Answered step by step

Verified Expert Solution

Question

1 Approved Answer

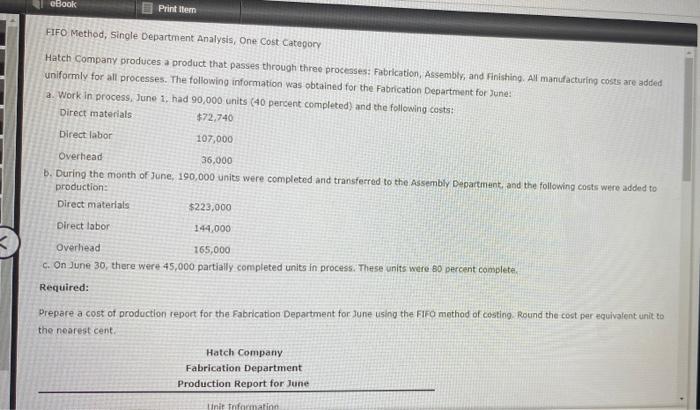

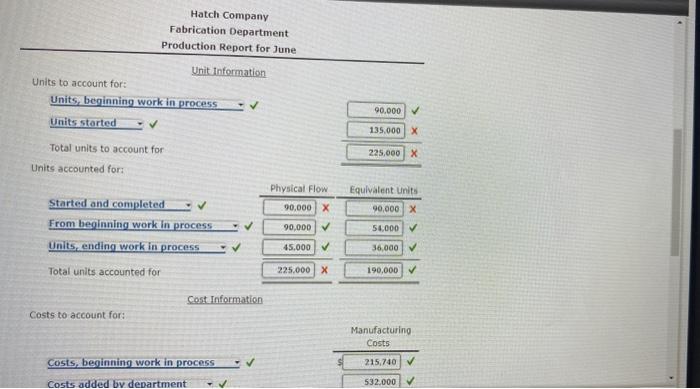

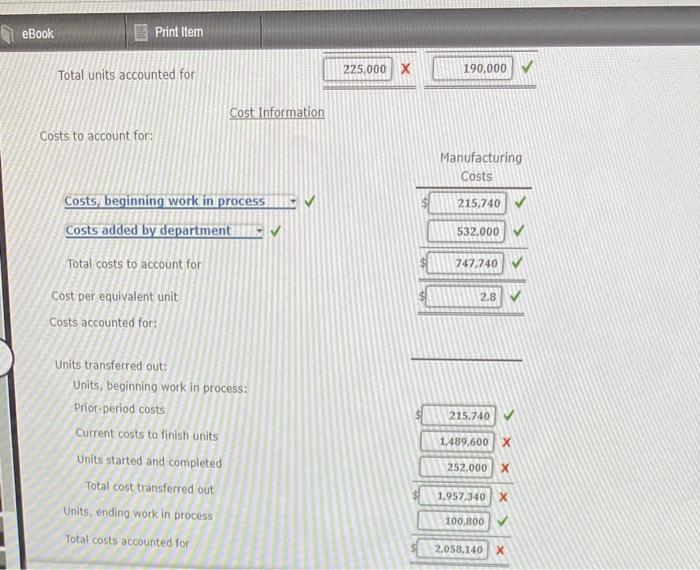

eBook Print item FIFO Method, Single Department Analysis, One Cost Category Hatch Company produces a product that passes through three processes: Fabrication, Assembly, and Finishing.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Auditing and Assurance Services

Authors: Timothy Louwers, Robert Ramsay, David Sinason, Jerry Straws

6th edition

978-1259197109, 77632281, 77862341, 1259197107, 9780077632281, 978-0077862343