DO 8.2 part ii) AND 8.3.

DO 8.2 part ii) AND 8.3.

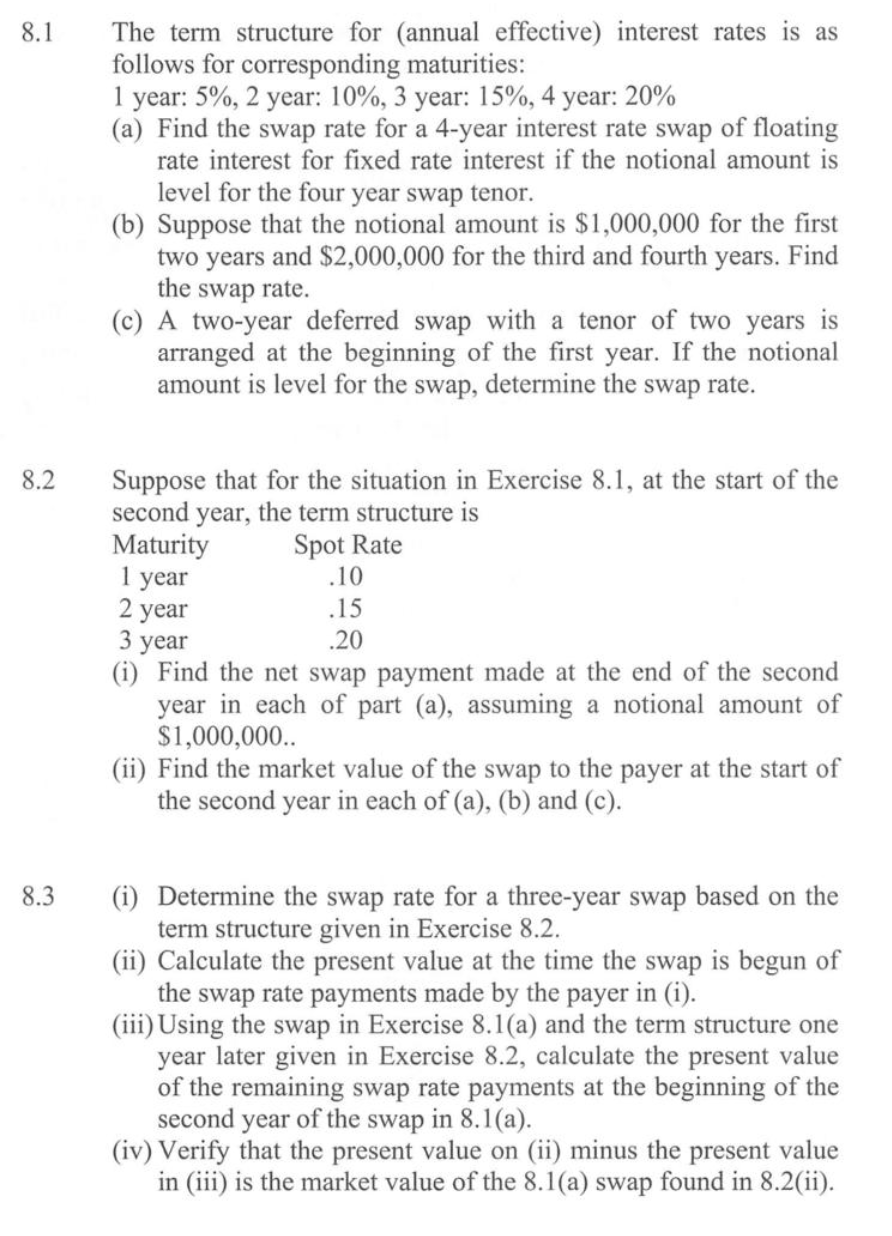

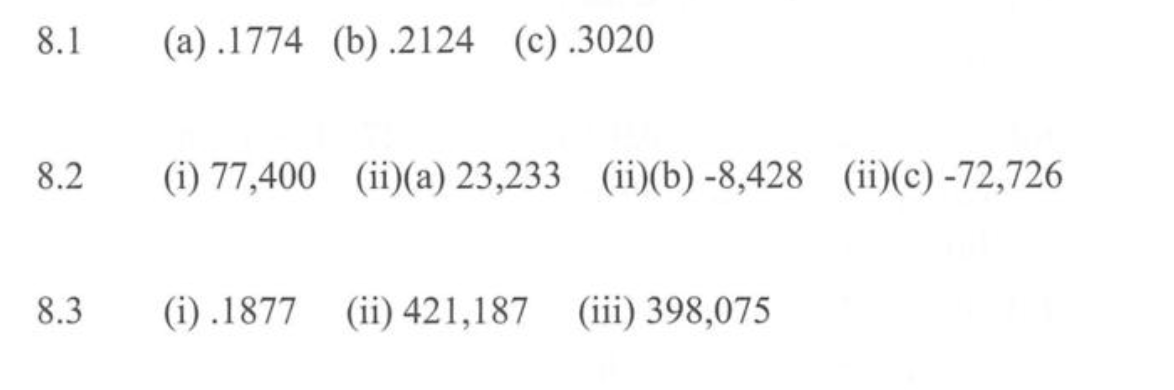

8.1 The term structure for (annual effective) interest rates is as follows for corresponding maturities: 1 year: 5%, 2 year: 10%, 3 year: 15%, 4 year: 20% (a) Find the swap rate for a 4-year interest rate swap of floating rate interest for fixed rate interest if the notional amount is level for the four year swap tenor. (b) Suppose that the notional amount is $1,000,000 for the first two years and $2,000,000 for the third and fourth years. Find the swap rate. (c) A two-year deferred swap with a tenor of two years is arranged at the beginning of the first year. If the notional amount is level for the swap, determine the swap rate. 8.2 Suppose that for the situation in Exercise 8.1, at the start of the second year, the term structure is Maturity Spot Rate 1 year .10 2 year .15 3 year .20 (i) Find the net swap payment made at the end of the second year in each of part (a), assuming a notional amount of $1,000,000.. (ii) Find the market value of the swap to the payer at the start of the second year in each of (a), (b) and (c). 8.3 (i) Determine the swap rate for a three-year swap based on the term structure given in Exercise 8.2. (ii) Calculate the present value at the time the swap is begun of the swap rate payments made by the payer in (i). (iii) Using the swap in Exercise 8.1(a) and the term structure one year later given in Exercise 8.2, calculate the present value of the remaining swap rate payments at the beginning of the second year of the swap in 8.1(a). (iv) Verify that the present value on (ii) minus the present value in (iii) is the market value of the 8.1(a) swap found in 8.2(ii). 