Donotuse any outside research whatsoever. All research is contained within the case PDF. Please provide your own, original analysis. Read the case study PDF: Chase

Donotuse any outside research whatsoever.

All research is contained within the case PDF. Please provide your own, original analysis.

Read the case study PDF: Chase Sapphire- Creating a Millennial Cult Brand

Please answer the following (in a Case Study / written paper format using full sentences and prose (NOT bullet points)):

In completing the case please make sure to answer the following in your paper.

Note: Remember to reference the case's attached exhibits and financials were relevant.

Do NOT use first person ("I" or "me" forms of speech) in writing a case document

Perform a brand analysis of Chase using the case documents and the brand pyramid. Your analysis should mirror your work from the discussion board assignment as follows:

SALIENCE (Category)

Needs this category fulfills for target segments

Recognition - how is Chase recognized and regarded within its category by target segments?

PERFORMANCE & JUDGEMENTS

Features & Functional - what features do target segments like about Chase and its product(s)?

Design (elements that we know matter)

Describe Chase's design and how your brand's design differentiates and what it communicates

Fighting brand confusion: What we need them to know/believe (incl. brand "truths") that they aren't aware of or are confused regarding and describe how the brand can help communicate that fact better.

(From video: Think Keurig where some customers believe Keurig has instant coffee in their k-cups instead of high quality grounds. The company needs to change this perception. This can also be something the company does well but not enough customers are aware)

FEELINGS & IMAGERY

Emotional Connection - describe the emotional fulfillment target segments receive from Chase

Social Connections - what social value does Chase deliver to target segments? (Think Prius and how it allows customers to communicate they are "green" just by driving such a unique looking vehicle)

Remember social media matters here

Image - How would you describe Chase's image?

Are there gaps?

Should they be doing anything differently?

2) Your paper begins here

Overview

What was the general market for credit card offerings and where was Chase looking to compete?

How did the Sapphire concept sit with Chase's existing product offerings and why was Sapphire an offering the market needed?

Customers

Describe the landscape of segments for credit card customers and based on your answers where is Chase's best opportunity for the Sapphire?

Who are the most ideal customers for the Chase Sapphire card and what are their expectations of a credit card offering?

Please pay special attention to Dormants (people who use and shelve the card) and churners (people who rack up points and leave the service). If there are other segments please find them.

Challenges

What defines success for Chase in launching Sapphire (besides getting as many subscribers/cardholders as possible which is a given)?

What are churners and why do they present a challenge?

What challenges to dormants pose?

If you have uncovered other segments, what challenges do they pose to the success of this card?

What were the challenges in designing Sapphire to appeal to key segments?

How did Chase answer these challenges and fulfill customer expectations at the same time? (pay special attention to the Millennial and millennial-minded base)

Remember to refer back to your brand pyramid too

GTM (go-to-market) strategy

How did Chase market the Sapphire and why (or why not) do you believe it maximized effectiveness? Could they have done something better?

Remember to leverage learnings from your brand pyramid

Why or why not do you consider Chase Sapphire to be a success? Back your answers with information from the case.

Recommendations

Given competitor responses and the possible opportunities for Chase after successfully being in the market a while, make at least three strategic recommendations to senior management on what you think is the best path forward and back your answer with case information.

