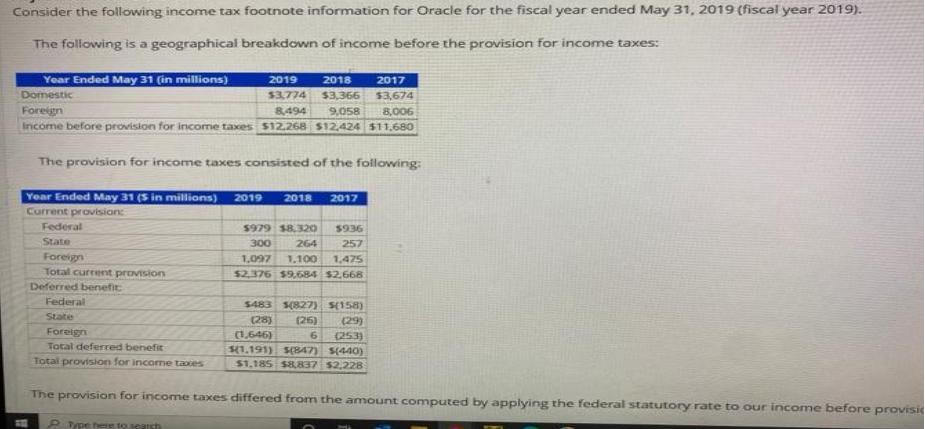

Consider the following income tax footnote information for Oracle for the fiscal year ended May 31,...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

