Answered step by step

Verified Expert Solution

Question

1 Approved Answer

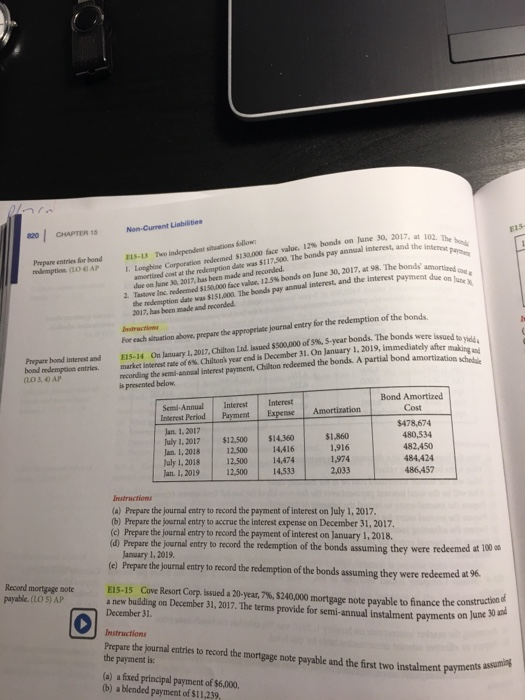

E15-13 a Non-Current Liabilities 820 CHAPTER 1 Prepare entries for bond 115-13 Two independent situations redemption LO 4 AP S130000 face value, 12% bonds on

E15-13

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Managerial Accounting Ba 213 At Central Oregon Community College

Authors: Albrecht

1st Edition

1111523622, 978-1111523626