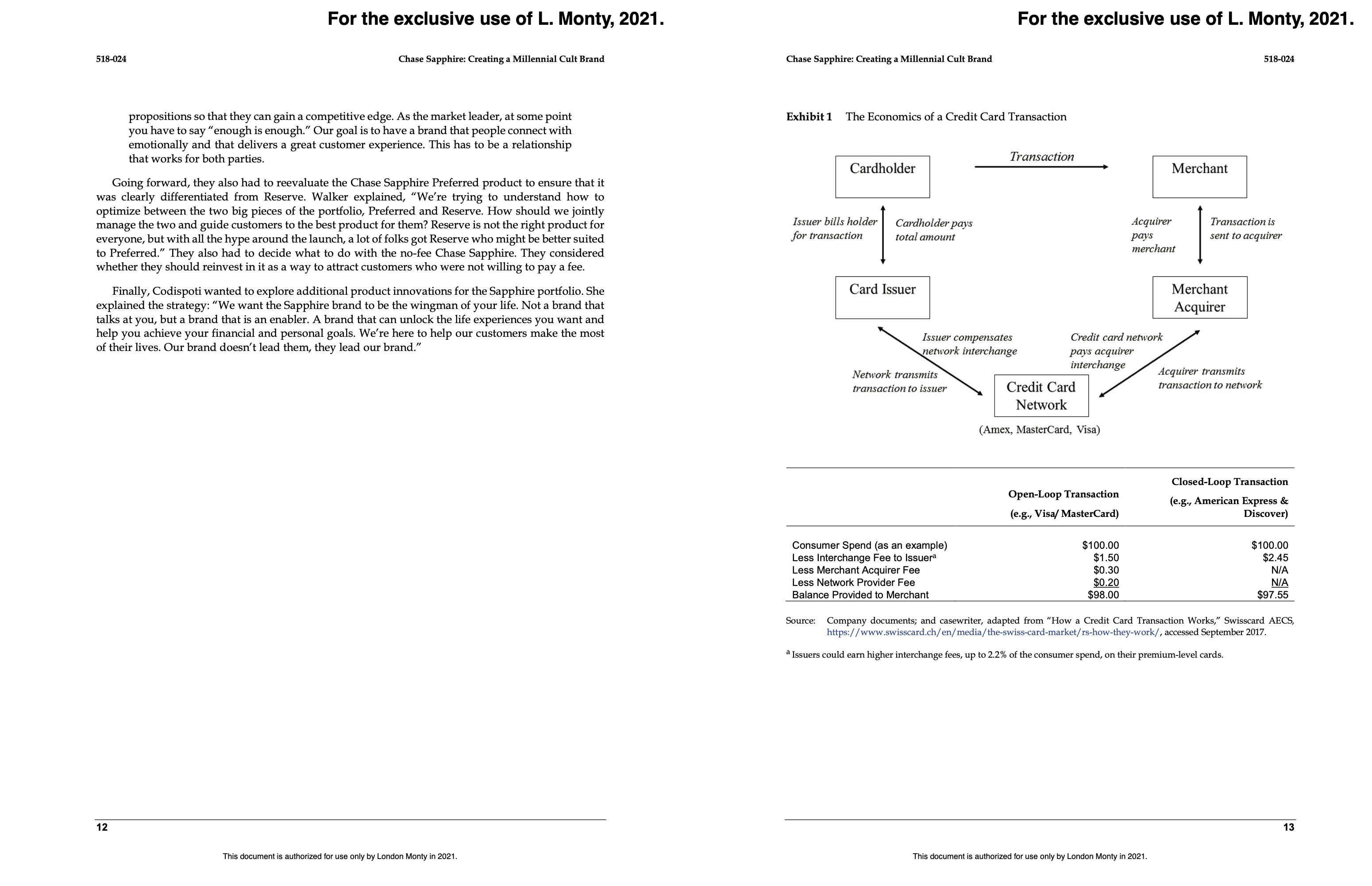

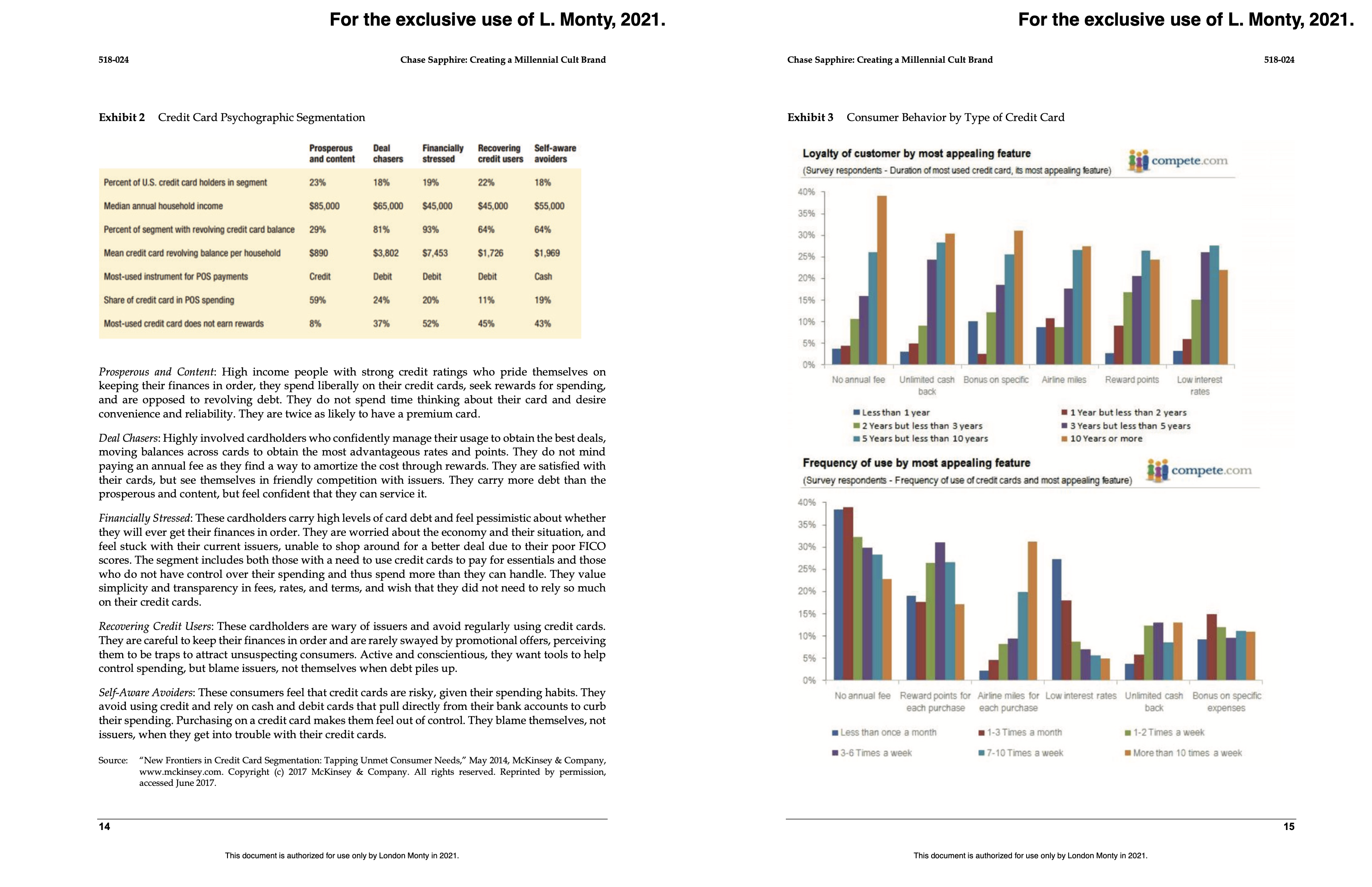

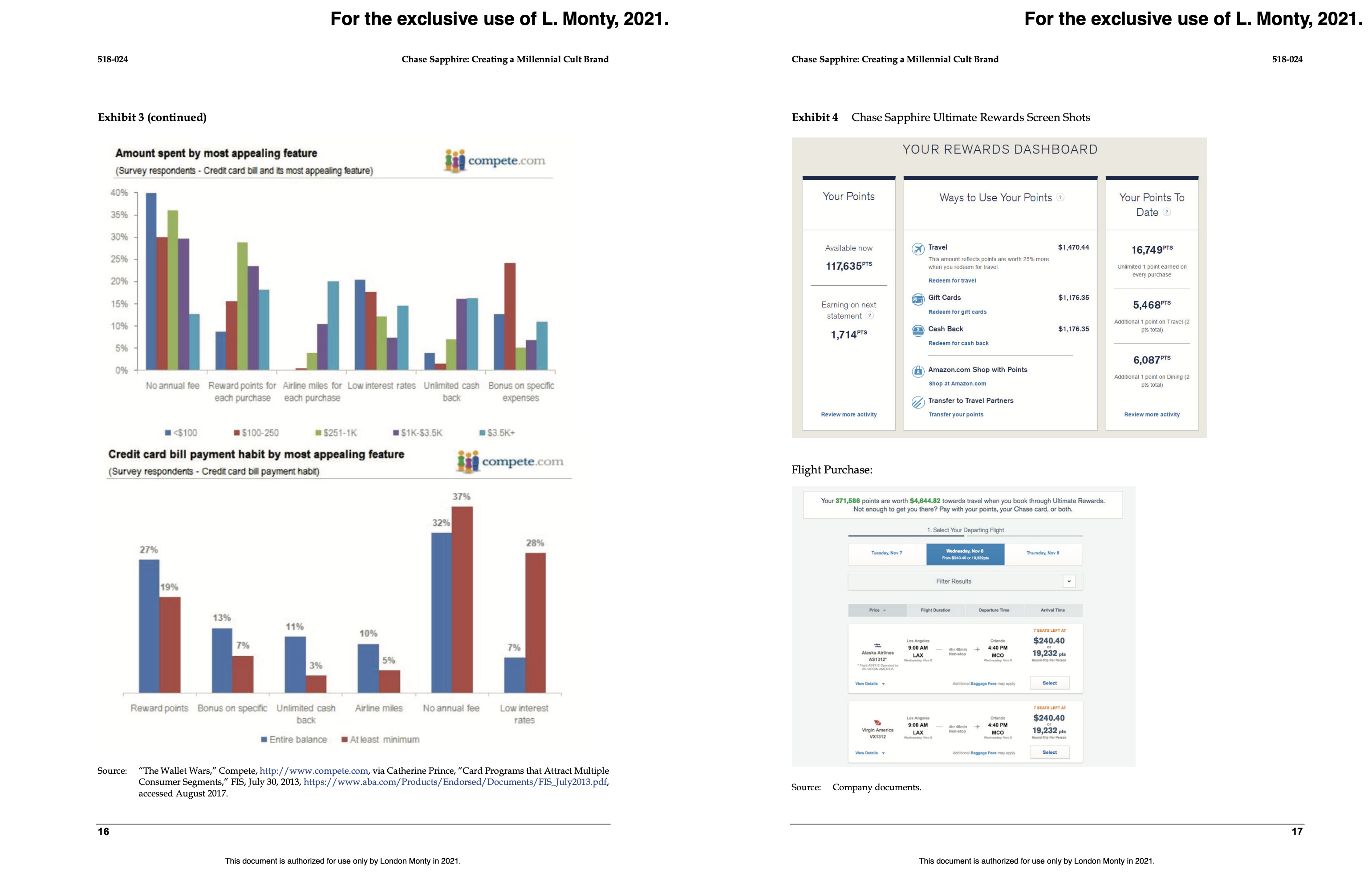

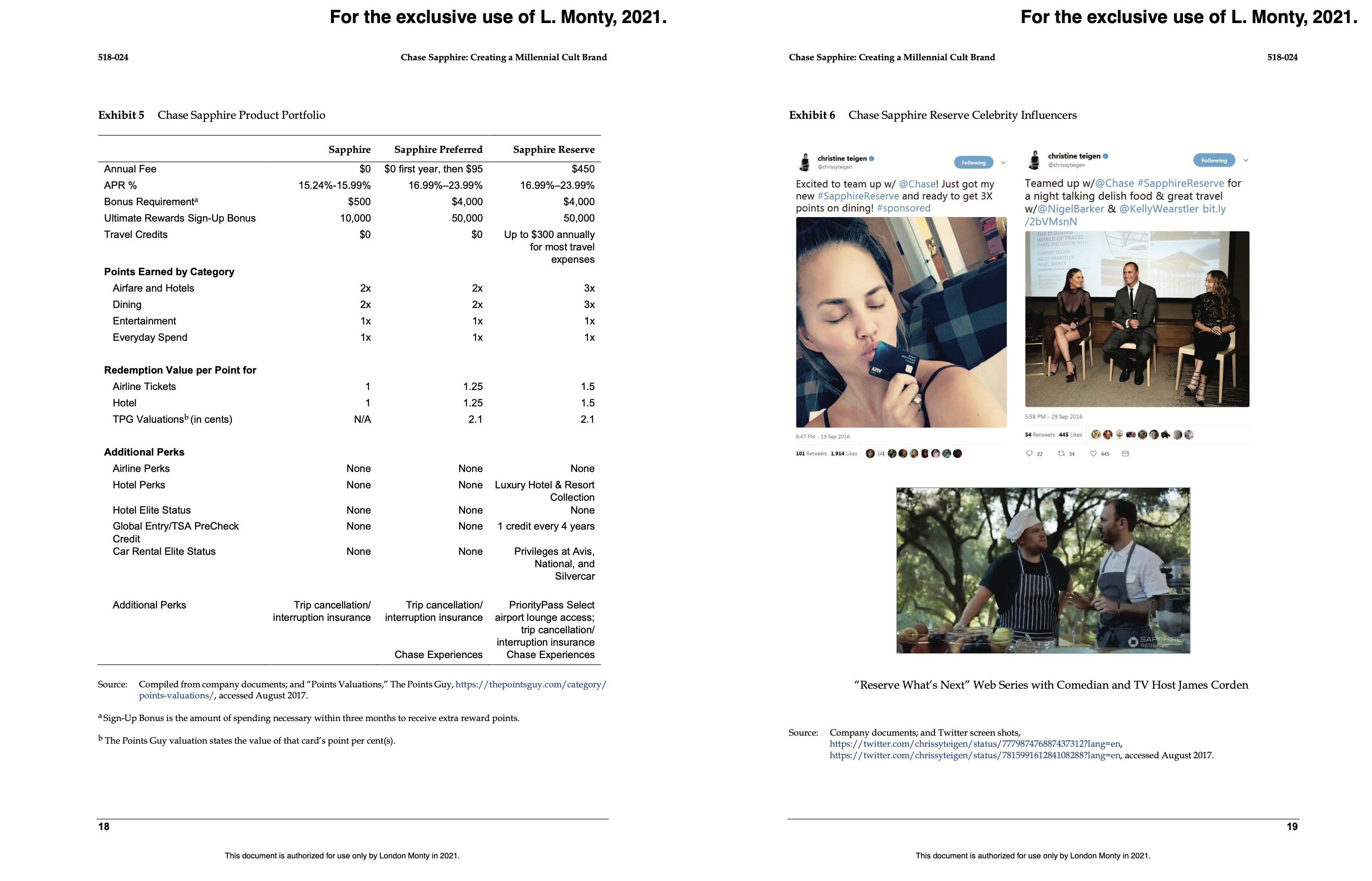

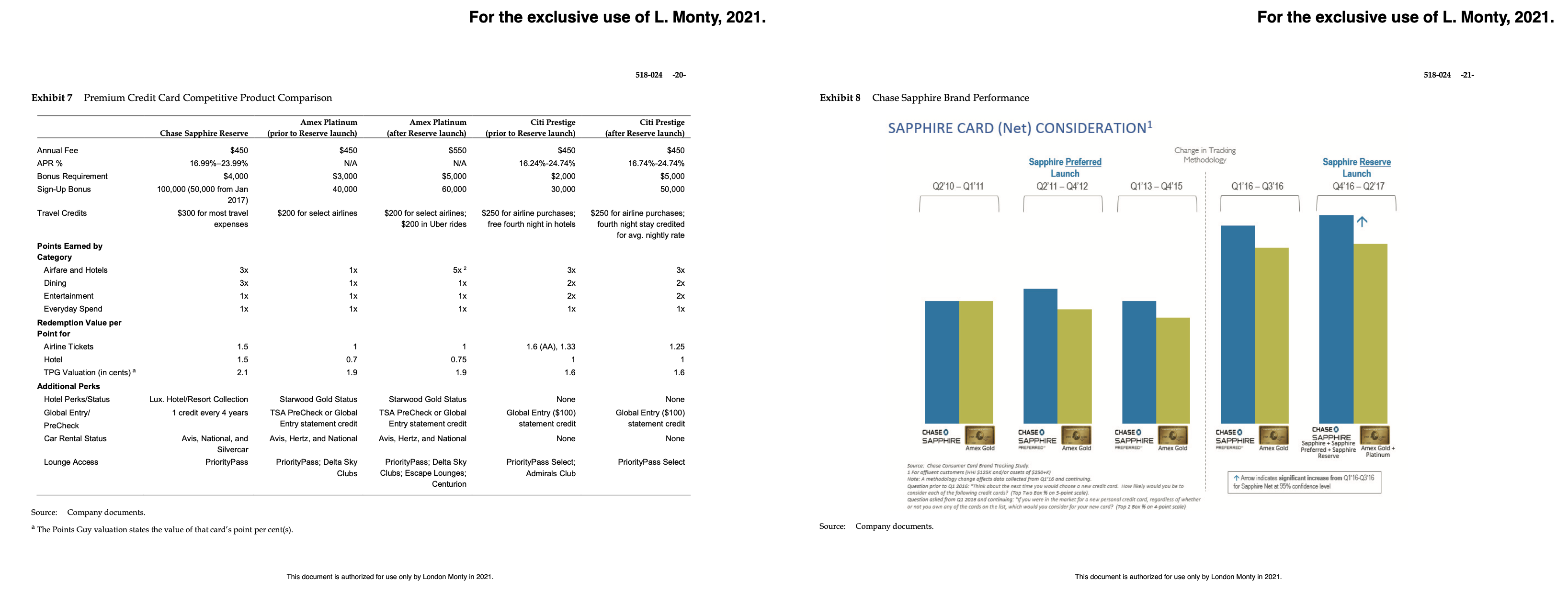

For the exclusive use of L. Monty, 2021. 5184024 Chase Sapphire: Creating a Millennial Cult Brand JPMorgan Chase: Consumer and Community Banking IPMorgan Chase (naerated four lines of business: Commercial Banking Corporate k Investment Bank, Asset 5r Wealth Management, and Consumer 5: Community Banking (CCB). Under the leadership of CEO Gordon Smith, the CCB division served as the face of the company to the general public. In addition to credit cards, CCB also included merchant acquiring, payment processing, small business and consumer banking services (including Chase's 5,200 retail bank branches), mortgages, and auto nancing. In 2016, CCB counted nearly half of all US. households as customers and generated $44.9 billion in revenue, with net income of $9.7 billion. Chase was ranked #1 or #2 in credit card issuance, credit and debit payments volume, and merchant acquisitions. It boasted the highest-rated mobile banking app and the largest ATM network (with 18,000 locations), and was the most visited banking portal. Over 50% of afuent US. households lived within two miles of a Chase branch or ATMI The US. Consumer Credit Card Market There were ve primary players in the credit card industry. Issuers were banks that issued credit cards to consumers and businesses, extended loans in the form of credit lines, and absorbed the resulting credit risk Cardholders repaid charges made on their cards, often in monthly installments, paying interest on the unpaid portion Merchant Acquirers signed up and managed relationships with Merchants so that merchants could accept credit cards as a form of payment. Network Providers (erg, MasterCard and Visa) processed payments between consumers and merchants Under the \"open-loop\" system operated by MasterCard and Visa, an issuer, such as JPMorgan Chase, marketed and issued cards to consumers and businesses, MasterCard or Visa processed the transactions, and a merchant acquirer enrolled merchants to accept issuers' cards running on the network provider's system.2 In contrast, American Express (Amex) and Discover served as their own network providers and merchant acquirers in a \"closed-loop\" system. Each of the partners received a small percentage of the value of each customer" s purchase (i.e., "transaction"). (See Exhibit 1 for a summary.) In 2016, the Us. general purpose credit card industry sales totaled ~$3 tr'illiorL3 In Q4 2016, the market was dominated by six issuers that accounted for 78% of industry sales. IPMorgan Chase led in market share (21.7%), followed by Amex (19.9%), Citigroup (115%), Capital One (110%), Bank of America (83%), and Discover (47%)' The industry experienced 11% annual revenue growth between 2011 and 2016, and was expected to grow 45% annually between 2016 and 2021.5 Industry profit margins had dropped from 31% in 2011 to 25% in 2016 due to lower interest rates, increased competition, greater regulation, and security/ technology costs.6 Customer acquisition in the industry was competitive and expensive. Costs to acquire a new cardholder ranged from $250 to $500.7 American consumers held 636 million credit cards\" and 38% of households carried credit card revolving debt, which averaged roughly $11,000.9 On average, people carried 2.35 credit cards in their wallets (14% held seven or more cards)10 but generally only used one on a regular basis Thus, issuers strove to make their cards the preferred choice, or \"top of wallet.\" Generally speaking Amex network cardholders charged $1,687 per month on their cards, while Visa cardholders charged $843.