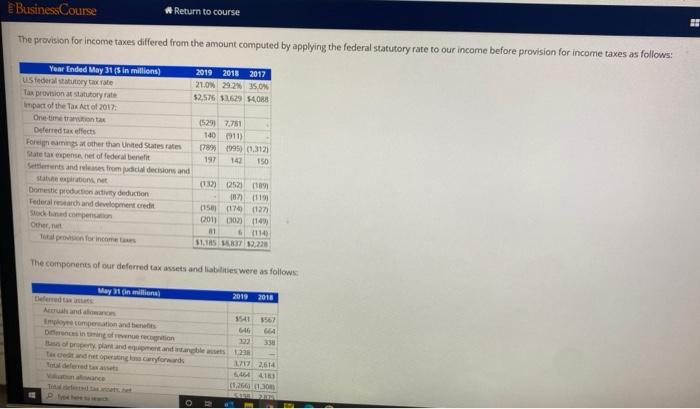

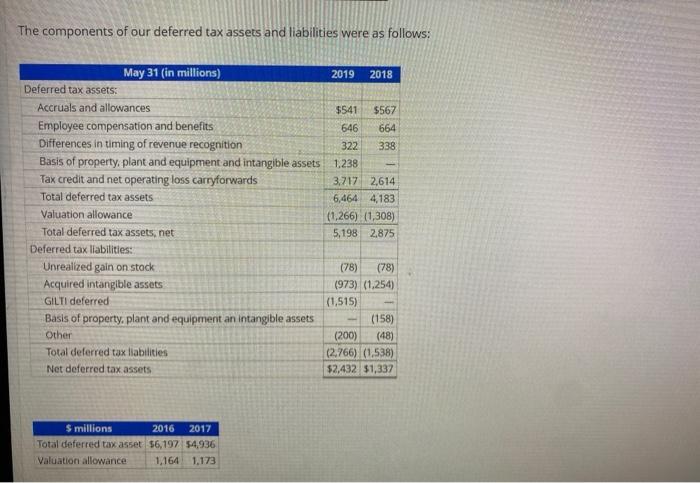

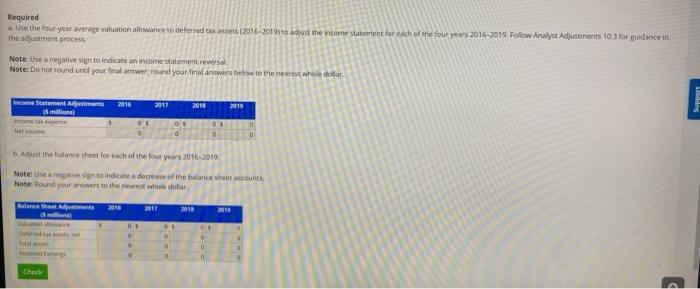

Consider the following income tax footnote information for Oracle for the fiscal year ended May 31, 2019 (fiscal year 2019). The following is a geographical breakdown of income before the provision for income taxes: Year Ended May 31 (in millions) Domestic 2019 2018 $3,774 $3,366 8,494 9,058 Foreign Income before provision for income taxes $12.268 $12,424 $11,680 The provision for income taxes consisted of the following: Year Ended May 31 (5 in millions) 2019 2018 2017 Current provision: Federal State Foreign Total current provision Deferred benefit Federal State Foreign Total deferred benefit Total provision for income taxes $979 $8,320 300 264 1,097 1.100 1,475 $2,376 $9,684 $2,668 $936 257 2017 $3,674 8,006 $483 1(827) $(158) (28) (26) (29) (253) 6 (1,646) (1.191) 5(847) $(440) $1,185 $8,837 $2,228 The provision for income taxes differed from the amount computed by applying the federal statutory rate to our income before provisi P... Type here to search Business Course Return to course The provision for income taxes differed from the amount computed by applying the federal statutory rate to our income before provision for income taxes as follows: Year Ended May 31 (5 in millions) 2019 2018 2017 21.0% 29.2% 35.0% $2,576 $3629 $4,088 US federal statutory tax rate Tax provision at statutory rate impact of the Tax Act of 2017: One-time transition tax Deferred tax effects Foreign eamings at other than United States rates State tax expense, net of federal benefit Settlements and releases from judicial decisions and statute expirations, net Domestic production activity deduction Tederal research and development credit Stock-based compensation Deferred tax assats Other, net Total provision for income taxes The components of our deferred tax assets and liabilities were as follows: May 31 On millions) (529) 7,781 140 (911) (789) (995) (1.312) 197 142 150 (132) (252) (189) (87) (119) (158) (174) (127) (2011 (302) (14) 81 6 (114) $1,185 16837 $2,228 O Accruals and allowanon Employee compensation and benefits Differences in taming of revenue recognition Bass of property, plant and equipment and intangble assets 1.238 Tax credit and net operating loss carryforwards 2019 2018 B $541 3567 646 644 322 338 3717 2,614 6464 4183 (1.266) (1.30 The components of our deferred tax assets and liabilities were as follows: Deferred tax assets: May 31 (in millions) Accruals and allowances Employee compensation and benefits Differences in timing of revenue recognition Basis of property, plant and equipment and intangible assets Tax credit and net operating loss carryforwards Total deferred tax assets Valuation allowance Total deferred tax assets, net Deferred tax liabilities: Unrealized gain on stock Acquired intangible assets GILTI deferred Basis of property, plant and equipment an intangible assets Other Total deferred tax liabilities Net deferred tax assets $ millions Total deferred tax asset Valuation allowance 2017 2016 $6,197 $4,936 1,164 1,173 2019 2018 $541 646 322 1,238 3,717 2,614 6,464 4,183 $567 664 338 (1,266) (1,308) 5,198 2,875 (1,515) (78) (78) (973) (1,254) (158) (200) (48) (2,766) (1,538) $2,432 $1,337 Required a. Use the four-year average valuation allowance to deferred tax assets (2016-2019 to adjust the income statement for each of the four years 2016-2019. Follow Analyst Adjustments 10.3 for guidance in the adjustment process. Note Use a negative sign to indicate an income statement reversal Note: Do not round until your final answer, round your final answers below to the nearest whole dollar. Income Statement Adjustments millions) income tax exper Netcome 2016 Balance Sheet Adjustments 2016 (3) Deferred fa Check 01 2017 2017 0.5 0 b. Adjust the balance sheet for each of the four years 2016-2019 Note: Use a negative sign to indicate a decrease of the balance sheet accounts. Note: Round your answers to the nearest whole dollar 0 2018 01 0 2018 2019 09 0 0 2019 ww the adjustment process. Note: Use a negative sign to indicate an income statement reversal. Note: Do not round until your final answer; round your final answers below to the nearest whole da Income Statement Adjustments ($ millions) Income tax expense Net income 2016 Balance Sheet Adjustments 2016 ($ millions) Valuation allowance Deferred tax assets, net Total assets Retained Earnings Check Tyne here to search 0 $ 0 0 $ 0 0 0 2017 2017 O b. Adjust the balance sheet for each of the four years 2016-2019. Note: Use a negative sign to indicate a decrease of the balance sheet accounts. Note: Round your answers to the nearest whole dollar. COO 0 $ 0 0$ 0 