Answered step by step

Verified Expert Solution

Question

1 Approved Answer

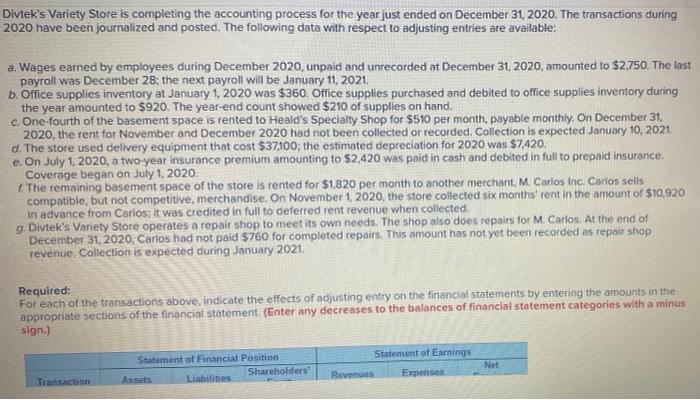

Divtek's Variety Store is completing the accounting process for the year just ended on December 31, 2020. The transactions during 2020 have been journalized

Divtek's Variety Store is completing the accounting process for the year just ended on December 31, 2020. The transactions during 2020 have been journalized and posted. The following data with respect to adjusting entries are available: a. Wages earned by employees during December 2020, unpaid and unrecorded at December 31, 2020, amounted to $2.750. The last payroll was December 28; the next payroll will be January 11, 2021. b. Office supplies inventory at January 1, 2020 was $360. Office supplies purchased and debited to office supplies inventory during the year amounted to $920. The year-end count showed $210 of supplies on hand. c. One-fourth of the basement space is rented to Heald's Specialty Shop for $510 per month, payable monthly. On December 31, 2020, the rent for November and December 2020 had not been collected or recorded. Collection is expected January 10, 2021. d. The store used delivery equipment that cost $37,100; the estimated depreciation for 2020 was $7,420. e. On July 1, 2020, a two-year insurance premium amounting to $2,420 was paid in cash and debited in full to prepaid insurance. Coverage began on July 1, 2020. f. The remaining basement space of the store is rented for $1,820 per month to another merchant, M. Carlos Inc. Carlos sells compatible, but not competitive, merchandise. On November 1, 2020, the store collected six months' rent in the amount of $10,920 in advance from Carlos; it was credited in full to deferred rent revenue when collected. g. Divtek's Variety Store operates a repair shop to meet its own needs. The shop also does repairs for M. Carlos. At the end of December 31, 2020, Carlos had not paid $760 for completed repairs. This amount has not yet been recorded as repair shop revenue. Collection is expected during January 2021. Required: For each of the transactions above, indicate the effects of adjusting entry on the financial statements by entering the amounts in the appropriate sections of the financial statement. (Enter any decreases to the balances of financial statement categories with a minus sign.) Statement of Financial Position Transaction Assets Liabilities Shareholders Revenues Statement of Earnings Expenses Net

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Essentials of Accounting for Governmental and Not-for-Profit Organizations

Authors: Paul Copley

12th edition

0078025818, 978-0078025815