Answered step by step

Verified Expert Solution

Question

1 Approved Answer

discuss risk profile, asset allocation and application to recommend strategy to this couple. Case Study Information: The Williams Family Sophie and Wendall Williams have come

discuss risk profile, asset allocation and application to recommend strategy to this couple.

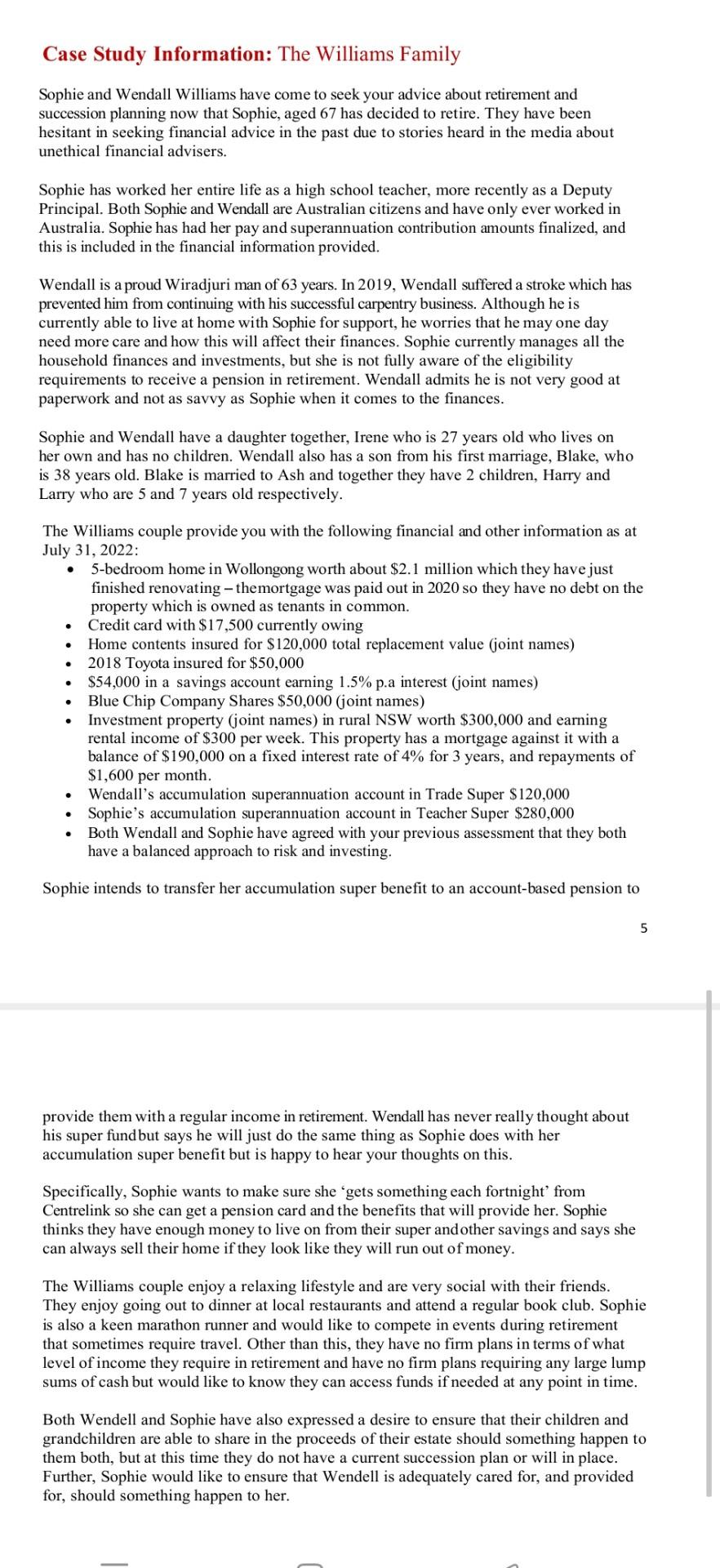

Case Study Information: The Williams Family Sophie and Wendall Williams have come to seek your advice about retirement and succession planning now that Sophie, aged 67 has decided to retire. They have been hesitant in seeking financial advice in the past due to stories heard in the media about unethical financial advisers. Sophie has worked her entire life as a high school teacher, more recently as a Deputy Principal. Both Sophie and Wendall are Australian citizens and have only ever worked in Australia. Sophie has had her pay and superannuation contribution amounts finalized, and this is included in the financial information provided. Wendall is a proud Wiradjuri man of 63 years. In 2019 , Wendall suffered a stroke which has prevented him from continuing with his successful carpentry business. Although he is currently able to live at home with Sophie for support, he worries that he may one day need more care and how this will affect their finances. Sophie currently manages all the household finances and investments, but she is not fully aware of the eligibility requirements to receive a pension in retirement. Wendall admits he is not very good at paperwork and not as savvy as Sophie when it comes to the finances. Sophie and Wendall have a daughter together, Irene who is 27 years old who lives on her own and has no children. Wendall also has a son from his first marriage, Blake, who is 38 years old. Blake is married to Ash and together they have 2 children, Harry and Larry who are 5 and 7 years old respectively. The Williams couple provide you with the following financial and other information as at July 31, 2022: - 5-bedroom home in Wollongong worth about $2.1 million which they have just finished renovating - themortgage was paid out in 2020 so they have no debt on the property which is owned as tenants in common. - Credit card with $17,500 currently owing - Home contents insured for $120,000 total replacement value (joint names) - 2018 Toyota insured for $50,000 - $54,000 in a savings account earning 1.5% p.a interest (joint names) - Blue Chip Company Shares $50,000 (joint names) - Investment property (joint names) in rural NSW worth $300,000 and earning rental income of $300 per week. This property has a mortgage against it with a balance of $190,000 on a fixed interest rate of 4% for 3 years, and repayments of $1,600 per month. - Wendall's accumulation superannuation account in Trade Super $120,000 - Sophie's accumulation superannuation account in Teacher Super $280,000 - Both Wendall and Sophie have agreed with your previous assessment that they both have a balanced approach to risk and investing. Sophie intends to transfer her accumulation super benefit to an account-based pension to 5 provide them with a regular income in retirement. Wendall has never really thought about his super fund but says he will just do the same thing as Sophie does with her accumulation super benefit but is happy to hear your thoughts on this. Specifically, Sophie wants to make sure she 'gets something each fortnight' from Centrelink so she can get a pension card and the benefits that will provide her. Sophie thinks they have enough money to live on from their super and other savings and says she can always sell their home if they look like they will run out of money. The Williams couple enjoy a relaxing lifestyle and are very social with their friends. They enjoy going out to dinner at local restaurants and attend a regular book club. Sophie is also a keen marathon runner and would like to compete in events during retirement that sometimes require travel. Other than this, they have no firm plans in terms of what level of income they require in retirement and have no firm plans requiring any large lump sums of cash but would like to know they can access funds if needed at any point in time. Both Wendell and Sophie have also expressed a desire to ensure that their children and grandchildren are able to share in the proceeds of their estate should something happen to them both, but at this time they do not have a current succession plan or will in place. Further, Sophie