Answered step by step

Verified Expert Solution

Question

1 Approved Answer

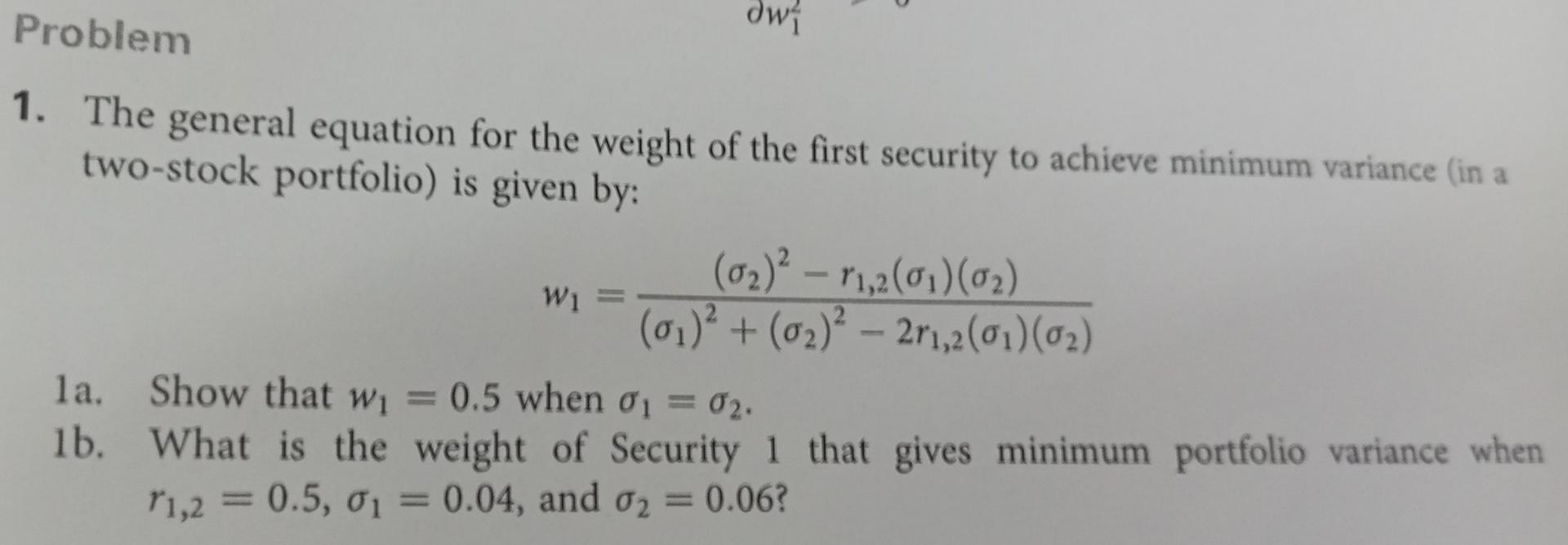

dwi Problem 1. The general equation for the weight of the first security to achieve minimum variance (in a two-stock portfolio) is given by: (0)

dwi Problem 1. The general equation for the weight of the first security to achieve minimum variance (in a two-stock portfolio) is given by: (0) - 11,2(01) (0) W = (0) + (0) - 2r,2(01)(0) la. Show that w = 0.5 when = 02. 1b. What is the weight of Security 1 that gives minimum portfolio variance when 71,2 = 0.5, 0 = 0.04, and o2 = 0.06? 01

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Fundamentals Of Financial Management

Authors: James C. Van Horne

10th Edition

0138596875, 978-0138596873