Discuss RadNets pre-merger capital structure based on the trade-off theory of capital structure.

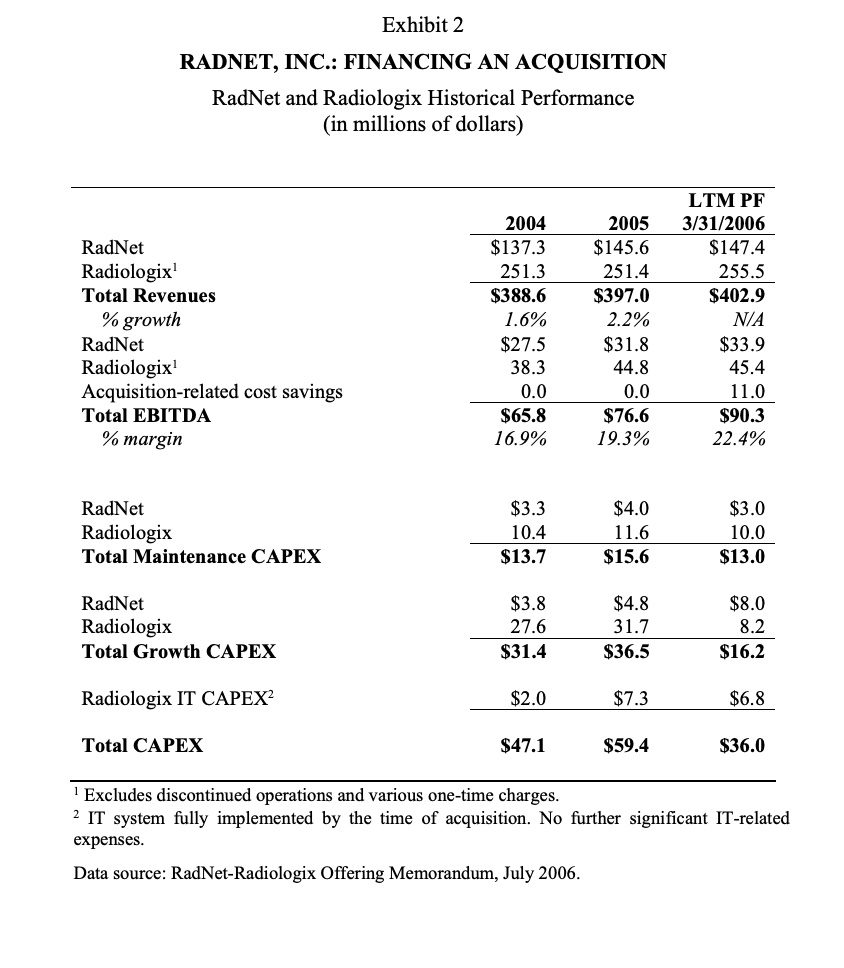

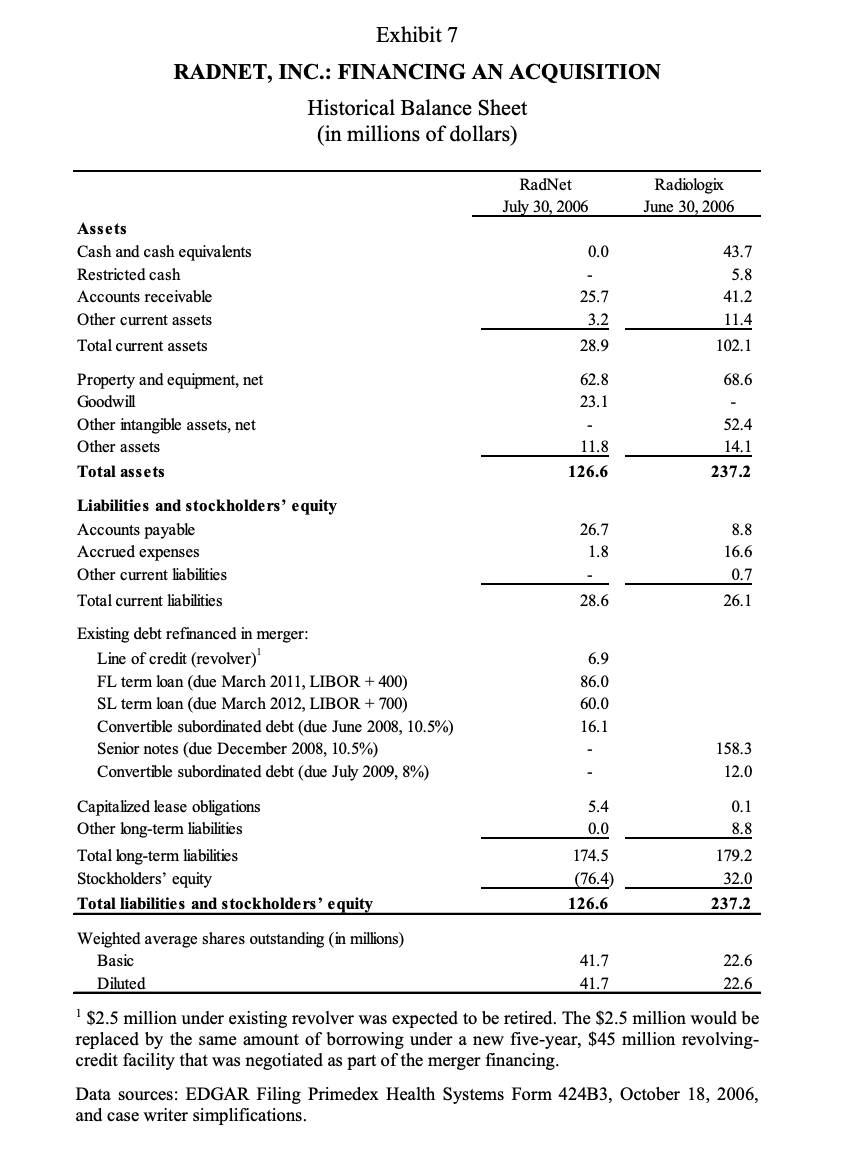

Exhibit 2 RADNET, INC.: FINANCING AN ACQUISITION RadNet and Radiologix Historical Performance (in millions of dollars) RadNet Radiologix Total Revenues % growth RadNet Radiologix Acquisition-related cost savings Total EBITDA % margin 2004 $137.3 251.3 $388.6 1.6% $27.5 38.3 0.0 $65.8 16.9% 2005 $145.6 251.4 $397.0 2.2% $31.8 44.8 0.0 $76.6 19.3% LTM PF 3/31/2006 $147.4 255.5 $402.9 N/A $33.9 45.4 11.0 $90.3 22.4% RadNet Radiologix Total Maintenance CAPEX $3.3 10.4 $13.7 $4.0 11.6 $15.6 $3.0 10.0 $13.0 RadNet Radiologix Total Growth CAPEX $3.8 27.6 $31.4 $4.8 31.7 $36.5 $8.0 8.2 $16.2 Radiologix IT CAPEX $2.0 $7.3 $6.8 Total CAPEX $47.1 $59.4 $36.0 Excludes discontinued operations and various one-time charges. 2 IT system fully implemented by the time of acquisition. No further significant IT-related expenses. Data sour RadNet-Radiologix Offering Memorandum, July 2006. Exhibit 7 RADNET, INC.: FINANCING AN ACQUISITION Historical Balance Sheet (in millions of dollars) RadNet July 30, 2006 Radiologix June 30, 2006 0.0 Assets Cash and cash equivalents Restricted cash Accounts receivable Other current assets Total current assets 43.7 5.8 41.2 25.7 3.2 11.4 28.9 102.1 68.6 62.8 23.1 Property and equipment, net Goodwill Other intangible assets, net Other assets Total assets 52.4 14.1 11.8 126.6 237.2 Liabilities and stockholders' equity Accounts payable Accrued expenses Other current liabilities Total current liabilities 26.7 1.8 8.8 16.6 0.7 28.6 26.1 Existing debt refinanced in merger: