Question

DROP DOWN ANSWER OPTIONS: Straight life / direct / unlimited Single premium / continuous premium / limited payment $140,000 / $120,000 / $60,000 / $200,000

DROP DOWN ANSWER OPTIONS:

-

Straight life / direct / unlimited

-

Single premium / continuous premium / limited payment

-

$140,000 / $120,000 / $60,000 / $200,000 / $10,000

-

In addition to / but would forfeit

-

$120,000 / $60,000 / $140,000 / $200,000 / $10,000

6. $120,000 / $60,000 / $35,000 / $10,000 / $200,000

7. Convertibility provision / nonforfeiture right / renewability provision

8. True / false

DROP DOWN ANSWER OPTIONS:

-

Straight life / direct / unlimited

-

Single premium / continuous premium / limited payment

-

$140,000 / $120,000 / $60,000 / $200,000 / $10,000

-

In addition to / but would forfeit

-

$120,000 / $60,000 / $140,000 / $200,000 / $10,000

6. $120,000 / $60,000 / $35,000 / $10,000 / $200,000

7. Convertibility provision / nonforfeiture right / renewability provision

8. True / false

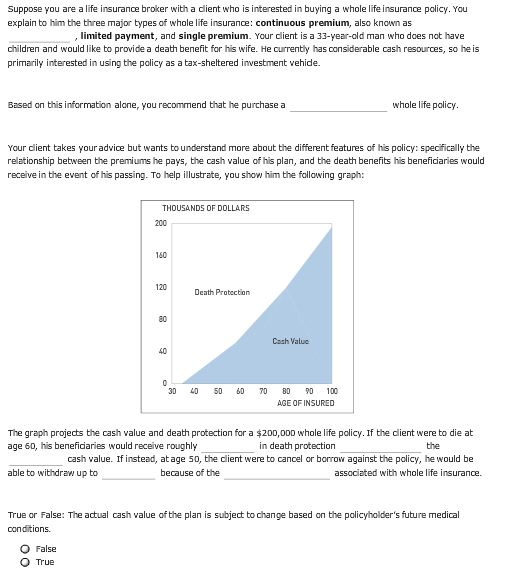

Suppose you are a life insurance broker with a client who is interested in buying a whole life insurance policy. You explain to him the three major types of whole life insurance: continuous premium, also known as limited payment, and single premium. Your client is a 33-year-old man who does not have children and would like to provide a death benefit for his wife. He currently has considerable cash resources, so he is primarily interested in using the policy as a tax-sheltered investment vehide. Based on this information alone, you recommend that he purchase a whole life policy. Your client takes your advice but wants to understand more about the different features of his policy: specifically the relationship between the premiums he pays, the cash value of his plan, and the death benefits his benefidaries would receive in the event of his passing. To help illustrate, you show him the following graph: THOUSANDS OF DOLLARS Death Protection Cash Value 30 40 50 60 70 80 90 100 AGE OF INSURED The graph projects the cash value and death protection for a $200,000 whole life policy. If the client were to die at age 60, his beneficiaries would receive roughly in death protection the cash value. If instead, at age 50, the client were to cancel or borrow against the policy, he would be able to withdraw up to because of the associated with whole life insurance True or False: The actual cash value of the plan is subject to change based on the policyholder's future medical conditions O False O True Suppose you are a life insurance broker with a client who is interested in buying a whole life insurance policy. You explain to him the three major types of whole life insurance: continuous premium, also known as limited payment, and single premium. Your client is a 33-year-old man who does not have children and would like to provide a death benefit for his wife. He currently has considerable cash resources, so he is primarily interested in using the policy as a tax-sheltered investment vehide. Based on this information alone, you recommend that he purchase a whole life policy. Your client takes your advice but wants to understand more about the different features of his policy: specifically the relationship between the premiums he pays, the cash value of his plan, and the death benefits his benefidaries would receive in the event of his passing. To help illustrate, you show him the following graph: THOUSANDS OF DOLLARS Death Protection Cash Value 30 40 50 60 70 80 90 100 AGE OF INSURED The graph projects the cash value and death protection for a $200,000 whole life policy. If the client were to die at age 60, his beneficiaries would receive roughly in death protection the cash value. If instead, at age 50, the client were to cancel or borrow against the policy, he would be able to withdraw up to because of the associated with whole life insurance True or False: The actual cash value of the plan is subject to change based on the policyholder's future medical conditions O False O TrueStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Inflation Growth And International Finance

Authors: Alec Cairncross

1st Edition

113865308X, 978-1138653085