\" Issuers had three main sources of revenue: cardholder fees, interest paid by consumers on unpaid card balancs, and interchange fees, which were paid by merchants as a percentage of each transaction amount. The contribution of each revenue source varied greatly from one issuer to another. For example, Amex, which required its charge card customers to pay all purchases in full each month, earned 21% of its revenue om interest payments and 79% om cardholder and interchange fees,12 2 This document is ammo tor ure onlyoy Lonoan Monty In 2021. For the exclusive use of L. Monty, 2021. Chan Sapphire: Grating a Millurlrial Cult Brand lm while J'PMorgarr Chase earned an estimated 70% of its revenue from interest payments and 30% from cardholder and interchange fees.13 Across the industry, about 30% of all customers were transacturs (those who paid their balances off in full each month to avoid paying interest fees), 43% were revolvers (those who did not pay off their balances in full each month), and 28% were dormant (those who carried, but did not use their cards frequently)\" Market Segmentation Issuers segmented the market in different ways in ord to identify different types of consumers. Common segmentation strategies included demographic, behavioral, and psychographic methods. Demographic segmentation separated consumers based on their life stage, assets, or credit score. 0 Life Stage Young adults (ages 1826) accounted for 15% of industry revenue.15 The 2660 age group accounted for 59% and tended to be more loyal.16 Senior citizens accounted for 15%, and the remainder (11%) was derived from business accounts" 0 Assets/Credit: The wealthy segment consisted of households with $500,000 to $1 million in assets, the afuent segment $100,000 to $500,000, and the emerging affluent segment consisted of those not yet afuent, but likely to be so within five to ten years.\" Afuent and wealthy consumers preferred to put most of their spending on credit cards and were a little less likely to carry revolving debt than the average consumer. Behavioral/ attitudinal segmentation provided insight into how consumers used their cards and how much they valued rewards and/ or what types of rewards they preferred (cash back, miles, points), as well as their channel preferences. For example: 0 Annual Fee: While most consumers did not pay an annual fee for credit cards, some issuers offered cards with annual fees of $25$550 to attract consumers that valued rich rewards and benefits 0 Rewards: Rewards were one of the key features consumers considered when selecting and using a credit card. There were currently three types of rewards cards in the market: Cash Back on Purchases: Cards that offered cash back attracted consumers who didn't want to spend time planning for and redeeming reward points. Some products offered higher percentages of cash back on spending in particular categories - Proprietary Rewards on Purchases: Issuers offered rewards in the form of points accumulated based on spending; point multiples varied for different categories of purchases. Points could be redeemed for travel benets, merchandise, or other perks. Cobranded Rewards on Purchases: Issuers partnered with particular hotels, airlines, retailers, and other merchants to offer cobranded cards that offered rewards affiliated with that partner. Points earned would typically be transferred to the cobrand partnecs loyalty program. These cards carried both the partner and the issuer brands. Recently, some issuers had increased their level of rewards and cobrand partner remuneration to a point where the costs of the rewards were approaching the interchange fee the issuer earned on the purchase. This oowrnem is authorlm to! me only oy London Monty in 2021. For the exclusive use of L. Monty, 2021. 51m Chane Sapphir: Creating: Millennial Cult Brand 0 Interest Rates or APR: Low interest rates appealed to consumers who wanted the option to extend payment on card purchases over time Average interest rates varied by card type and could range from 12.88% to over 20%.