Answered step by step

Verified Expert Solution

Question

1 Approved Answer

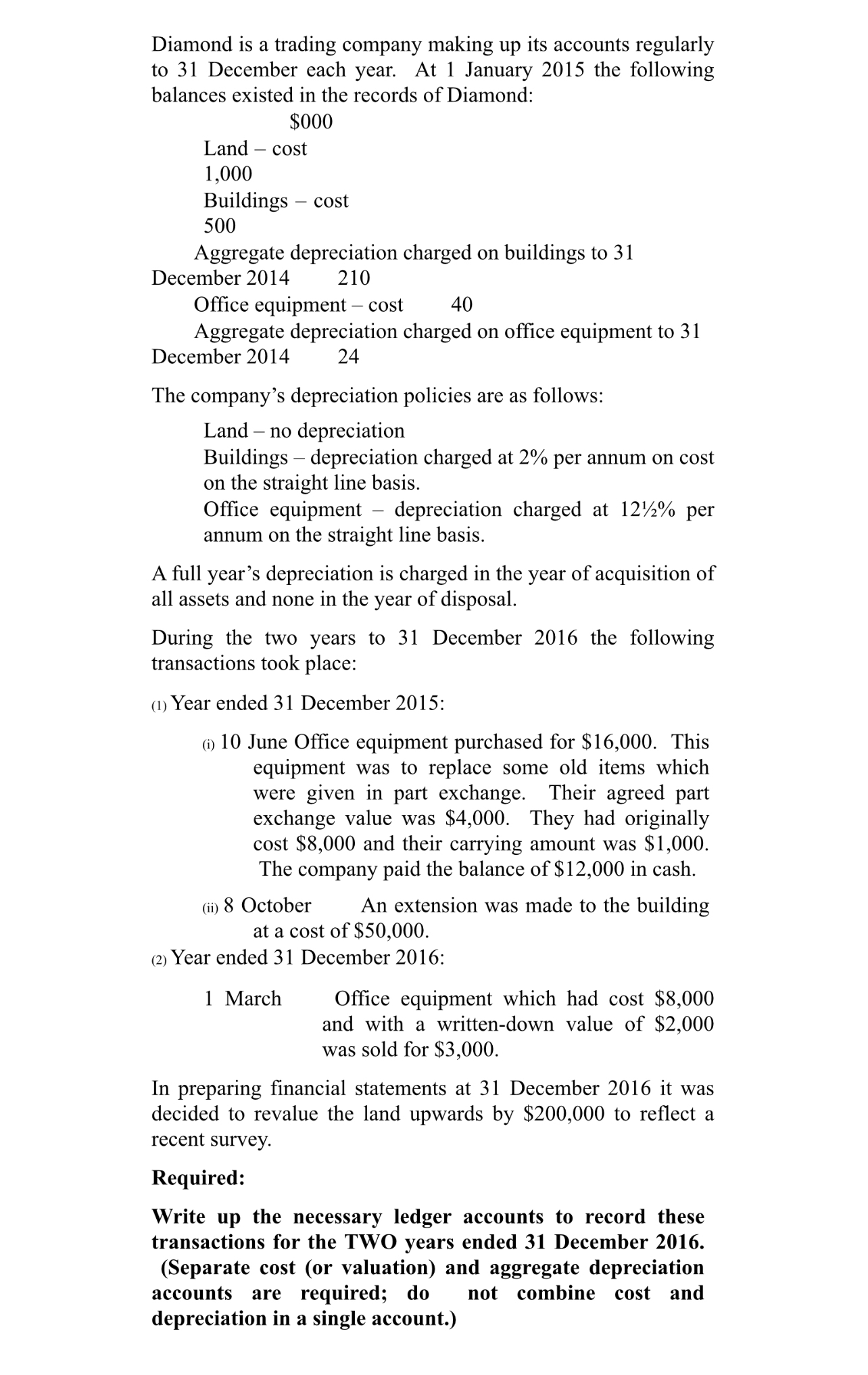

Diamond is a trading company making up its accounts regularly to 3 1 December each year. At 1 January 2 0 1 5 the following

Diamond is a trading company making up its accounts regularly

to December each year. At January the following

balances existed in the records of Diamond:

$

Land cost

Buildings cost

Aggregate depreciation charged on buildings to

December

Office equipment cost

Aggregate depreciation charged on office equipment to

December

The company's depreciation policies are as follows:

Land no depreciation

Buildings depreciation charged at per annum on cost

on the straight line basis.

Office equipment depreciation charged at per

annum on the straight line basis.

A full year's depreciation is charged in the year of acquisition of

all assets and none in the year of disposal.

During the two years to December the following

transactions took place:

Year ended December :

i June Office equipment purchased for $ This

equipment was to replace some old items which

were given in part exchange. Their agreed part

exchange value was $ They had originally

cost $ and their carrying amount was $

The company paid the balance of $ in cash.

ii October An extension was made to the building

at a cost of $

Year ended December :

March Office equipment which had cost $

and with a writtendown value of $

was sold for $

In preparing financial statements at December it was

decided to revalue the land upwards by $ to reflect a

recent survey.

Required:

Write up the necessary ledger accounts to record these

transactions for the TWO years ended December

Separate cost or valuation and aggregate depreciation

accounts are required; do not combine cost and

depreciation in a single account.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Intermediate Accounting

Authors: Loren A Nikolai, D. Bazley and Jefferson P. Jones

10th Edition

324300980, 978-0324300987