Line of credit (revolver) FL term loan (due March 2011, LIBOR +400) SL term loan (due March 2012, LIBOR + 700) Convertible subordinated debt (due June 2008, 10.5%) Senior notes (due December 2008, 10.5%) Convertible subordinated debt (due July 2009, 8%) 6.9 86.0 60.0 16.1 158.3 12.0 Capitalized lease obligations Other long-term liabilities Total long-term liabilities Stockholders' equity Total liabilities and stockholders' equity 5.4 0.0 174.5 (76.4) 126.6 0.1 8.8 179.2 32.0 237.2 Weighted average shares outstanding in millions) Basic Diluted 41.7 41.7 22.6 22.6 $2.5 million under existing revolver was expected to be retired. The $2.5 million would be replaced by the same amount of borrowing under a new five-year, $45 million revolving- credit facility that was negotiated as part of the merger financing. Data sources: EDGAR Filing Primedex Health Systems Form 424B3, October 18, 2006, and case writer simplifications. Exhibit 2 RADNET, INC.: FINANCING AN ACQUISITION RadNet and Radiologix Historical Performance (in millions of dollars) RadNet Radiologix Total Revenues % growth RadNet Radiologix Acquisition-related cost savings Total EBITDA % margin 2004 $137.3 251.3 $388.6 1.6% $27.5 38.3 0.0 $65.8 16.9% 2005 $145.6 251.4 $397.0 2.2% $31.8 44.8 0.0 $76.6 19.3% LTM PF 3/31/2006 $147.4 255.5 $402.9 N/A $33.9 45.4 11.0 $90.3 22.4% RadNet Radiologix Total Maintenance CAPEX $3.3 10.4 $13.7 $4.0 11.6 $15.6 $3.0 10.0 $13.0 RadNet Radiologix Total Growth CAPEX $3.8 27.6 $31.4 $4.8 31.7 $36.5 $8.0 8.2 $16.2 Radiologix IT CAPEX $2.0 $7.3 $6.8 Total CAPEX $47.1 $59.4 $36.0 Excludes discontinued operations and various one-time charges. 