruments in active markets, quoted prices for identical or similar instruments in markets that are not active, and model-based valuation techniques for which all significant assumptions are observable in the market. At Level 2 securities include an unregistered mutual fund. Level 3: Valuation is generated from model-based techniques that use significant assumptions not observable in the market. These unobservable assumptions reflect the Hospital's estimates of assumptions that market participants would use in pricing the asset or liability. Valuation techniques include use of discounted cash flow models and similar techniques. Level 3 securi- ties include an equity fund limited partnership. Fair value is based on the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date. The Hos- pital maximizes the use of observable inputs and minimizes the use of unobservable inputs when developing fair value measurements. Fair value measurements for assets and lia- bilities where there is limited or no observable market data and, therefore, are based primarily on estimates calculated by the Hospital, are based on the economic and competitive environment, the characteristics of the asset or liability and other factors. Therefore, the results cannot be determined with precision and may not be real- ized upon an actual settlement of the asset or lia- bility. There may be inherent weaknesses in any calculation technique, and changes in the under- lying assumptions used, including discount rates and estimates of future cash flows that could significantly affect the results of the current or future values. The following methods and assumptions were used by the Foundation in estimating the fair value of its financial instruments: Cash and cash equivalents: The carrying amount reported in the combined balance sheet for cash and cash equivalents approximates its fair value. Investments: Fair values, which are the amounts reported in the combined balance sheet, are based on quoted market prices. Interest rate swap agreements: Fair values, which are the amounts reported in the combined bal- ance sheet as due to broker and other assets, are based on market rates. Long-term debt: The carrying amount of the Foundation's borrowings under its revolving line of credit and auction rate security bond issues approximates fair value. The fair value of the Foundation's other long-term debt is esti- mated using discounted cash flow analyses, based on the Foundation's current incremental borrowing rates for similar types of borrowing arrangements. 11. Functional Expenses The Foundation provides healthcare services to residents within its geographical service area. TABLE 9A-10 The Carrying Amounts and Fair Values of the Foundation's Financial Instruments in the combined Balance Sheets at December 31 (in Thousands) Carrying Amount Fair Value 20X7 Cash and cash equivalents $82,815 $82,815 Assets limited as to use 518,313 518,313 Due to broker 15,128 15,128 Long-term debt 444,289 444,349 20X6 Cash and cash equivalents $59,696 $59,696 Assets limited as to use 472,176 472,176 Due to broker 19,608 19,608 Long-term debt 338,262 340,809 242 Chapter 9 Financial Statements TABLE 9A-11 Expenses Related to providing These Services for the Years Ended December 31, 20X7 and 20X6 (in Thousands) December 31, 20X7 December 31, 20X6 Healthcare services $619,596 562,186 General and administrative 143,293 140,546 Fundraising 1,887 1,845 Total operating expenses $764,776 704,577 TABLE 13-7 Forecasted Financial Ratios for OHF 20X7 20X8 20X9 20X0 20X1 Profitability Total margin percentage 3.9 4.9 4.9 5.0 5.0 1.3 Operating margin percentage 2.3 20 1.7 1.4 2.6 2.9 3.0 3.2 3,5 Nonoperating revenue % ROE percentage 8.2 9.7 8.8 8.5 8,0 Liquidity Current 1.11 1.11 1.09 1.09 1.09 Days in accounts receivable 54.8 54.8 54.8 54.8 54.8 Days cash on hand (short term) 20.0 20.0 20.0 20.0 20.0 Capital structure Equity financing percentage 44.1 46.4 48.7 50.9 53.0 Long-term debt to equity % 63.3 55.6 49.1 43.2 38.4 Cash flow to debt percentage 14.9 17.4 18.0 18.8 19.6 Times interest earned 2.65 3.19 3.31 3.43 3.59 Activity Total asset turnover 0.93 0.91 0.89 0.87 0.85 Fixed asset turnover 2.32 2.37 2.43 2.52 2.63 Current asset turnover 4.44 4.44 4.44 4.44 4.44 Other ratios Average age of plant 8.8 9.3 9.7 102 10.7 high price structure, which it may not be able to maintain. A 2% growth rate is predicated on zero growth in net prices but a 2% growth in volume of services. A 2% growth in services seems reason- able given previous growth in outpatient and clinic services. The assumptions made about revenue growth (volume and price) are the most import- ant variables in terms of impact on the financial plan. Small changes in these assumtions can ham Salaries and wages: In the labor intensive healthcare industry the second most important assumption in any financial forecast is salaries and wages. Salary and wage cost are the product of three factors: Salary and wage costs = Volume of services Staffing ratios x Wage rates UIT Omega Health Foundation 20X7 Return on equity % 8.4 Operating margin % 1.3 Total asset turnover 0.93 Nonoperating revenue % 2.7 Equity financing % 0.44 FIGURE 13-4 Financial 338 of 586 mega Health Foundation provide a basis for our audit opinion. In our opinion, the financial statements referred to above present fairly, in all material respects, the combined financial position of Harris Memorial subsidiaries at December 31, 20X7 and 20X6, and the combined changes in their net assets and their cash flows for the years then ended in conformity with U.S. generally accepted accounting principles. TABLE 9A-1 Harris Memorial Hospital and Harris Community Foundation Combined Balance Sheets (in Thousands) December 31, 20X7 December 31, 20X6 Assets Current assets Cash and cash equivalents $82,815 $59,696 Assets limited as to use, current portion 5,327 5,088 Accounts receivable Patients, less allowance for doubtful accounts ($25,302 in 20X7 and $23,014 in 20X6) 70,025 59,939 Other 28,990 24,995 Supplies 7,078 6,663 Total current assets 194,235 156,381 Assets limited as to use For donor-restricted purposes 84,440 67,826 Board designated for specific purposes 382,835 378,413 Held by trustees under bond agreements 51,038 25,937 518,313 472,176 Less current portion 5,327 5,088 512,986 467,088 Property and equipment, net 563,349 458,829 Other assets 34,476 34,302 Total assets $1,305,046 $1,116,600 Liabilities and net assets Current liabilities Accounts payable $32,572 $24,631 Accrued expenses and other liabilities 58,878 53,725 Due to third-party payers 7,380 12,633 Current maturities of long-term debt 4,692 5,908 Total current liabilities 103,522 96,897 Long-term debt, less current maturities 439,597 332,354 Contingent professional liabilities 33,260 48,487 Due to broker 15,128 19,608 Other liabilities 20,713 5,298 Postretirement benefit obligation, other than pensions 8,207 7,694 Total liabilities 620,427 510,338 Net assets Unrestricted 538,436 Temporarily restricted 55,213 40,393 Permanently restricted 29,227 27,433 Total net assets 684,619 606,262 Total liabilities and net assets $1,305,046 $1,116,600 TABLE 9A-2 Harris Memorial Hospital and Harris Community Foundation Combined Statements of Operations (in Thousands) December 31, 20X7 December 31, 20X6 Operating revenues and other support $829,005 $774,662 Net patient service revenue (55,851) (57,975) Provision for doubtful accounts 773,154 716,687 Net patient service revenue less provision for doubtful accounts 27,055 29,334 Other operating revenue 800,209 746,021 Total operating revenue (continues) TABLE 9A-2 Harris Memorial Hospital and Harris Community Foundation Combined Statements of Operations (in Thousands) (continued) Operating expenses Salaries and wages $371,449 $329,668 Employee benefits 81,532 77,231 Supplies and purchased services 228,244 225,497 Advertising 3,072 2,376 Staff enrichment 10,767 8,591 Occupancy cost 14,346 13,442 Depreciation 44,392 41,627 Interest 10,974 6,145 Operating expenses 764,776 704,577 Excess of revenue over expenses 35,433 41,444 Nonoperating gains (lesses) Contributions, gifts, and bequests 3,189 1,318 Net assets released from restrictions for research expenditures 14,070 14,474 Research, education, and other nonoperating expenses (22,980) (24,773) Change in interest rate swap value and put agreements 1,578 9,397 Investment income 30,453 18,402 26,310 18,818 Excess of revenues and gains over expenses and losses $61,743 $60.262 TABLE 9A-3 Harris Memorial Hospital and Harris Community Foundation Combined Statements of Changes in Net Assets (in Thousands) December 31, 20X7 December 31, 20X6 Unrestricted net assets Excess of revenues and gains over expenses and losses $61,743 $60,262 Net assets released from restrictions for capital expenditures 119 239 of 586 Cumulative effect of change in accounting principle (3,943) Increase in