\" 0 Credit Lines: Some heavy spenders were drawn to cards with high credit lines that allowed them to access credit for big-ticket purchases in categories such as travel and home improvemmt, o Credilworthiness: Consumers with low credit scores were attracted to cards that offered a high likelihood of approval. These cards often carried higher interest rates and/ or annual fees to compensate for the higher level of risk the issuer incurred. A segmentation approach based on consumer psychographics offered yet another way to group consumers. McKinsey 5: Company identified five prominent segmenb based on consumers\" beliefs about and attitudes toward credit (see Exhibit 2 for segment descriptions and Exhibit 3 for how consumer behavior differed by card type)?\" A New Strategy for Chase Consumer Credit Cards In 2006, despite the size and protability of Chase Card Services, JPMorgan Chase CEO James \"Jamie" Dimon (HES MBA '82) believed that more should be done to strengthen Chase's proprietary products and to build a stronger presence for the company in the afuent market. In 2007, he hired Gordon Smith om Amex to become the (IO of Chase Card Services. Smith and Serra, who had also recently joined Chase, created a new strategy that rationalized the company's product portfolio and identified the need to create new Chase proprietary products to compete in the afuent market. Sena launched a substantial market research project. "It was clear we needed to deeply understand the various segments in the market, what features were attractive to those segments, and what kinds of products we wanted to build for those segments," she explained. The research conrmed the attractiveness of the affluent/ high net worth (AFF/l-NW) customer segment. According to company research, this group represented ~15% of the ~200 million US. cardholders, generating ~50% of total spending on credit cards, of which Chase was capturing ~15% market share. Sixty percent of AFF/HNW individuals lived in the top 15 markets inthe Us. that were Well'served by Chase branches. Competition in the afuent space was formidable. Travel cobranded credit card products, such as those for United and Delta Air Lines, had always been soong in the affluent market, but competition for proprietary issuer cards had been dominated by Amex. In 1984, Amex had introduced its Platinum Card, initially available by invihtion only, with a $250 annual fee. It offered 24-hour customer service, access to exclusive clubs, and special amenities at high-end hotels, resorts, and restaurants around the world.\" In 2007, Amex increased the annual fee to $450, but its extensive slate of rewards and perks allowed savvy users to recoup most of this cost.\" The Platinum Card's value proposition included exclusivity, rewards, and access. Amex referred to its customers as "card members,\" and all cards were embossed with a \"member since" date, which for many served as a badge of honor that marked the arrival of financial success and stability "For more than 30 years American Express has reaped enormous prots by telling its customers that they are successful, elite, the cream of the moneyed crop and t . t that there's no better way to make certain everyone knows just how special you are than by pulling an Amex out of your wallet," explained the New York Times}3 However, after reviewing consumer insights from her research, Serra questioned just how relevant the Amex brand was to the younger, emerging afuent consumer. She felt confident that Chase could compete for these affluent consumers with the right product and positioning, This document is anmorizod for use only by London Momy in 2021. For the exclusive use of L. Monty, 2021. Chou Sapphire: (Eating a Millennial Cult Brand 518024 Chase Sapphire: A New Sub-Brand Is Born In 2009, JPMorgan Chase consolidated its Chase proprietary card portfolio into five primary sub- brands to address distinct market segments: J'PMorgan (for private banking customers), Chase