Answered step by step

Verified Expert Solution

Question

1 Approved Answer

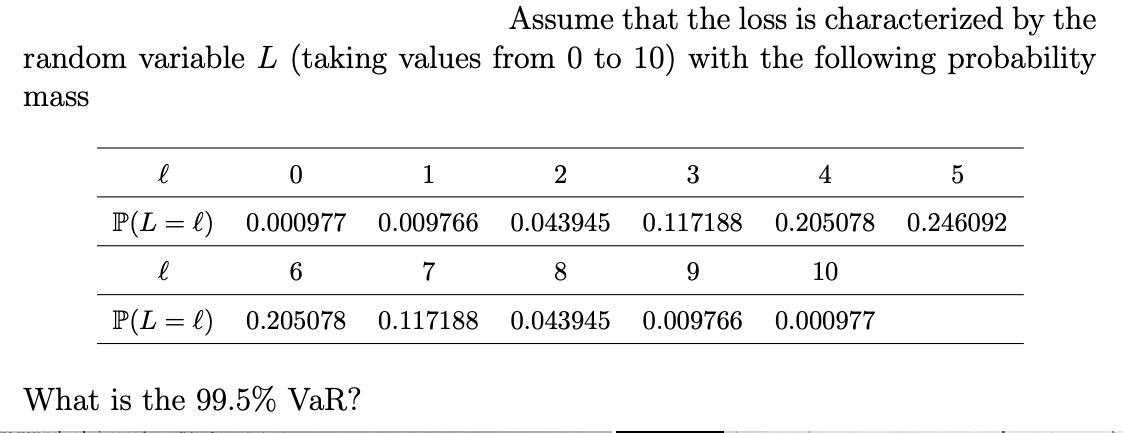

Assume that the loss is characterized by the random variable L (taking values from 0 to 10) with the following probability mass 0 P(L

Assume that the loss is characterized by the random variable L (taking values from 0 to 10) with the following probability mass 0 P(L = l) 0.000977 6 P(L = l) 0.205078 What is the 99.5% VaR? 1 0.009766 7 0.117188 2 3 0.043945 0.117188 8 9 0.043945 0.009766 4 5 0.205078 0.246092 10 0.000977

Step by Step Solution

★★★★★

3.44 Rating (151 Votes )

There are 3 Steps involved in it

Step: 1

To calculate the 995 Value at Risk VaR we need to determine the loss va...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Fundamentals of Financial Accounting

Authors: Fred Phillips, Robert Libby, Patricia Libby

4th edition

978-0073369709, 73369705, 78025370, 978-0077444846, 77444841, 978-0078025372