unrestricted net assets 61,743 56,438 Temporarily restricted net assets Contributions, gifts, and bequests 20,435 15,512 Investment income 8,455 3,972 Net assets released from restrictions for research expenditures (14,070) (14,474) Net assets released from restrictions for capital expenditures (119) Increase in temporarily restricted net assets 14,820 4,891 Permanently restricted net assets Contributions, gifts, and bequests 1,794 3,218 Increase in permanently restricted net assets 1,794 3,218 Net assets at beginning of year 606,262 541,715 Net assets at end of year $684,619 $606,262 TABLE 9A-4 Harris Memorial Hospital and Harris Community Foundation Combined Statements of Cash Flows in Thousands) December 31, 20X7 December 31, 20X6 Operating activities $78,357 $ 64,547 Increase in nel assets Adjustments to reconcile increase in net assets to net cash provided by operating activities (26,358) 11,432 Change in net unrealized gains and losses on investment securities (3,943) Cumulative effect of change in accounting principle 44,392 41,627 Depreciation (6,119) Gain on sale or disposal of assets, net 55,851 57,975 Provision for bad debts (1,578) (9,397) Change in interest rate swap value and put agreements (continues TABLE 9A-4 Harris Memorial Hospital and Harris Community Foundation Combined Statements of Cash Flows in Thousands) (continued) December 31, 20X7 December 31, 20X6 Changes in operating assets and liabilities Assets limited as to use (19,779) (14,274) Accounts receivable (65,937) (51,251) Other assets (7,071) (43) Supplies (415) 840 Accounts payable 7,941 10,613 Accrued expenses and other liabilities 20,568 8,430 Due to third-party payers (5,253) (4,877) Contingent professional liabilities (15,227) 3,743 Postretirement benefit obligation, other thari pensions 513 456 Net cash provided by operating activities 59,885 115,878 Investing activities Property and equipment acquired (142,793) (159,943) Cash used in investing activities (142,793) (159,943) Financing activities Repayment of long-term debt (177,294) (5,545) Proceeds from borrowing 283,321 57,614 106,027 52,069 Net cash provided by financing activities 23,119 8,004 Net increase in cash and cash equivalents 59,696 51,692 Cash and cash equivalents at beginning of ye $82,815 $59,696 Cash and cash equivalents at end of year Harris Memorial Hospital and Harris Community Foundation Notes to Combined Financial Statements December 31, 20X7 1. Organization and Significant Accounting Policies Organization and Basis of Combination Harris Memorial Hospital (the Hospital) and Har- ris Community Foundation (the Foundation) are a hospital and charitable foundation located in Jersey, Ohio. The Hospital and Foundation are exempt from federal income taxes under Section 501(c)(3) of the Internal Revenue Code (IRC). The Hospital and Foundation are collectively referred to herein as the Foundation, The Foundation owns and operates the Renee Center, which has 27 skilled nursing beds; Harris Assurance, Ltd. (Assurance), a for-profit, wholly owned insurance subsidiary; and Harris Properties (Condit Inn), a for-profit, wholly owned subsidi- ary. During 20X6, the Foundation formed the Har- ris Community Hospital Corporation (dba Harris Hospital) located in Oldstone, Ohio and the Harris Long Term Acute Care Hospital Corporation (dba Harris Continuing Care Hospital) located in Jersey, Ohio. The 60-bed Harris Continuing Care Hospi- tal opened in May 20X7. Harris Hospital, with 92 beds, opened in late July 20X7. At December 31, 20x7, the Foundation has remaining commitments totaling approximately $7,360,000 under construc- tion contracts for these and other capital projects. The Foundation is affiliated with the Harris Health Plan (the Health Plan). The Health Plan's financial statements are not included in these combined financial statements. The Foundation provides healthcare services in the central Ohio region. All appropriate intercompany accounts have been eliminated in combination. Cash Equivalents The Foundation considers all undesignated highly liquid investments with maturities of 3 months or less when purchased to be cash equivalents. Supplies Supplies are stated at cost (first-in, first-out method), which is not in excess of market value. patient accounts receivable were 20% and 19% at December 31, 20X7 and 20X6, respectively, from government-related programs. Patient accounts receivable from the Health Plan were 25% and 29% at December 