Sapphire (for afuent consumers interested in travel and dining), Chase Ink (for small business owners), Chase Freedom (for those consumers interested in cash back), and Chase Slate (for- consumers interested in building finandal responsibility). The Chase brand was used on all products as an endorser brand, which gave consumers a sense of trust, credibility, and security, according to Chief Brand Officer Susan Canavari, while each of the subbrands carried its own unique meaning. Serra recounted the discussion: \"There were people who felt that all of our products should just be called 'Chase.' That just didn't make sense to me. The market is highly segmented. Sub-branding allows you to speak directly to each target segment. I think it strengthens the Chase brand, broadening it and making it more relevant to more segments of consumers" In August 2009, Chase launched Chase Sapphire, its first Chase proprietary card marketed to the afuent consumer. A company statement articulated the value proposition of this new offering: For tuda'y's savvy ulucnt consumer, Guise Sapphire is the rim, next generation rewards card that combines the premium service and travel benets high-end consumers expect with practical features, so that they can always get more of what matters most. To enter the market, the team decided to offer a card with no annual fee. Consumers earned 1 point per dollar on general spend and 2 points per dollar on airline travel booked through Grase. Customers also received 10,000 bonus reward points after they spent $500 on the card during the first three months. To support all Chase proprietary products, including Sapphire, Chase launched Ultimate Rewards, a proprietary rewards program with a simple and transparent online portal where customers could manage their rewards, offers, and redemptionst It included a user-friendly landing page containing all of the information that a customer might need: point tracking progress toward program goals, and redemption options with point conversions listed so that customers could easily see the value of their points It was a clear differentiator, according to Canavari. \"Over the course of time, if you use the product, you will fall in love with it It's not like other cards that offer you things and when you try to use them, you can't actually redeem them When you go to redeem your points with us, you're going to be able to redeem them for great value at really great places,\" Lisa Walker, General Manager of Chase Sapphire Branded Orrds, added, \"Consumers believe that we deliver significant value and they like the elevated experiences and the simple nature of our rewards program. It is easy to understand and easy to redeem: no gotchas, rewards are automatically uedited to your account, You don't have to do anything.\" (See Exhibitd for images of the Ultimate Rewards website.) All Chase Sapphire calls were answered by a live advisort As Walker noted, "You don't have to push any buttons You don't have to enter your credit card numbert You simply call the number on the back of your card and someone answers the phone and says, 'Thank you for calling Chase Sapphire. How can] help you?' That is unique today in the credit card industry.\" Giase staffed the lines with experienced, high-performing repmentatives to improve customer satisfaction The teams had a goal of answering 85% of calls within 20 seconds and resolving customer issues within one call. \"It' s certainly a more expensive way of servicing our customers . . l but there is a clear connection between the service experience improvements, net promotor score improvements, and customer retention,\" said Tom Home, Head of Credit Card Operations, "The savings you get from pulling back on your service levels to save a few dollars is not worth the risk of lower customer satisfaction, which always leads to higher attrition\" He continued, \"Direct-to-advisor is attractive to many customers, These customers are very busy, and so their immediate reaction is 'l'm going to get a quick answer to my question!