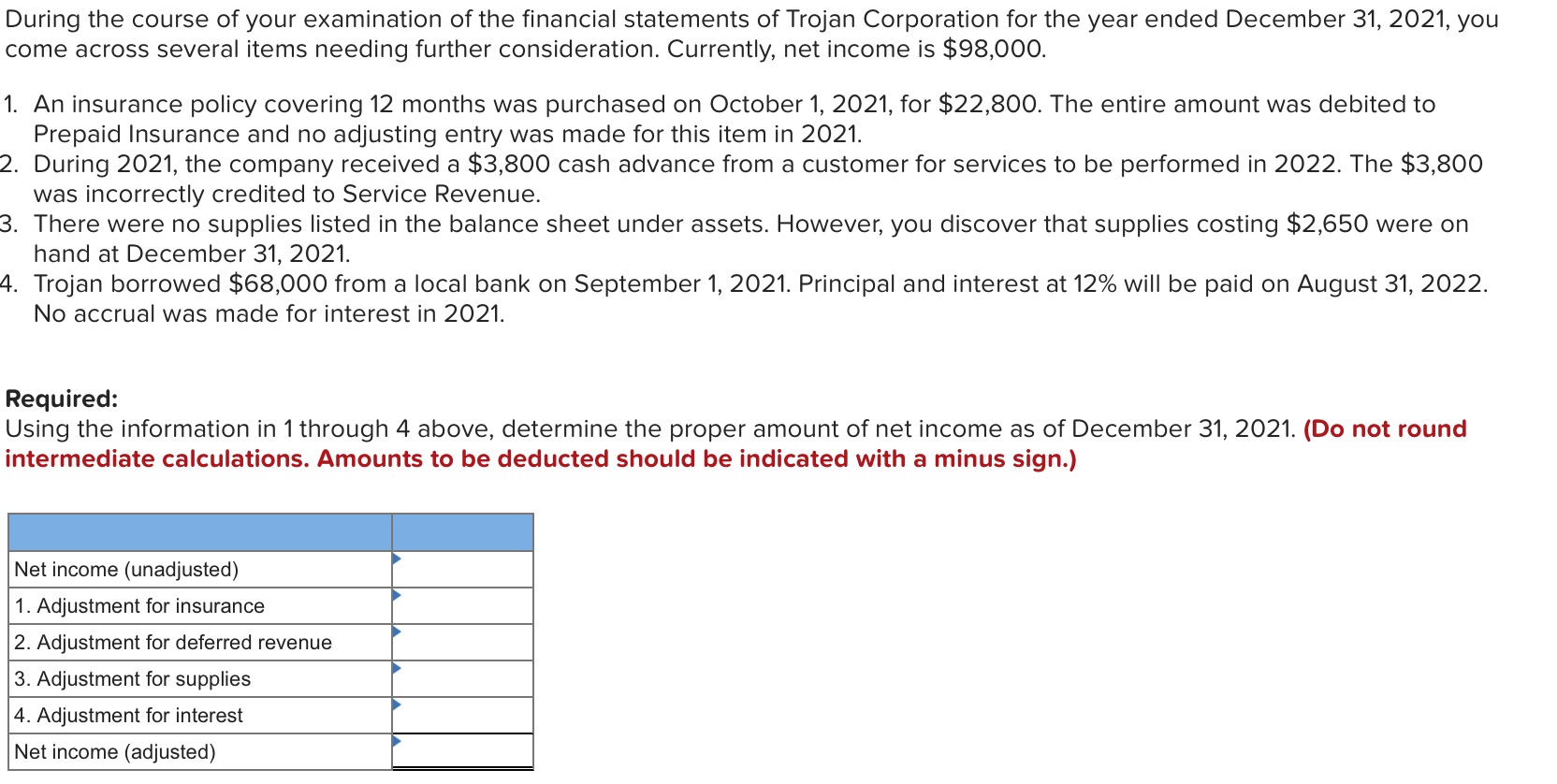

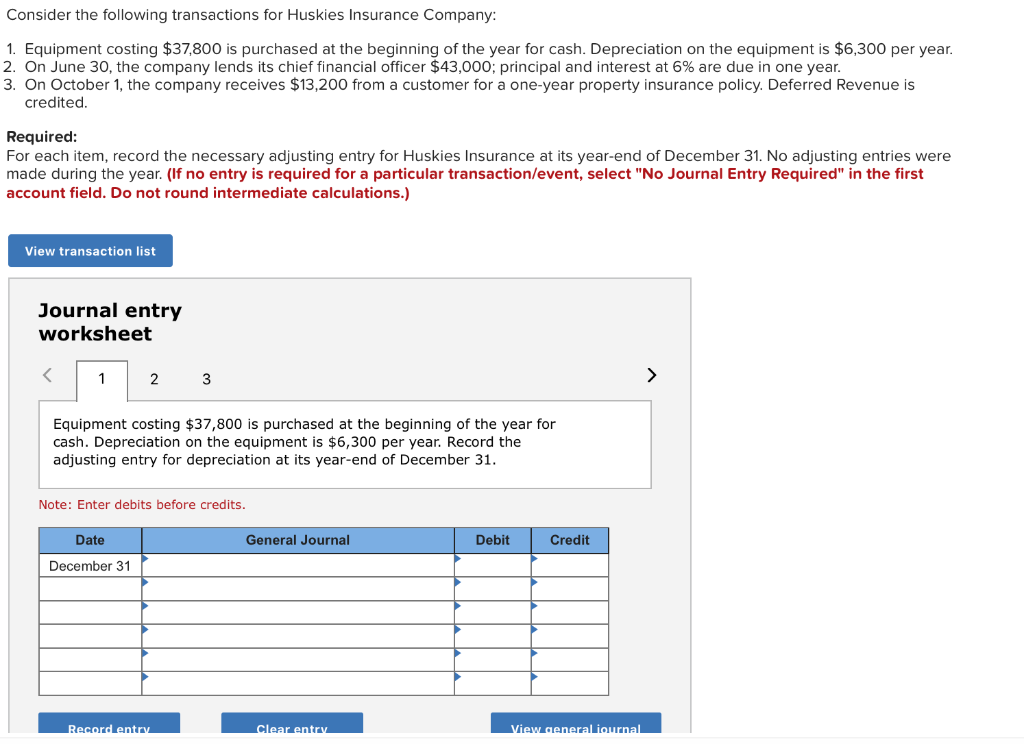

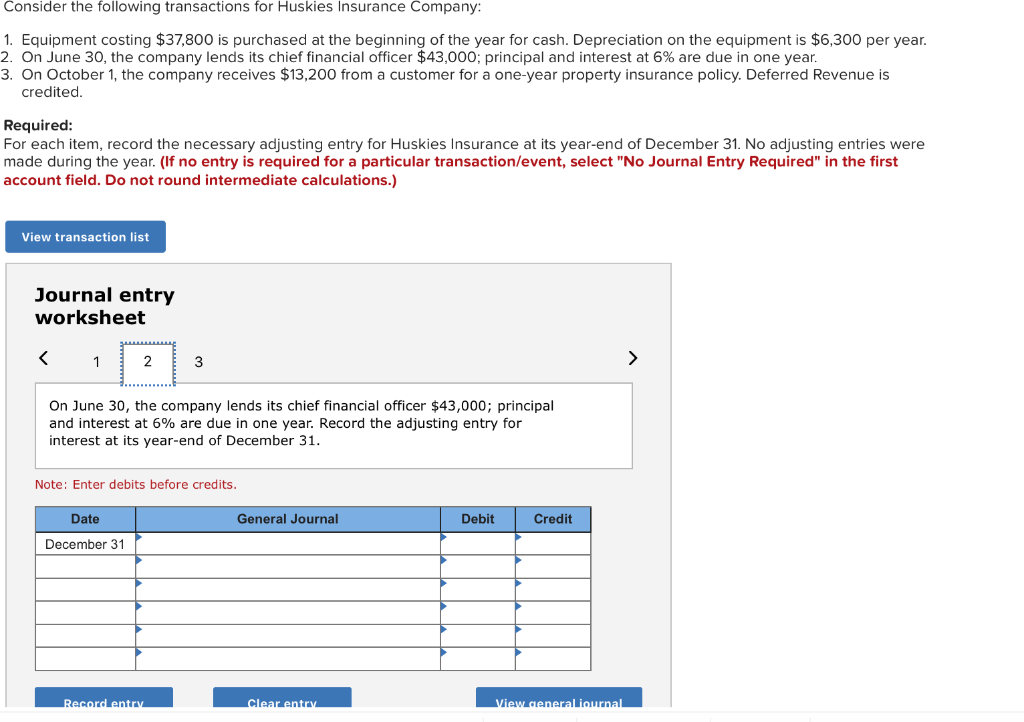

During the course of your examination of the financial statements of Trojan Corporation for the year ended December 31, 2021, you come across several items needing further consideration. Currently, net income is $98,000. 1. An insurance policy covering 12 months was purchased on October 1, 2021, for $22,800. The entire amount was debited to Prepaid Insurance and no adjusting entry was made for this item in 2021. 2. During 2021, the company received a $3,800 cash advance from a customer for services to be performed in 2022. The $3,800 was incorrectly credited to Service Revenue. 3. There were no supplies listed in the balance sheet under assets. However, you discover that supplies costing $2,650 were on hand at December 31, 2021. 4. Trojan borrowed $68,000 from a local bank on September 1, 2021. Principal and interest at 12% will be paid on August 31, 2022. No accrual was made for interest in 2021. Required: Using the information in 1 through 4 above, determine the proper amount of net income as of December 31, 2021. (Do not round intermediate calculations. Amounts to be deducted should be indicated with a minus sign.) Net income (unadjusted) 1. Adjustment for insurance 2. Adjustment for deferred revenue 3. Adjustment for supplies 4. Adjustment for interest Net income (adjusted) Consider the following transactions for Huskies Insurance Company: 1 Equipment costing $37,800 is purchased at the beginning of the year for cash. Depreciation on the equipment is $6,300 per year. 2. On June 30, the company lends its chief financial officer $43,000; principal and interest at 6% are due in one year. 3. On October 1, the company receives $13,200 from a customer for a one-year property insurance policy. Deferred