Question: E 4. (20 points) You consider an ARMA(1,2) model, Te = do + 11-1+4-016-1 - 022, & ~D(0,0%), where e is a white noise process,

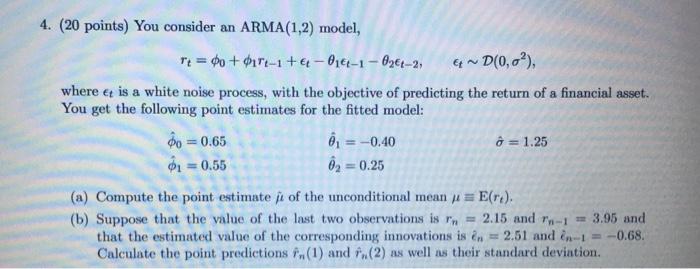

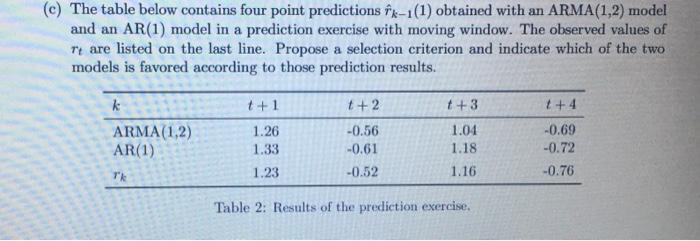

E 4. (20 points) You consider an ARMA(1,2) model, Te = do + 11-1+4-016-1 - 022, & ~D(0,0%), where e is a white noise process, with the objective of predicting the return of a financial asset. You get the following point estimates for the fitted model: Do = 0.65 , = -0.40 3 =1.25 01 = 0.55 02 = 0.25 a (a) Compute the point estimate fi of the unconditional mean x = E(re). (b) Suppose that the value of the last two observations is n = 2.15 and -1 = 3.95 and that the estimated value of the corresponding innovations is n = 2.51 and in-1 = -0.68. Calculate the point predictions (1) and (2) as well as their standard deviation, (c) The table below contains four point predictions fx-1(1) obtained with an ARMA(1,2) model and an AR(1) model in a prediction exercise with moving window. The observed values of rt are listed on the last line. Propose a selection criterion and indicate which of the two models is favored according to those prediction results. t +3 t +4 k ARMA(1,2) AR(1) * t+1 1.26 1.33 1.23 t + 2 -0.56 -0.61 -0.52 1.04 1.18 -0.69 -0.72 -0.76 1.16 Table 2: Results of the prediction exercise. E 4. (20 points) You consider an ARMA(1,2) model, Te = do + 11-1+4-016-1 - 022, & ~D(0,0%), where e is a white noise process, with the objective of predicting the return of a financial asset. You get the following point estimates for the fitted model: Do = 0.65 , = -0.40 3 =1.25 01 = 0.55 02 = 0.25 a (a) Compute the point estimate fi of the unconditional mean x = E(re). (b) Suppose that the value of the last two observations is n = 2.15 and -1 = 3.95 and that the estimated value of the corresponding innovations is n = 2.51 and in-1 = -0.68. Calculate the point predictions (1) and (2) as well as their standard deviation, (c) The table below contains four point predictions fx-1(1) obtained with an ARMA(1,2) model and an AR(1) model in a prediction exercise with moving window. The observed values of rt are listed on the last line. Propose a selection criterion and indicate which of the two models is favored according to those prediction results. t +3 t +4 k ARMA(1,2) AR(1) * t+1 1.26 1.33 1.23 t + 2 -0.56 -0.61 -0.52 1.04 1.18 -0.69 -0.72 -0.76 1.16 Table 2: Results of the prediction exercise

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts