Answered step by step

Verified Expert Solution

Question

1 Approved Answer

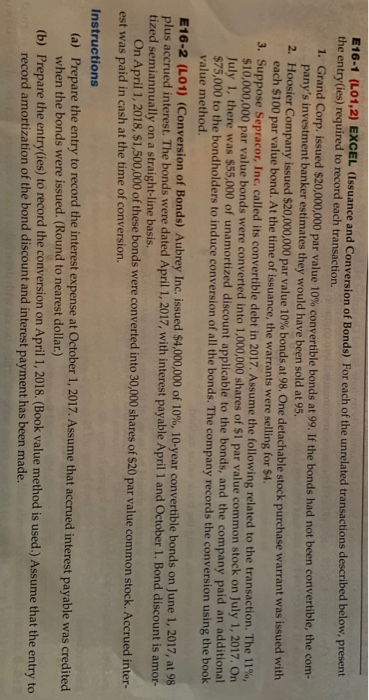

E16-1(1,2,3) & E16-2 (a,b) E16-1 (L01,2) EXCEL (Issuance and Conversion of Bonds) For each of the unrelated transactions described below, present the entry(ies) required to

E16-1(1,2,3) & E16-2 (a,b)

E16-1(1,2,3) & E16-2 (a,b)Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Innovation Audit Workbook

Authors: Langdon Morris

1st Edition

B08HBBKKPJ, 979-8682091614