\" This document is authorized tor use onlyby London Manly in 2021. For the exclusive use of L. Monty, 2021. 51m Chase Sapphire: Geatinga Milluuiial one Brand The card had a minimalist design (see Figure 1), differentiating it from competitors' cards, which were lled with numbers and graphics. Figure 1 Giase Sapphire Credit Card Source: Company documents. The market response was promising. A customer survey at the end of 2009 revealed that 90% of cardholders reported overall satisfaction with the card, and 85% would recommend it to others.\" Expanding the Product Portfolio with Chase Sapphire Preferred By 2011, the economy was showing signs of recovery. Although Sapphire had generated consumer excitement and was performing well, Serra was anxious to make stronger inroads into the AFF/l-lNW segment The team decided to leverage the Giase Sapphire subbrand and launched the Chase Sapphire Preferred card, It carried an annual fee of $95 and offered cardholders 50,000 points after they spent $4,000 during the first three months. The card also provided a 1.25% pointsto-dollar conversion rate toward travel if points were redeemed on the Ultimate Rewards website (for example, when 50,000 points were redeemed, consumers would receive $625 in value against their travel purchases). Cardholders could earn 2x points on travel and dining and received a 1:1 point transfer to frequent ier programs, such as United Mileage Plus. Preferred customers also had access to exclusive, curated Chase Experiences such as exclusive packages to the Sundance Film Festival, private dining series at acclaimed restaurants, and access to the Sapphire Lounge at New York City s Madison Square Garden, where customers could meet athletes and talent before games and shows. One of the card's dening characteristics was its weight. Unlike molded plastic cards, Chase Sapphire Preferred had a metal core sandwiched between two pieces of plastic, giving it more heft. While a standard plastic card generally cost $1 to produce, this card cost significantly more. However, the team felt that the satisfying \"thunk\" it made as a consumer put it down for payment was an important quality signal. Remarked Walker, \"When I look at my P&L, that' s a pretty big cost of goods number, But ithas an intangible value, When I take my Chase Sapphire Preferred card out of my wallet and hand it to someone in a store, they make a comment about it. It isn't showy, but it is a conversation piece.\" A NerdWallet writer explained, \"I have the Chase Sapphire Preferred, and virtually nothing gives me more pleasure when I pay and the cashier notices how gorgeous that card is. Chase has basically realized that the weight raises customers' dopamine levels. Being able to get into my brain every single time I swipe a cardthere's literally nothing better a marketer could want.\"25 A consumer noted, \"They've managed to take something from being a stupid card you carry in your wallet to a part of your identity,\" 15 This dowmem is authorized tor use only by London Monty in 20m. For the exclusive use of L. Monty, 2021. Chase Sapphire: Creating a Millennial Cult Brand lm In 2014, Chase stopped actively acquiring customers and began throttling back marketing efforts on the no-fee product, focusing marketing on the Sapphire Preferred product instead Some no-fee consumers migrated to Preferred, but others stayed with the nofee card, moved to one of Chase's other subbranded cards, or left the company. By 2016, Sapphire Preferred represented more than half of Sapphire total accounts and sales. The Sapphire Preferred card had also won several awards. Consumers were enthusiastic about the brand and eager to share it with their tribe. Said Canavan', \"When you are passionate about something, you want to share it with your community and with