Answered step by step

Verified Expert Solution

Question

1 Approved Answer

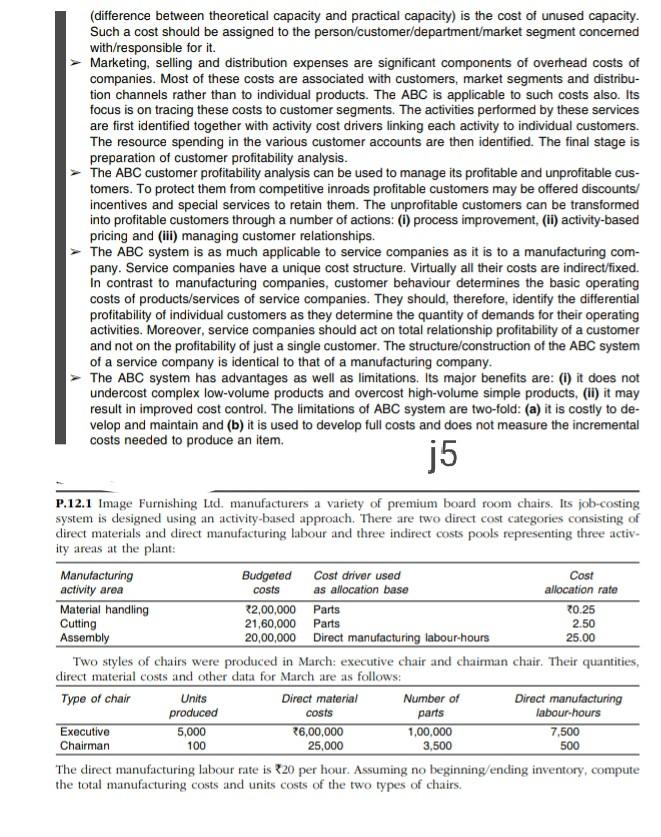

(difference between theoretical capacity and practical capacity) is the cost of unused capacity. Such a cost should be assigned to the person/customer/department/market segment concerned with/responsible

(difference between theoretical capacity and practical capacity) is the cost of unused capacity. Such a cost should be assigned to the person/customer/department/market segment concerned with/responsible for it. Marketing, selling and distribution expenses are significant components of overhead costs of companies. Most of these costs are associated with customers, market segments and distribu- tion channels rather than to individual products. The ABC is applicable to such costs also. Its focus is on tracing these costs to customer segments. The activities performed by these services are first identified together with activity cost drivers linking each activity to individual customers. The resource spending in the various customer accounts are then identified. The final stage is preparation of customer profitability analysis. The ABC customer profitability analysis can be used to manage its profitable and unprofitable cus- tomers. To protect them from competitive inroads profitable customers may be offered discounts/ incentives and special services to retain them. The unprofitable customers can be transformed into profitable customers through a number of actions: (1) process improvement, (ii) activity-based pricing and (iii) managing customer relationships. The ABC system is as much applicable to service companies as it is to a manufacturing com- pany. Service companies have a unique cost structure. Virtually all their costs are indirect/fixed. in contrast to manufacturing companies, customer behaviour determines the basic operating costs of products/services of service companies. They should, therefore, identify the differential profitability of individual customers as they determine the quantity of demands for their operating activities. Moreover, service companies should act on total relationship profitability of a customer and not on the profitability of just a single customer. The structure/construction of the ABC system of a service company is identical to that of a manufacturing company. The ABC system has advantages as well as limitations. Its major benefits are: (1) it does not undercost complex low-volume products and overcost high-volume simple products, (ii) it may result in improved cost control. The limitations of ABC system are two-fold: (a) it is costly to de velop and maintain and (b) it is used to develop full costs and does not measure the incremental costs needed to produce an item. j5 P.12.1 Image Furnishing Ltd. manufacturers a variety of premium board room chairs. Its job-costing system is designed using an activity-based approach. There are two direct cost categories consisting of direct materials and direct manufacturing labour and three indirect costs pools representing three activ- ity areas at the plant: Manufacturing Budgeted Cost driver used Cost activity area costs as allocation base allocation rate Material handling 22,00,000 Parts 20.25 Cutting 21,60,000 Parts 2.50 Assembly 20,00,000 Direct manufacturing labour-hours 25.00 Two styles of chairs were produced in March: executive chair and chairman chair. Their quantities, direct material costs and other data for March are as follows: Type of chair Units Direct material Number of Direct manufacturing produced costs parts labour-hours Executive 5,000 26,00,000 1,00,000 7,500 Chairman 25,000 3,500 The direct manufacturing labour rate is 20 per hour. Assuming no beginning/ending inventory, compute the total manufacturing costs and units costs of the two types of chairs. 100 500

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Internal Auditing An Integrated Approach

Authors: Richard Cascarino

3rd Edition

1485110599, 978-1485110590