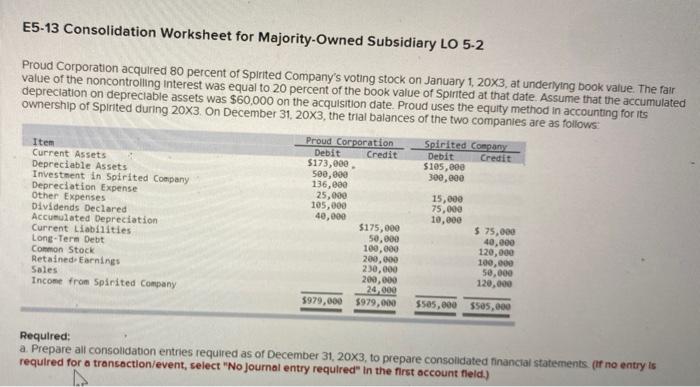

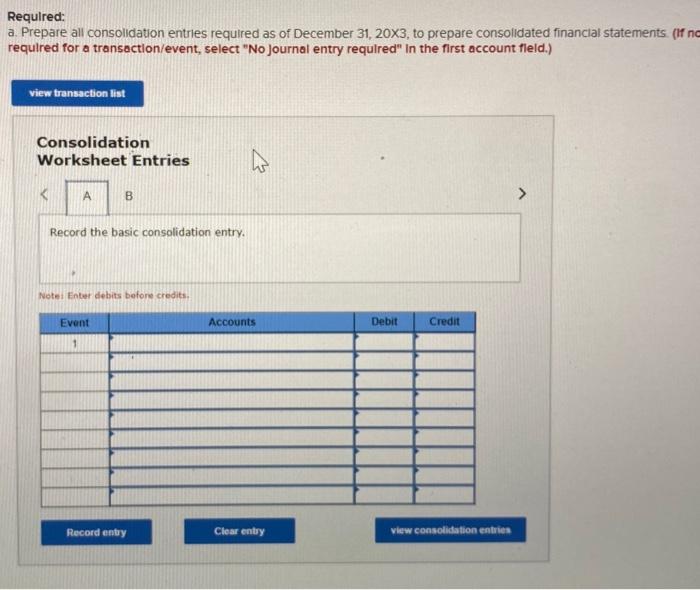

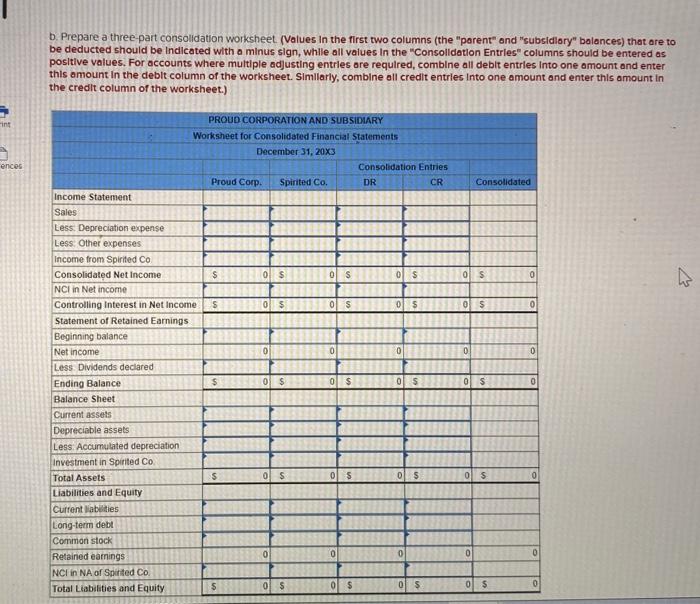

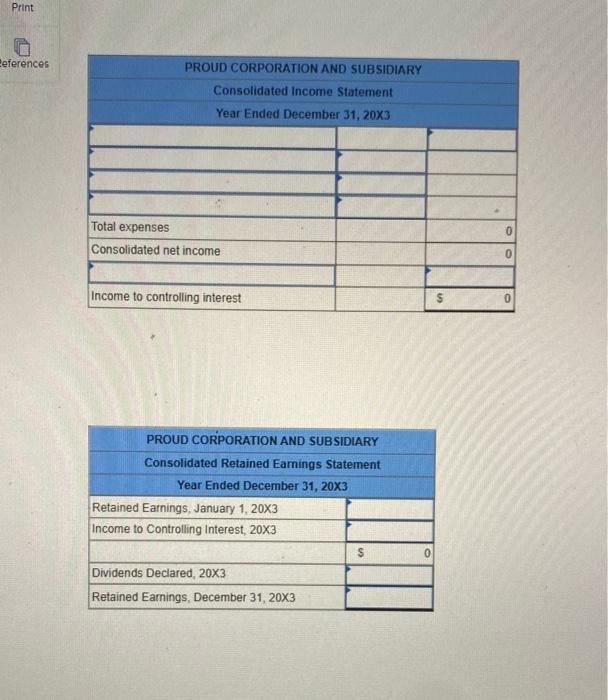

E5-13 Consolidation Worksheet for Majority-Owned Subsidiary LO 5-2 Proud Corporation acquired 80 percent of Spirited Company's voting stock on January 1, 2003, at underlying book value. The fair value of the noncontrolling Interest was equal to 20 percent of the book value of Spirited at that date. Assume that the accumulated depreciation on depreciable assets was $60,000 on the acquisition date Proud uses the equity method in accounting for its ownership of Spirited during 20X3. On December 31, 20X3, the trial balances of the two companies are as follows: Proud Corporation Spirited Company Item Debit Credit Debit Credit Current Assets $173,000 $105,000 Depreciable Assets 500,000 300,000 Investment in Spirited Company 136,000 Depreciation Expense 25,000 15,000 Other Expenses 105,000 75,000 Dividends Declared 40,000 10,000 Accumulated Depreciation $175,000 $ 75,000 Current Liabilities 50,000 40.000 Long-Term Debt 100.000 120,000 Common Stock 200,000 100,000 Retained Earnings 230,000 50,000 Sales 200,000 120,000 Income from Spirited Company 24,000 5979,000 $979,00 $505,000 $505,000 Required: a Prepare all consolidation entries required as of December 31, 20X3, to prepare consolidated financial statements. (If no entry is required for a transaction/event, select "No Journal entry required in the first account field) Required: a Prepare all consolidation entries required as of December 31, 20X3, to prepare consolidated financial statements. (If no required for a transaction/event, select "No Journal entry required" In the first account fleld.) view transaction list Consolidation Worksheet Entries A B Record the basic consolidation entry. Note Enter debits before credits Event Accounts Debit Credit 1 Record entry Clear entry view consolidation entries b. Prepare a three part consolidation worksheet. (Values in the first two columns (the "parent" and "subsidiary" balances) that are to be