like-minded people because that's what makes you really proud to be part of a brand." By 2014, Citi had also entered the premium credit card segment with its Citi Prestige card. The Prestige card, marketed primarily to travelers, carried a $450 annual fee and access to Priority Pass airport lounges27 Cardholders received an anniml $250 air travel credit, automatically applied to ight- related expenses. They also received a tree fourth night at a hotel in the form of a statement credit when booked through the Citi Prestige Concierge}8 a sign-up bonus of 50,000 ThankYou points after spending $5,000 within three months of being issued the card, and three points per dollar spent on air travel and hotels, two points per dollar on dining and entertainment, and 1 point per dollar spent on other purchases.\" The Launch of the Chase Sapphire Reserve Card Codispoti joined Chase in 2014, after more than 18 years at Amex. She quickly noticed that Sapphire Preferred customers were more afuent than the rest of Chase's proprietary portfolio, and included a segment of \"new afuents\" that were 7544 years old with incomes of $150,000+. They were authentic travelers and savvy about rewards, and they liked to make the most of every trip, whether it was around the comet or across the globe. The team believed there was an opportunity to build on the momentum and brand equity of Sapphire to create a line extension to compete in the ultra-premium, high-fee segment Product Design Strategy Codispoti explained, "Launching a new credit card product is a complex series of trade-offs. We have to construct a value proposition comprised of the optimal mix of rewards, benets, services, experience, interest rates, annual fees, and more Throughout the new product development process we are constantly doing analysis to determine which set of features will deliver the most value for consumers, provide clear differentiation from competition, and yield the best returns for our company.\" Since the new offering would carry the Chase Sapphire brand, it needed to reect the brand's DNA: strong rewards, premium travel redemptions, and exceptional customer service. In addition, not only did it need to differentiate itself from other ultra-premium cards in the market, it also needed to be distinct from the Giase Sapphire Preferred card to generate incremental customers. (Refer to Exhibit 5 for a summary of each Sapphire product's features) Codispoti also knew she needed to account for and overcome two significant industry dynamics in developing a new product: millennial attitudes toward credit cards and churnerst First, by 2013, only 37% of Americans aged 35 and under carried credit card debt, the lowest level since 1989.\" Millennials, many of whom carried significant student loan debt, were wary of revolving credit and tended to use debit cards or pay off their full balance each month. Their spending habits This document is authorized tor usa only by London Monty in 20m. For the exclusive use of L. Monty, 2021. 518424 Chase Sapphire: Creanga Millennial Cult Brand differed from past generations, as they tended to favor collecting experiences instead of things, and much of their spending occurred in places that were not traditionally included in reward programs. However, while some had sworn off credit cards, others were attracted by rewards. The Wall Street IDumnI noted, \"Credit cards, and the prizes they earn, are the hot new collectibles for millennials.