Answered step by step

Verified Expert Solution

Question

1 Approved Answer

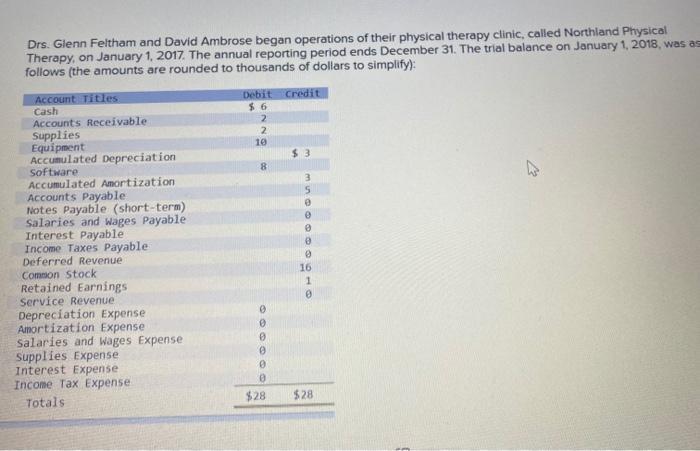

Drs. Glenn Feltham and David Ambrose began operations of their physical therapy clinic, called Northland Physical Therapy, on January 1, 2017. The annual reporting

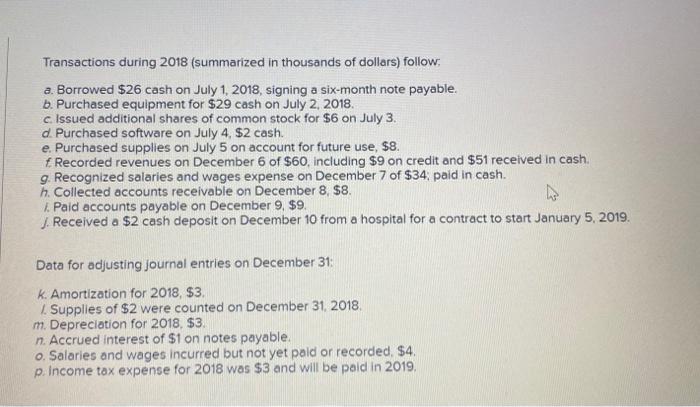

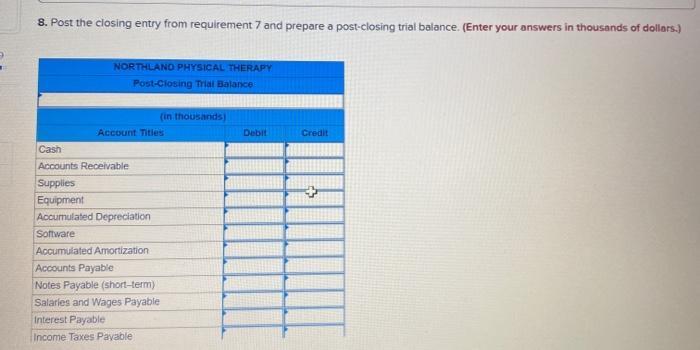

Drs. Glenn Feltham and David Ambrose began operations of their physical therapy clinic, called Northland Physical Therapy, on January 1, 2017. The annual reporting period ends December 31. The trial balance on January 1, 2018, was as follows (the amounts are rounded to thousands of dollars to simplify): Account Titles Cash Debit $ 6 Credit Accounts Receivable Supplies Equipment Accumulated Depreciation Software Accumulated Amortization Accounts Payable Notes Payable (short-term) Salaries and wages Payable Interest Payable Income Taxes Payable Deferred Revenue 2. 10 16 Common Stock Retained Earnings Service Revenue Depreciation Expense Amortization Expense Salaries and wages Expense Supplies Expense Interest Expense Income Tax Expense Totals $28 $28 Transactions during 2018 (summarized in thousands of dollars) follow: a. Borrowed $26 cash on July 1, 2018, signing a six-month note payable. b. Purchased equipment for $29 cash on July 2, 2018. c Issued additional shares of common stock for $6 on July 3. d. Purchased software on July 4, $2 cash. e. Purchased supplies on July 5 on account for future use, $8. f Recorded revenues on December 6 of $60, including $9 on credit and $51 received in cash. g. Recognized salaries and wages expense on December 7 of $34, paid in cash. h. Collected accounts receivable on December 8, $8. I. Paid accounts payable on December 9, $9. J. Received a $2 cash deposit on December 10 from a hospital for a contract to start January 5, 2019. Data for adjusting journal entries on December 31: k. Amortization for 2018, $3. 1. Supplies of $2 were counted on December 31, 2018. m. Depreciation for 2018, $3. n. Accrued interest of $1 on notes payable. o. Salaries and wages incurred but not yet pald or recorded, $4. p. Income tax expense for 2018 was $3 and will be peid in 2019. 8. Post the closing entry from requirement 7 and prepare a post-closing trial balance. (Enter your answers in thousands of dollars.) NORTHLANO PHYSICAL THERAPY Post-Closing Trial Balance (in thousands) Account Titles Debit Credit Cash Accounts Receivable Supplies Equipment Accumulated Depreciation Software Accumulated Amortization Accounts Payable Notes Payable (short-term) Salarles and Wages Payable Interest Payable Income Taxes Payable

Step by Step Solution

★★★★★

3.39 Rating (140 Votes )

There are 3 Steps involved in it

Step: 1

Date Journal Debit Credit In thousands In thousands July 12018 Cash 13 Note payable 13 Borrowed through note payable July 22018 Equipment 16 Cash 16 P...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Document Format ( 2 attachments)

60966d4528301_211087.pdf

180 KBs PDF File

60966d4528301_211087.docx

120 KBs Word File

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Fundamentals of Financial Accounting

Authors: Fred Phillips, Robert Libby, Patricia Libby

6th edition

1259864235, 1259864230, 1260159547, 126015954X, 978-1259864230