Revenue is credited Required: For each item, record the necessary adjusting entry for Huskies Insurance at its year-end of December 31. No adjusting entries were made during the year. (If no entry is required for a particular transaction/event, select "No Journal Entry Required" in the first account field. Do not round intermediate calculations.) View transaction list Journal entry worksheet > 1 2 Equipment costing $37,800 is purchased at the beginning of the year for cash. Depreciation on the equipment is $6,300 per year. Record the adjusting entry for depreciation at its year-end of December 31 Note: Enter debits before cred its. Debit Date Credit General Journal December 31 Record entry Clear entr View general iournal. Consider the following transactions for Huskies Insurance Company: 1. Equipment costing $37,800 is purchased at the beginning of the year for cash. Depreciation on the equipment is $6,300 per year. 2. On June 30, the company lends its chief financial officer $43,000; principal and interest at 6% are due in one year 3. On October 1, the company receives $13,200 from a customer for a one-year property insurance policy. Deferred Revenue is credited Required: For each item, record the necessary adjusting entry for Huskies Insurance at its year-end of December 31. No adjusting entries were made during the year. (If no entry is required for a particular transaction/event, select "No Journal Entry Required" in the first account field. Do not round intermediate calculations.) View transaction list Journal entry worksheet 2 1 On June 30, the company lends its chief financial officer $43,000; principal and interest at 6% are due in one year. Record the adjusting entry for interest at its year-end of December 31 Note: Enter debits before cred its. Date General Journal Debit Credit December 31 Record entry