Answered step by step

Verified Expert Solution

Question

1 Approved Answer

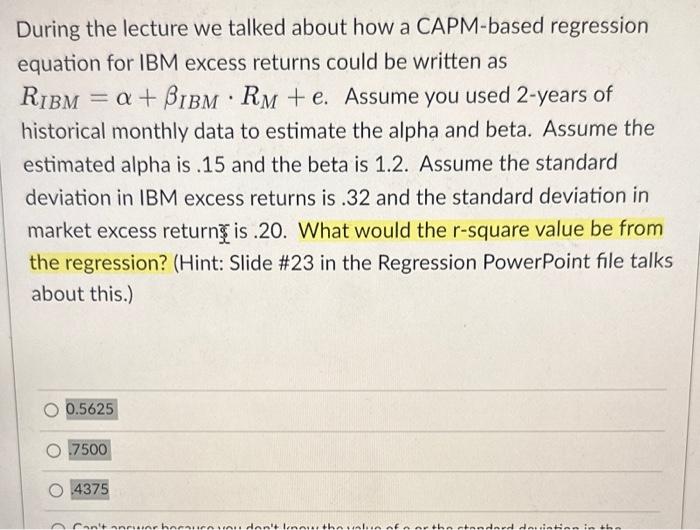

During the lecture we talked about how a CAPM-based regression equation for IBM excess returns could be written as RIBM=+IBMRM+e. Assume you used 2-years of

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Study Guide To Accompany Corporate Finance

Authors: Jonathan Berk, Peter DeMarzo, Mark Simonson

1st Edition

0321388682, 9780321388681