Question

(e) Find the weights for two risky assets S and B in the optimal risky/tangency portfolio P* (f) What is the expected return and the

(e) Find the weights for two risky assets S and B in the optimal risky/tangency portfolio P*

(f) What is the expected return and the standard deviation of the optimal risky/tangency portfolio P*

(g) If a customer risk aversion A is 0.37 and whats to invest $10000, how should she invest? (how much money should she allocate to the stock S, the bond B, and the T-bill T?)

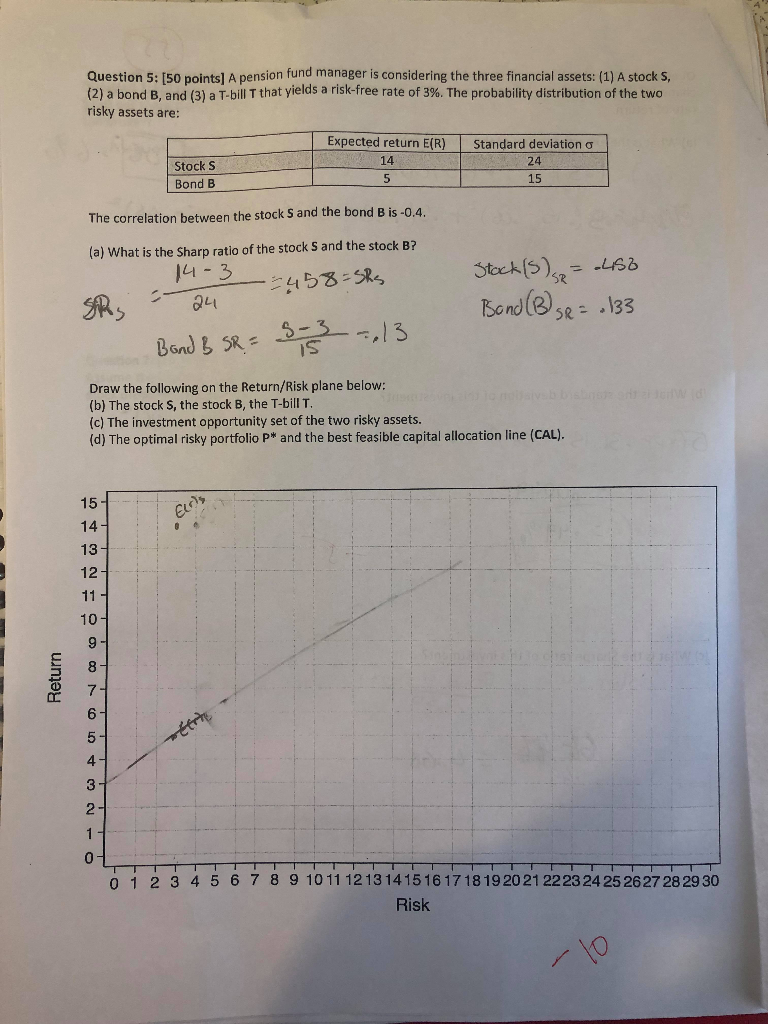

Question 5: [50 points] A pension fund manager is considering the three financial assets: (1) A stock S, (2) a bond B, and (3) a T-bill T that yields a risk-free rate of 3%. The probability distribution of the two risky assets are: Expected return E(R) Standard deviation a 14 24 Stock S 5 15 Bond B The correlation between the stock S and the bond B is -0,4 (a) What the Sharp ratio of the stock S and the stock B? Sechs) Bond(es 4-3 =58-SR 4 SR=133 S-3--,13 IS Bond B SR Draw the following on the Return/Risk plane below: (b) The stock S, the stock B, the T-bill T. (c) The investment opportunity set of the two risky assets. (d) The optimal risky portfolio P* and the best feasible capital allocation line (CAL). 15- 14- 13 12 11 10- 9- 8- 7- ttrre 4 - 3 2- 1 0 0 1 2 3 4 5 6 7 8 9 10 11 121314151617181920 21 2223 24 25 2627 28 29 30 Risk ReturnStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Navigating The Investment Minefield A Practical Guide To Avoiding Mistakes Biases And Traps

Authors: H. Kent Baker , Vesa Puttonen

1st Edition

1787690563,1787690539