Clear entry View generaliournal Consider the following transactions for Huskies Insurance Company: 1. Equipment costing $37,800 is purchased at the beginning of the year for cash. Depreciation on the equipment is $6,300 per year. 2. On June 30, the company lends its chief financial officer $43,000; principal and interest at 6% are due in one year. 3. On October 1, the company receives $13,200 from a customer for a one-year property insurance policy. Deferred Revenue is credited. Required: For each item, record the necessary adjusting entry for Huskies Insurance at its year-end of December 31. No adjusting entries were made during the year. (If no entry is required for a particular transaction/event, select "No Journal Entry Required" in the first account field. Do not round intermediate calculations.) View transaction list Journal entry worksheet K 1 2 3 On October 1, the company receives $13,200 from a customer for a one year property insurance policy. Deferred Revenue is credited. Record the adjusting entry for deferred revenue at its year-end of December 31 Note: Enter debits before credits. Debit Credit Date General Journal December 31 Clear entrv Record entry View general iournal Consider the following transactions for Huskies Insurance Company: 1. Equipment costing $30,600 is purchased at the beginning of the year for cash. Depreciation on the equipment is $5,100 per year. 2. On June 30, the company lends its chief financial officer $31,000; principal and interest at 7% are due in one year. 3. On October 1, the company receives $8,400 from a customer for a one-year property insurance policy. Deferred Revenue is credited Required: Indicate by how much net income in the income statement is higher or lower if the adjustment is not recorded. (Do not round intermediate calculations.) Transaction Net Income 1 2. 3. Total