Answered step by step

Verified Expert Solution

Question

1 Approved Answer

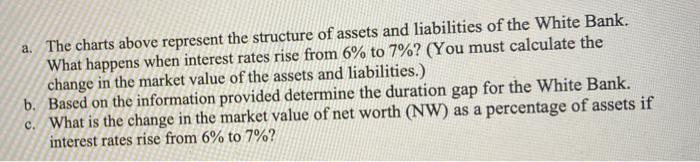

Duration in years Amounts in millions Assets EUR Loans and advances to central banks and administrations Loans and advances to credit institutions Loans and

Duration in years Amounts in millions Assets EUR Loans and advances to central banks and administrations Loans and advances to credit institutions Loans and advances to customers Financial assets held for trading Fixed-income securities 0.4 58,729 427,179 191,608 22,189 194,693 19,419 3 1 2.4 Variable-yield securities Real estate assets and other assets 1.1 7 040 TAL 930,858 Liabilities Duration in years Amounts in millions EUR Amounts owed to central banks Amounts owed to credit institutions 0.4 1.2 46,865 429,565 279,027 77,692 21,840 6,230 14,712 15,914 39,012 930,858 Amounts owed to customers Debts evidenced by certificates Liabilities held for trading 0.8 2.3 0.6 Provisions Subordinated liabilities 1.6 Other liabilities 3. Capital and reserves TOTAL a. The charts above represent the structure of assets and liabilities of the White Bank. What happens when interest rates rise from 6% to 7%? (You must calculate the change in the market value of the assets and liabilities.) b. Based on the information provided determine the duration gap for the White Bank. c. What is the change in the market value of net worth (NW) as a percentage of assets if interest rates rise from 6% to 7%?

Step by Step Solution

★★★★★

3.45 Rating (164 Votes )

There are 3 Steps involved in it

Step: 1

Given interest rates rise from 6 to 7 The total asset value is 930857 million and the total liability value is 891845 million excluding capital a change in market value of Assets Liabilities sensitivi...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Accounting and Auditing Research Tools and Strategies

Authors: Thomas Weirich, Thomas Pearson, Natalie Tatiana

9th edition

1119441915, 1119441919, 978-1-119-3737, 9781119373629 , 978-1119441915