Answered step by step

Verified Expert Solution

Question

1 Approved Answer

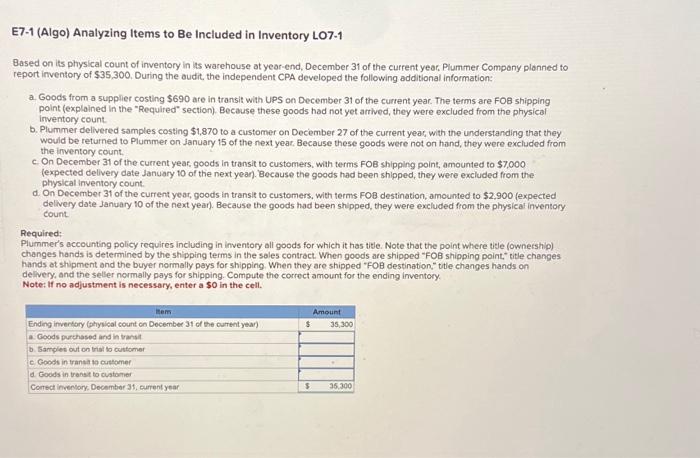

E7-1 (Algo) Analyzing Items to Be Included in Inventory LO7-1 Based on its physical count of inventory in its warehouse at year-end, December 31 of

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Auditing Cases An Interactive Learning Approach

Authors: Mark S. Beasley, Frank A. Buckless, Steven M. Glover, Douglas F. Prawitt

6th edition

133852105, 978-0133852103