Answered step by step

Verified Expert Solution

Question

1 Approved Answer

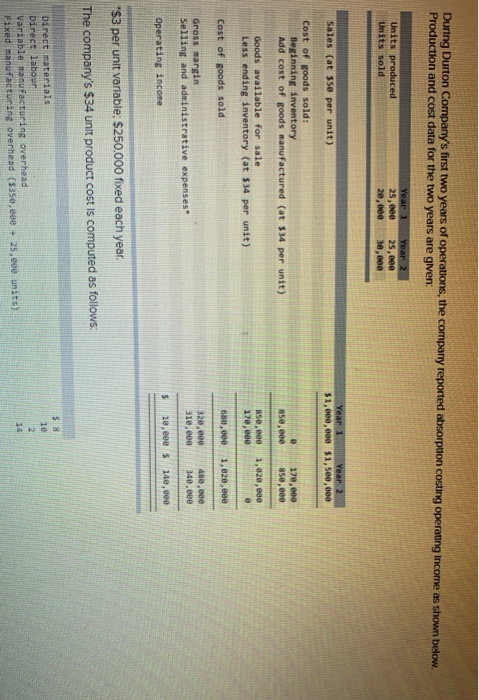

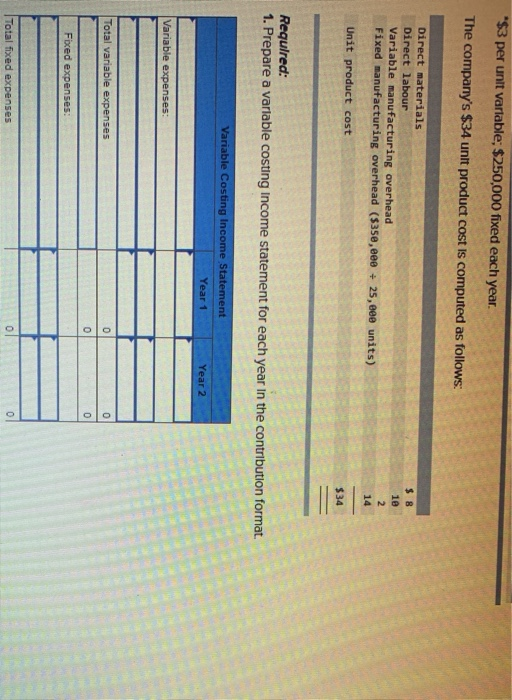

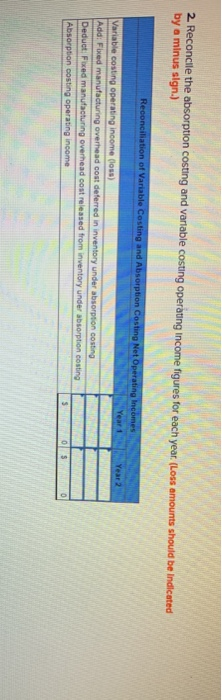

During Durton Company's first two years of operations, the company reported absorption costing operating income as shown below. Production and cost data for the two

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Auditing Your Human Resources Department A Step By Step Guide To Assessing The Key Areas Of Your Program

Authors: John H. McConnell

2nd Edition

0814416616, 978-0814416617