00 2018 2018 0 $ 0 0 0 $ 0 2019 2019 0 0 0 0 0 0 adjust the in Consider the following income tax footnote information for Oracle for the fiscal year ended May 31, 2019 (fiscal year 2019). The following is a geographical breakdown of income before the provision for income taxes: Year Ended May 31 (in millions) Domestic 2019 2018 $3,774 $3,366 8,494 9,058 Foreign Income before provision for income taxes $12.268 $12,424 $11,680 The provision for income taxes consisted of the following: Year Ended May 31 (5 in millions) 2019 2018 2017 Current provision: Federal State Foreign Total current provision Deferred benefit Federal State Foreign Total deferred benefit Total provision for income taxes $979 $8,320 300 264 1,097 1.100 1,475 $2,376 $9,684 $2,668 $936 257 2017 $3,674 8,006 $483 1(827) $(158) (28) (26) (29) (253) 6 (1,646) (1.191) 5(847) $(440) $1,185 $8,837 $2,228 The provision for income taxes differed from the amount computed by applying the federal statutory rate to our income before provisi P... Type here to search Business Course Return to course The provision for income taxes differed from the amount computed by applying the federal statutory rate to our income before provision for income taxes as follows: Year Ended May 31 (5 in millions) 2019 2018 2017 21.0% 29.2% 35.0% $2,576 $3629 $4,088 US federal statutory tax rate Tax provision at statutory rate impact of the Tax Act of 2017: One-time transition tax Deferred tax effects Foreign eamings at other than United States rates State tax expense, net of federal benefit Settlements and releases from judicial decisions and statute expirations, net Domestic production activity deduction Tederal research and development credit Stock-based compensation Deferred tax assats Other, net Total provision for income taxes The components of our deferred tax assets and liabilities were as follows: May 31 On millions) (529) 7,781 140 (911) (789) (995) (1.312) 197 142 150 (132) (252) (189) (87) (119) (158) (174) (127) (2011 (302) (14) 81 6 (114) $1,185 16837 $2,228 O Accruals and allowanon Employee compensation and benefits Differences in taming of revenue recognition Bass of property, plant and equipment and intangble assets 1.238 Tax credit and net operating loss carryforwards 2019 2018 B $541 3567 646 644 322 338 3717 2,614 6464 4183 (1.266) (1.30 The components of our deferred tax assets and liabilities were as follows: Deferred tax assets: May 31 (in millions) Accruals and allowances Employee compensation and benefits Differences in timing of revenue recognition Basis of property, plant and equipment and intangible assets Tax credit and net operating loss carryforwards Total deferred tax assets Valuation allowance Total deferred tax assets, net Deferred tax liabilities: Unrealized gain on stock Acquired intangible assets GILTI deferred Basis of property, plant and equipment an intangible assets Other Total deferred tax liabilities Net deferred tax assets $ millions Total deferred tax asset Valuation allowance 2017 2016 $6,197 $4,936 1,164 1,173 2019 2018 $541 646 322 1,238 3,717 2,614 6,464 4,183 $567 664 338 (1,266) (1,308) 5,198 2,875 (1,515) (78) (78) (973) (1,254) (158) (200) (48) (2,766) (1,538) $2,432 $1,337 Required a. Use the four-year average valuation allowance to deferred tax assets (2016-2019 to adjust the income statement for each of the four years 2016-2019. Follow Analyst Adjustments 10.3 for guidance in the adjustment process. Note Use a negative sign to indicate an income statement reversal Note: Do not round until your final answer, round your final answers below to the nearest whole dollar. Income Statement Adjustments millions) income tax exper Netcome 2016 Balance Sheet Adjustments 2016 (3) Deferred fa Check 01 2017 2017 0.5 0 b. Adjust the balance sheet for each of the four years 2016-2019 Note: Use a negative sign to indicate a decrease of the balance sheet accounts. Note: Round your answers to the nearest whole dollar 0 2018 01 0 2018 2019 09 0 0 2019 ww the adjustment process. Note: Use a negative sign to indicate an income statement reversal. Note: Do not round until your final answer; round your final answers below to the nearest whole da Income Statement Adjustments ($ millions) Income tax expense Net income 2016 Balance Sheet Adjustments 2016 ($ millions) Valuation allowance Deferred tax assets, net Total assets Retained Earnings Check Tyne here to search 0 $ 0 0 $ 0 0 0 2017 2017 O b. Adjust the balance sheet for each of the four years 2016-2019. Note: Use a negative sign to indicate a decrease of the balance sheet accounts. Note: Round your answers to the nearest whole dollar. COO 0 $ 0 0$ 0 00 2018 2018 0 $ 0 0 0 $ 0 2019 2019 0 0 0 0 0 0 adjust the in

