Question

Duration Matching with a Swap Consider a bank with the following balance sheet: Value of Assets: V A = $10,000 Duration of Assets: D A

Duration Matching with a Swap

Consider a bank with the following balance sheet:

Value of Assets: VA = $10,000

Duration of Assets: DA = 4.2 yrs

Value of Liabilities: VL = $20,000

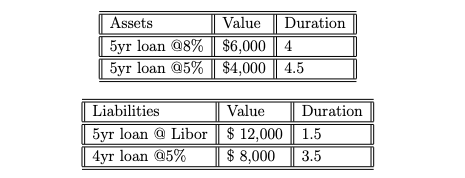

a) Suppose you want to reduce duration gap to zero by using a swap. In particular, you can swap a portion of the 4yr loan @5% liability with a 4yr loan @Libor liability. The duration of the 4yr loan @Libor liability is 2 years. Find the swap size that reduces duration gap to zero.

Assets Value Duration 5yr loan @8% $6,000 4 5yr loan 25% $4,000 4.5 Liabilities Value Duration 5yr loan @ Libor $ 12,000 1.5 4yr loan @5% $ 8,000 3.5 Assets Value Duration 5yr loan @8% $6,000 4 5yr loan 25% $4,000 4.5 Liabilities Value Duration 5yr loan @ Libor $ 12,000 1.5 4yr loan @5% $ 8,000 3.5Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Handbook Of EDP Auditing

Authors: Michael A. Murphy, Xenia Ley Parker

2nd Edition

0791304116, 978-0791304112