Question

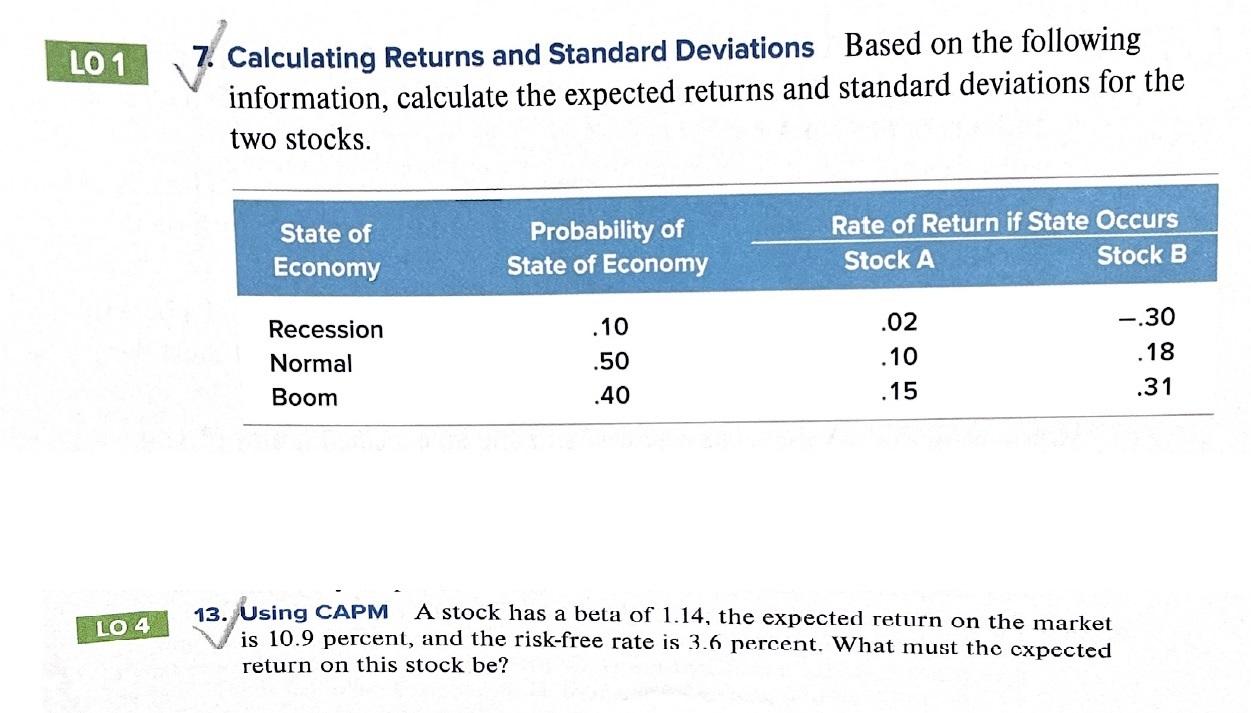

Do Problem 7 and Problem 13 on page 383 with the following modifications for problem 7. 1. Assume probability of state of economy to be

Do Problem 7 and Problem 13 on page 383 with the following modifications for problem 7.

1. Assume probability of state of economy to be equal, that is 1/3 for each state of economy.

2. Construct an equally weighted portfolio of Stock A and Stock B (50% of Stock A and 50% of Stock B). Determine the expected return and standard deviation of such a portfolio.

3. Compare the standard deviation of this portfolio to the average standard deviation of Stock A and Stock B. Which is lower? Explain.

4. Assume return on Stock A has a correlation coefficient of 0.70 with the market portfolio, S&P500, and return on Stock B has a correlation coefficient of 0.45 with the market portfolio, S&P500, and that the return of S&P 500 has a standard deviation of 25%. Determine the beta of Stock A and the beta of Stock B.

Would it be possible to show excel formulas for each question in an excel worksheet? Thank you!

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Bitcoin 101 A Beginner S Guide To Digital Currency

Authors: Nicholas Mohr

1st Edition

B0BW27PC43