Answered step by step

Verified Expert Solution

Question

1 Approved Answer

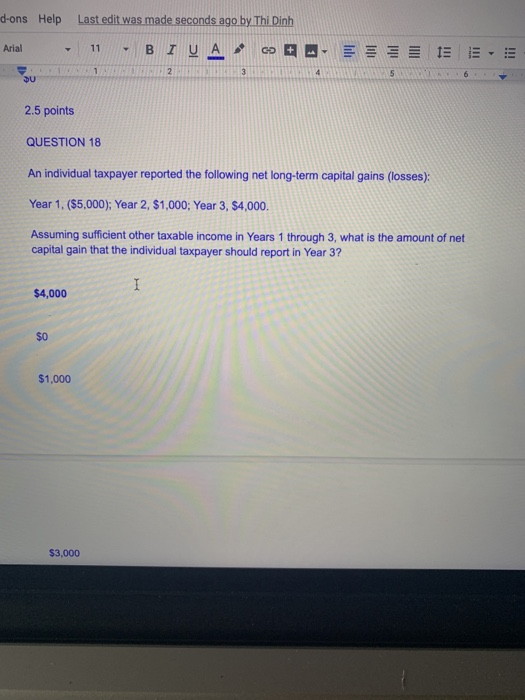

d-ons Help Last edit was made seconds ago by Thi Dinh Arial 11 BIU A co + im TIT ili 1 2 3 4 5A

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Using Microcomputers In Managerial Accounting

Authors: George Hildebrand

1st Edition

0938188275, 978-0938188278