would like to ensure that Wendell is adequately cared for, and provided for, should something happen to her. Case Study Information: The Williams Family Sophie and Wendall Williams have come to seek your advice about retirement and succession planning now that Sophie, aged 67 has decided to retire. They have been hesitant in seeking financial advice in the past due to stories heard in the media about unethical financial advisers. Sophie has worked her entire life as a high school teacher, more recently as a Deputy Principal. Both Sophie and Wendall are Australian citizens and have only ever worked in Australia. Sophie has had her pay and superannuation contribution amounts finalized, and this is included in the financial information provided. Wendall is a proud Wiradjuri man of 63 years. In 2019 , Wendall suffered a stroke which has prevented him from continuing with his successful carpentry business. Although he is currently able to live at home with Sophie for support, he worries that he may one day need more care and how this will affect their finances. Sophie currently manages all the household finances and investments, but she is not fully aware of the eligibility requirements to receive a pension in retirement. Wendall admits he is not very good at paperwork and not as savvy as Sophie when it comes to the finances. Sophie and Wendall have a daughter together, Irene who is 27 years old who lives on her own and has no children. Wendall also has a son from his first marriage, Blake, who is 38 years old. Blake is married to Ash and together they have 2 children, Harry and Larry who are 5 and 7 years old respectively. The Williams couple provide you with the following financial and other information as at July 31, 2022: - 5-bedroom home in Wollongong worth about $2.1 million which they have just finished renovating - themortgage was paid out in 2020 so they have no debt on the property which is owned as tenants in common. - Credit card with $17,500 currently owing - Home contents insured for $120,000 total replacement value (joint names) - 2018 Toyota insured for $50,000 - $54,000 in a savings account earning 1.5% p.a interest (joint names) - Blue Chip Company Shares $50,000 (joint names) - Investment property (joint names) in rural NSW worth $300,000 and earning rental income of $300 per week. This property has a mortgage against it with a balance of $190,000 on a fixed interest rate of 4% for 3 years, and repayments of $1,600 per month. - Wendall's accumulation superannuation account in Trade Super $120,000 - Sophie's accumulation superannuation account in Teacher Super $280,000 - Both Wendall and Sophie have agreed with your previous assessment that they both have a balanced approach to risk and investing. Sophie intends to transfer her accumulation super benefit to an account-based pension to 5 provide them with a regular income in retirement. Wendall has never really thought about his super fund but says he will just do the same thing as Sophie does with her accumulation super benefit but is happy to hear your thoughts on this. Specifically, Sophie wants to make sure she 'gets something each fortnight' from Centrelink so she can get a pension card and the benefits that will provide her. Sophie thinks they have enough money to live on from their super and other savings and says she can always sell their home if they look like they will run out of money. The Williams couple enjoy a relaxing lifestyle and are very social with their friends. They enjoy going out to dinner at local restaurants and attend a regular book club. Sophie is also a keen marathon runner and would like to compete in events during retirement that sometimes require travel. Other than this, they have no firm plans in terms of what level of income they require in retirement and have no firm plans requiring any large lump sums of cash but would like to know they can access funds if needed at any point in time. Both Wendell and Sophie have also expressed a desire to ensure that their children and grandchildren are able to share in the proceeds of their estate should something happen to them both, but at this time they do not have a current succession plan or will in place. Further, Sophie would like to ensure that Wendell is adequately cared for, and provided for, should something happen to herStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Structured Credit Handbook

Authors: Arvind Rajan, Glen McDermott, Ratul Roy

1st Edition

0471747491, 978-0471747499