2 IT system fully implemented by the time of acquisition. No further significant IT-related expenses. Data sour RadNet-Radiologix Offering Memorandum, July 2006. Exhibit 7 RADNET, INC.: FINANCING AN ACQUISITION Historical Balance Sheet (in millions of dollars) RadNet July 30, 2006 Radiologix June 30, 2006 0.0 Assets Cash and cash equivalents Restricted cash Accounts receivable Other current assets Total current assets 43.7 5.8 41.2 25.7 3.2 11.4 28.9 102.1 68.6 62.8 23.1 Property and equipment, net Goodwill Other intangible assets, net Other assets Total assets 52.4 14.1 11.8 126.6 237.2 Liabilities and stockholders' equity Accounts payable Accrued expenses Other current liabilities Total current liabilities 26.7 1.8 8.8 16.6 0.7 28.6 26.1 Existing debt refinanced in merger: Line of credit (revolver) FL term loan (due March 2011, LIBOR +400) SL term loan (due March 2012, LIBOR + 700) Convertible subordinated debt (due June 2008, 10.5%) Senior notes (due December 2008, 10.5%) Convertible subordinated debt (due July 2009, 8%) 6.9 86.0 60.0 16.1 158.3 12.0 Capitalized lease obligations Other long-term liabilities Total long-term liabilities Stockholders' equity Total liabilities and stockholders' equity 5.4 0.0 174.5 (76.4) 126.6 0.1 8.8 179.2 32.0 237.2 Weighted average shares outstanding in millions) Basic Diluted 41.7 41.7 22.6 22.6 $2.5 million under existing revolver was expected to be retired. The $2.5 million would be replaced by the same amount of borrowing under a new five-year, $45 million revolving- credit facility that was negotiated as part of the merger financing. Data sources: EDGAR Filing Primedex Health Systems Form 424B3, October 18, 2006, and case writer simplifications