31, 20X7 and 20X6, respectively. The Foundation maintains allowances for uncollectable accounts for estimated losses result ing from a payer's inability to make payments on accounts. The Foundation uses a balance sheet approach to value the allowance account based on historical write-offs,payer type, and the aging of the accounts. Accounts are written off when collection efforts have been exhausted. Management contin- ually monitors and adjusts, as necessary, allow- ances associated with its receivables. The majority of uncollectable accounts are from uninsured and the patient portion of accounts receivable. Assets Limited as to Use Assets limited as to use at December 31, 20X7, include 76% and 9% held under master trust agreements with Liberty Fagle Trust and Highbanks, respectively, and 15% held in government-insured time deposits and other financial instruments. Assets limited as to use at December 31, 20X6, include 78% and 5% held under master trust agree- ments with Liberty Eagle Trust and Highbanks, respectively, and 17% held in government-insured time deposits and other financial instruments. The investments held under the master trust agree- ments are diversified among equity, debt, and money market instruments and are reported at estimated fair value. The fair value of these invest- ments is generally based on quoted market prices on national exchanges. Property and Equipment Property and equipment are recorded at cost at the date of acquisition or estimated fair value at the date of donation. Depreciation is computed on the straight-line method using the estimated economic lives of the depreciable assets, gener- ally ranging from 3 to 40 years. Expenditures that materially increase values, change capacities, or extend useful lives are capitalized. Routine main- tenance and repair items are charged to operating expenses. The Foundation evaluates whether events and circumstances have occurred that indicate the remaining estimated useful life of long-lived assets may warrant revision or that the remaining balance of an asset may not be recoverable. The assessment of possible impairment is based on Patient Accounts Receivable Patient accounts receivable are stated at estimated net realizable value. Significant concentrations of whether the carrying amount of the asset exceeds the expected total undiscounted value of cash flows expected to result from the use of the assets and their eventual disposition. No amounts were recognized in 20X6. In 20X7, the Foundation recorded a charge of $4,000,000, net of reimbursement, for unrecover- able costs incurred in connection with repair and maintenance costs of the Condit Inn. Derivative Financial Instruments The Foundation accounts for its derivatives under Statement of Financial Accounting Stan- dards No. 133, Accounting for Derivative Instru- ments and Hedging Activities, or SFAS No. 133. SFAS No. 133 requires that all derivative finan- cial instruments that qualify for hedge account- ing be recognized in the financial statements and measured at fair value regardless of the purpose or intent for holding them. Changes in the fair value of derivative financial instruments are rec- ognized periodically either in operations or in changes in unrestricted net assets. The Founda- tion's policy is to not hold or issue derivatives for trading purposes and to avoid derivatives with leverage features. Restricted Support The Foundation records unconditional promises of cash or other assets at estimated fair value on the date the promises are received. The Foun- dation reports gifts of cash and other assets as restricted support if they are received with donor stipulations that limit the use of the donated assets. When a donor restriction expires, that is, when a stipulated time restriction ends or a purpose of restriction is accomplished, temporarily restricted net assets are reclassified to unrestricted net assets and reported in the combined statements of oper- ations or combined statements of changes in net assets (based on nature of restriction) as net assets released from restrictions. The Foundation reports gifts of land, build- ings, and equipment as unrestricted support unless explicit donor stipulations specify how the donated assets must be used. Gifts of long- lived assets with explicit restrictions that specify how the assets are to be used and gifts of cash or other assets that must be used to acquire long- lived assets are re