Expert Answer:

Answer rating: 100% (QA)

1 Deferred income statement In order to obtain the deferred income schedule the following steps are ... View the full answer

Related Book For

Financial Markets and Institutions

ISBN: 978-0077861667

6th edition

Authors: Anthony Saunders , Marcia Cornett

Posted Date:

Students also viewed these accounting questions

-

Consider the following income statement for WatchoverU Savings Inc. (in millions): a. What is WatchoverUs expected net interest income at year-end? b. What will be the net interest income at year-...

-

Consider the following income statement and non-cash working capital account information of Yahk Ltd. (Yahk). Assume Yahk uses IFRS. Required: a. Calculate cash from operations for Yahk using the...

-

Consider the following income statement: Sales .......................... $713,500 Costs .......................... 497,300 Depreciation ................... 87,400 EBIT...

-

In a given week, 12 babies are born in hospital. Assume that this sample came from an underlying normal population. The length of each baby is routinely measured and is listed below (in cm): 49, 50,...

-

Alpine Ski Shops Prepaid Rent balance is $4,500 on June 1. This prepaid rent represents six months rent. Journalize and post the adjusting entry on June 30 to record one months rent. Compute the...

-

The Stockholders' Equity section of the December 31, 2012, balance sheet of Carter Company appeared as follows: Preferred stock, $50 par value, 10,000 shares authorized, ? shares issued............$...

-

Explain the concept of limited liability.

-

Poole Company began the 2013 accounting period with $36,000 cash, $80,000 inventory, $70,000 common stock, and $46,000 retained earnings. During the 2013 accounting period, Poole experienced the...

-

One of the more closely watched ratios by investors is the price-earnings (P/E) ratio. By dividing price per share by earnings per share. analysts get insight into the value the market attaches to a...

-

The evening manager of a restaurant was very concerned about the length of time some customers were waiting in line to be seated. She also had some concern about the seating times that is, the length...

-

What It Means to Invest in Stocks? Common stock is considered to be one of the most popular investment vehicles for long-term wealth building. Investors earn income from common stock in the form of...

-

Based on the attached template, draft the beginning of a contract, including the title , an introductory statement , recitals , and a transitional clause. Scenario: Professional staff outsourcing has...

-

Given the Hick's Law equation of RT = 260 + 120[log2N], what reaction time would be expected for 16 choices. Provide you answer in milliseconds and do not include units in your answer. Your Answer:

-

Consider a product, children's bikes, sold to customers in two cities, A and B. After some customer research, the bike maker has determined the following: Total Potential Customers in City A = 60...

-

Central to the economics of Smith, Ricardo and Marx is the labor theory of value. Did they all agree or did later writers criticize earlier writers? Also what, if any, are the implications of the...

-

Assume the bonus contract pays the manager 50% of the firm's income above 40. If the firm revenue is $50 with p = 0.6 and $70 with p = 0.4 under the manager's chosen level of effort, calculate the...

-

A firm has issued preferred stock at its $ 1 4 5 per share par value. The stock will pay a $ 1 5 annual dividend. The cost of issuing and selling the stock was $ 4 per share. The cost of the...

-

Consider the circuit of Fig. 7.97. Find v0 (t) if i(0) = 2 A and v(t) = 0. 1 3 ett)

-

What is the difference between an open-end mutual fund and a closed-end fund? What is the difference between an open-end mutual fund and a unit investment trust?

-

What are the primary responsibilities of the Federal Reserve Board?

-

Describe the structure of the Board of Governors of the Federal Reserve System.

-

A slurry of pure \(\mathrm{NaCl}\) crystals, \(\mathrm{NaCl}\) in solution, \(\mathrm{NaOH}\) in solution, and water is sent to a system of thickener(s) at a rate of \(100.0 \mathrm{~kg} /...

-

Repeat Example 14-2 except for a three-stage countercurrent system and unknown underflow product concentration. Example 14-2 We wish to treat 1000.0 kg/h (wet basis) of insoluble meal (D) that...

-

This problem looks at the trade-offs between purity measured by \(\mathrm{y}_{\mathrm{I}, \text { out }} / \mathrm{y}_{\text {sugar, out }}\) and sugar recovery in the liquid,...

Study smarter with the SolutionInn App