Answered step by step

Verified Expert Solution

Question

1 Approved Answer

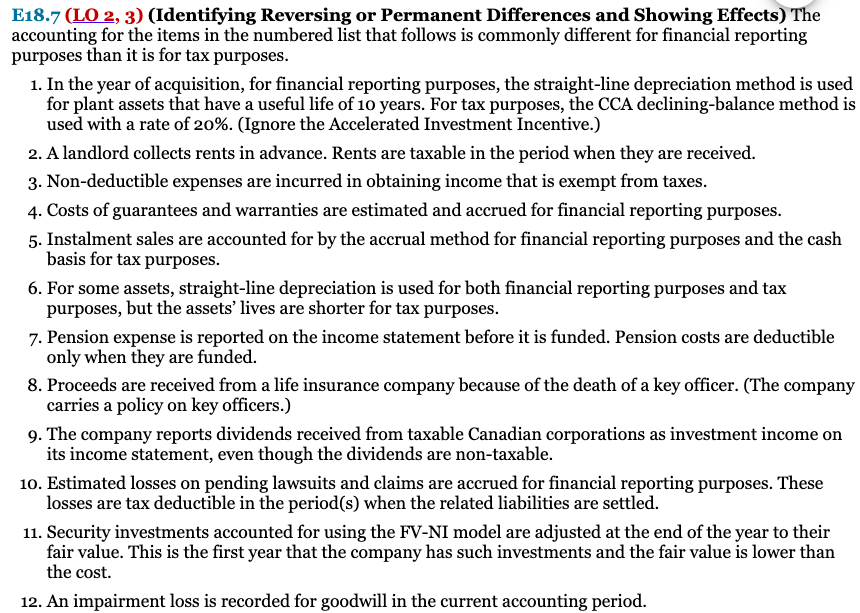

E18.7 ( (LO2,3) (Identifying Reversing or Permanent Differences and Showing Effects) The accounting for the items in the numbered list that follows is commonly different

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

ISE Fundamental Managerial Accounting Concepts

Authors: Thomas P. Edmonds, Christopher Edmonds, Mark A. Edmonds, Philip R. Olds

10th Edition

1265045925, 9781265045920