deducted should be Indicated with a minus sign, while all values in the "Consolidation Entries" columns should be entered as positive values. For accounts where multiple adjusting entries are required, combine all debit entries into one amount and enter this amount in the debit column of the worksheet. Similarly, combine all credit entries into one amount and enter this amount in the credit column of the worksheet.) int ences Consolidated 0 s 0 OS 0 0 0 PROUD CORPORATION AND SUBSIDIARY Worksheet for Consolidated Financial Statements December 31, 20X3 Consolidation Entries Proud Corp. Spirited Co. DR CR Income Statement Sales Less. Depreciation expense Less Other expenses Income from Spirited Co Consolidated Net Income $ 0 $ os 0 $ NCI in Net income Controlling Interest in Net Income S 0 $ ols 0 $ Statement of Retained Earnings Beginning balance Net income 0 0 0 Less Dividends declared Ending Balance $ 0 $ 0 $ os Balance Sheet Current assets Depreciable assets Less Accumulated depreciation Investment in Spirited Co. Total Assets $ os ols 0 $ Liabilities and Equity Current liabilities Long-term debt Common stock Retained earnings 0 0 0 NCI in NA of Spirited Co. Total Liabilities and Equity $ 0 $ 0 $ 0 $ 0 S 0 05 0 0 0 $ 0 Print eferences PROUD CORPORATION AND SUBSIDIARY Consolidated Income Statement Year Ended December 31, 20X3 0 Total expenses Consolidated net income 0 Income to controlling interest s 0 PROUD CORPORATION AND SUBSIDIARY Consolidated Retained Earnings Statement Year Ended December 31, 20X3 Retained Earnings, January 1, 20X3 Income to Controlling Interest, 20X3 Dividends Declared, 20X3 Retained Earnings, December 31, 20X3 C Prepare a consolidated balance sheet, income statement and retained earnings statement for 20X3. (Amounts to be deducted should be indicated with a minus sign.) PROUD CORPORATION AND SUBSIDIARY Consolidated Balance Sheet December 31, 20X3 Assets 0 $ 0 Total Assets Liabilities Stockholders' Equity: Controlling interest Total Controlling Interest 0 0 Total Stockholder's equity Total Liabilities and Stockholders' Equity $ 0