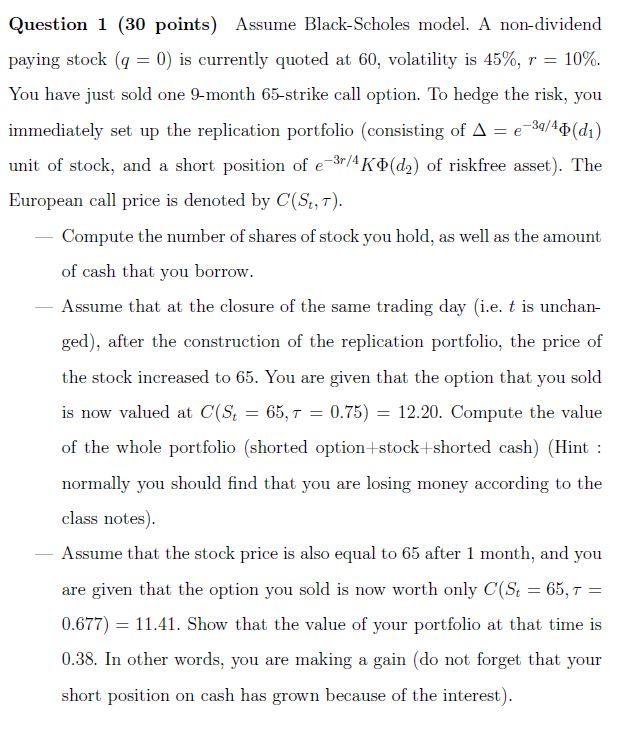

= =e Question 1 (30 points) Assume Black-Scholes model. A non-dividend paying stock (q = 0) is currently quoted at 60, volatility is 45%, r = 10%. You have just sold one 9-month 65-strike call option. To hedge the risk, you immediately set up the replication portfolio (consisting of A = e-3/4" (di) unit of stock, and a short position of e-3r/4K (d)) of riskfree asset). The European call price is denoted by C(S4,7). Compute the number of shares of stock you hold, as well as the amount of cash that you borrow. Assume that at the closure of the same trading day (i.e. t is unchan- ged), after the construction of the replication portfolio, the price of the stock increased to 65. You are given that the option that you sold is now valued at C(St 65,7 0.75) = 12.20. Compute the value of the whole portfolio (shorted option+stock+shorted cash) (Hint: normally you should find that you are losing money according to the class notes). Assume that the stock price is also equal to 65 after 1 month, and you are given that the option you sold is now worth only C(Se = 65,7 = 0.677) = 11.41. Show that the value of your portfolio at that time is 0.38. In other words, you are making a gain (do not forget that your short position on cash has grown because of the interest). = = = = =e Question 1 (30 points) Assume Black-Scholes model. A non-dividend paying stock (q = 0) is currently quoted at 60, volatility is 45%, r = 10%. You have just sold one 9-month 65-strike call option. To hedge the risk, you immediately set up the replication portfolio (consisting of A = e-3/4" (di) unit of stock, and a short position of e-3r/4K (d)) of riskfree asset). The European call price is denoted by C(S4,7). Compute the number of shares of stock you hold, as well as the amount of cash that you borrow. Assume that at the closure of the same trading day (i.e. t is unchan- ged), after the construction of the replication portfolio, the price of the stock increased to 65. You are given that the option that you sold is now valued at C(St 65,7 0.75) = 12.20. Compute the value of the whole portfolio (shorted option+stock+shorted cash) (Hint: normally you should find that you are losing money according to the class notes). Assume that the stock price is also equal to 65 after 1 month, and you are given that the option you sold is now worth only C(Se = 65,7 = 0.677) = 11.41. Show that the value of your portfolio at that time is 0.38. In other words, you are making a gain (do not forget that your short position on cash has grown because of the interest). = = =