8.1 (a) .1774 (b) .2124 (c).3020 8.2 (i) 77,400 (ii)(a) 23,233 (ii)(b) -8,428 (ii)(C) -72,726 8.3 (i).1877 (ii) 421,187 (iii) 398,075 8.1 The term structure for (annual effective) interest rates is as follows for corresponding maturities: 1 year: 5%, 2 year: 10%, 3 year: 15%, 4 year: 20% (a) Find the swap rate for a 4-year interest rate swap of floating rate interest for fixed rate interest if the notional amount is level for the four year swap tenor. (b) Suppose that the notional amount is $1,000,000 for the first two years and $2,000,000 for the third and fourth years. Find the swap rate. (c) A two-year deferred swap with a tenor of two years is arranged at the beginning of the first year. If the notional amount is level for the swap, determine the swap rate. 8.2 Suppose that for the situation in Exercise 8.1, at the start of the second year, the term structure is Maturity Spot Rate 1 year .10 2 year .15 3 year .20 (i) Find the net swap payment made at the end of the second year in each of part (a), assuming a notional amount of $1,000,000.. (ii) Find the market value of the swap to the payer at the start of the second year in each of (a), (b) and (c). 8.3 (i) Determine the swap rate for a three-year swap based on the term structure given in Exercise 8.2. (ii) Calculate the present value at the time the swap is begun of the swap rate payments made by the payer in (i). (iii) Using the swap in Exercise 8.1(a) and the term structure one year later given in Exercise 8.2, calculate the present value of the remaining swap rate payments at the beginning of the second year of the swap in 8.1(a). (iv) Verify that the present value on (ii) minus the present value in (iii) is the market value of the 8.1(a) swap found in 8.2(ii). 8.1 (a) .1774 (b) .2124 (c).3020 8.2 (i) 77,400 (ii)(a) 23,233 (ii)(b) -8,428 (ii)(C) -72,726 8.3 (i).1877 (ii) 421,187 (iii) 398,075