\"31 Millennials capitalized on rewards to stretch their nances, hacking the system to maximize the points they earned and the value at which they redeemed them Second, an increasing number of consumers were churning credit card offerings for large personal gains, This small subset of customers known as \"churners\" signed up for multiple credit cards to take advantage of acquisition sign-on bonuses, first-year free offers, or low introductory interest rates and then canceled the account or allowed the card to sit unused and became part of the dormant segment. Prominent bloggers offered ingenious methods for consumers to maximize the benets of their credit cards, As Codispoti noted, "We work hard to deliver compelling ongoing benets well beyond the signon bonus so our cards remain top of wallet for the long term,\" The new Chase Sapphire Reserve card was launched in August 2016 and carried a $450 annual fee, Cardholders earned 3 points per dollar spent on travel and dining, a 15% points-todollar conversion rate toward travel on Ultimate Rewards redemptions, a $300 annual travel credit, and access to the Chase Experiences platform At launch, Chase Sapphire Reserve offered a market-leading 100,000- point sign-on bonus, which was earned after a customer spent $4,000 Within their first three months, The bonus offer alone was worth $1,500 in travel redemption credits on the rewards site' For Codispoti, what made the Sapphire brand so compelling was that it reflected what young, successful consumers wanteda exible product that allowed them to set their own rules and that provided convenience, relevance, and choice. \"For millennials, 'travel' might mean a mime-lifetime trip around the world or it could mean taking a Lyft to a holein-thewall restaurant in Giinatown and then riding the subway to karaoke, and then catching a taxi home. So we decided to give customers accelerated rewards on all those purchases Reserve provided millennials even more of what they loved about Sapphire This is a card for accumulating experiences,\" she explained. "The emphasis is on what you can do, rather than what you can buy." She added, \"Our card is for those on a lifelong journey of exploration, as opposed to a card that serves as a badge of arrival, Our card is meant for people who want to be viewed as interesting, not rich." At launch, the Sapphire team created a new approach for marketing and communications. They recognized that afuent millennial consumers were consuming media differently, so rather than investing in traditional television advertising, they turned to media platforms and inuencers that were more pertinent to them. They engaged relevant influencers, who spread the word within their communities, partnering with model/ producer] director Nigel Barker, designer Kelly Wearstler, and model/ TV personality Guissy Teigen to help generate largescale reach (see Exhibit 6). The celebrities shared their Chase Sapphire Reserve experiences through more than 20 unique and highly engaging pieces of social content delivered to their millions of followers on social media, and hosted a media event to discuss their unique perspectives on the evolution of travel. Chase blanketed its extensive branch network with point-of-sale material promoting the product, featured the card on its chasecom website, and advertised with online video content on sites like VOX media that featured actor and comedian James Corden interviewing cutting-edge masters of travel and dining in unique venues. Said Canavari, \"I think the way we went to market was really smart. We created this sense that it was limited, you had to be in the know to get it. We didn't start with mass advertising . . . We wanted it to feel a little bit exclusive.\" This document is authorized muse only by London Monty in 202l. For the exclusive use of L. Monty, 2021. Chase Sapphire Geang a Millurnial Cult Brand 518024 Market Response In August 2016, The Points Guy wrote, "When I first heard the details of the new Chase Sapphire Reserve Card, I had to sit down, because it sounded way too good to be true\": Fueled by social media and online forums, news about the new card spread quickly to \"points junkies\" eager to apply for the card and spread the word. Demand skyrocketed, overwhelming Chase's call centers. Some consumers called in just to ask if the 100,000

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance