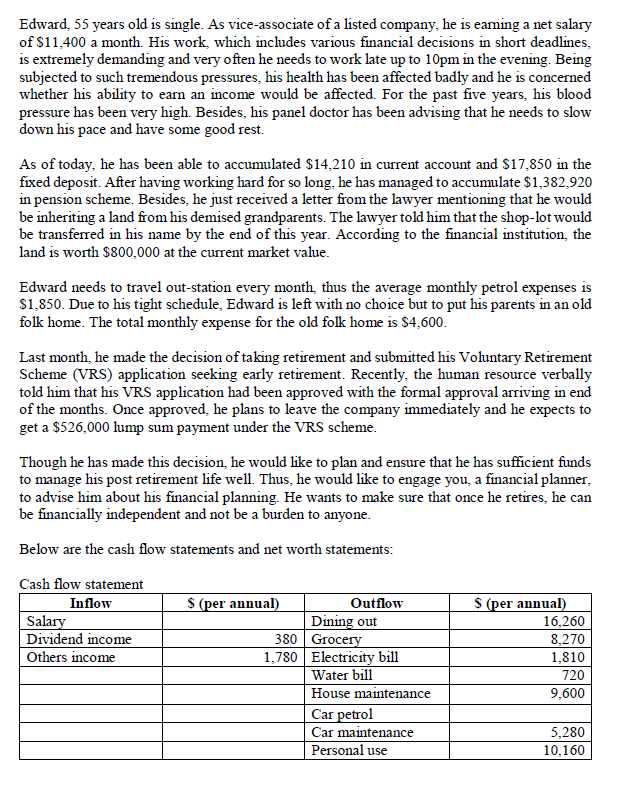

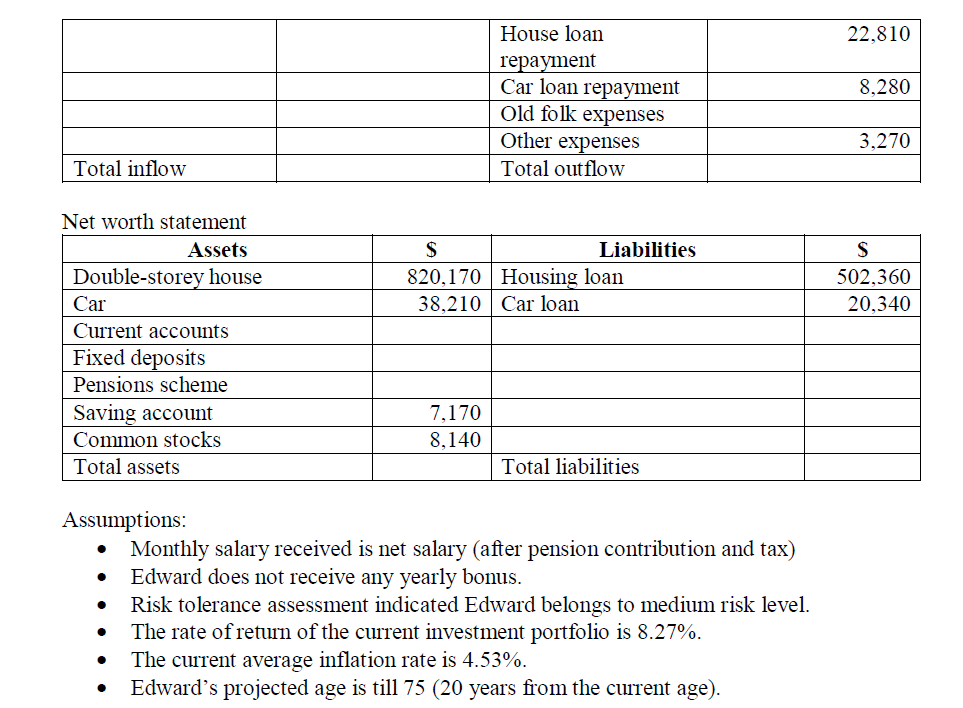

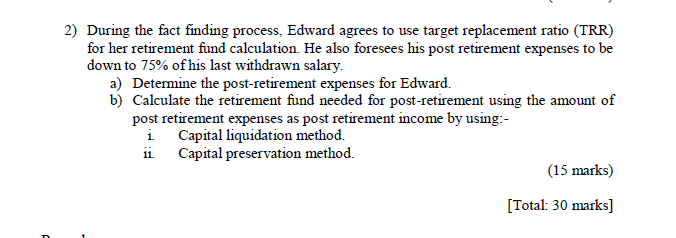

Edward, 55 years old is single. As vice-associate of a listed company, he is earning a net salary of $11,400 a month. His work, which includes various financial decisions in short deadlines, is extremely demanding and very often he needs to work late up to 10pm in the evening. Being subjected to such tremendous pressures, his health has been affected badly and he is concerned whether his ability to earn an income would be affected. For the past five years, his blood pressure has been very high. Besides, his panel doctor has been advising that he needs to slow down his pace and have some good rest. As of today, he has been able to accumulated $14,210 in current account and $17.850 in the fixed deposit. After having working hard for so long, he has managed to accumulate $1,382,920 in pension scheme. Besides, he just received a letter from the lawyer mentioning that he would be inheriting a land from his demised grandparents. The lawyer told him that the shop-lot would be transferred in his name by the end of this year. According to the financial institution, the land is worth $800,000 at the current market value. Edward needs to travel out-station every month, thus the average monthly petrol expenses is $1,850. Due to his tight schedule, Edward is left with no choice but to put his parents in an old folk home. The total monthly expense for the old folk home is $4,600. Last month, he made the decision of taking retirement and submitted his Voluntary Retirement Scheme (VRS) application seeking early retirement. Recently, the human resource verbally told him that his VRS application had been approved with the formal approval arriving in end of the months. Once approved, he plans to leave the company immediately and he expects to get a $526,000 lump sum payment under the VRS scheme. Though he has made this decision, he would like to plan and ensure that he has sufficient funds to manage his post retirement life well. Thus, he would like to engage you, a financial planner, to advise him about his financial planning. He wants to make sure that once he retires, he can be financially independent and not be a burden to anyone. Below are the cash flow statements and net worth statements: Cash flow statement Inflow S (per annual) Outflow S (per annual) Salary Dining out 16,260 Dividend income 380 Grocery 8,270 Others income 1,780 Electricity bill 1,810 Water bill 720 House maintenance 9,600 Car petrol Car maintenance 5,280 Personal use 10,160 22.810 8,280 House loan repayment Car loan repayment Old folk expenses Other expenses Total outflow 3,270 Total inflow S Liabilities 820,170 Housing loan 38,210 Car loan S 502,360 20,340 Net worth statement Assets Double-storey house Car Current accounts Fixed deposits Pensions scheme Saving account Common stocks Total assets 7,170 8,140 Total liabilities Assumptions: Monthly salary received is net salary (after pension contribution and tax) Edward does not receive any yearly bonus. Risk tolerance assessment indicated Edward belongs to medium risk level. The rate of return of the current investment portfolio is 8.27%. The current average inflation rate is 4.53%. Edward's projected age is till 75 (20 years from the current age). . . 2) During the fact finding process, Edward agrees to use target replacement ratio (TRR) for her retirement fund calculation. He also foresees his post retirement expenses to be down to 75% of his last withdrawn salary. a) Determine the post-retirement expenses for Edward. b) Calculate the retirement fund needed for post-retirement using the amount of post retirement expenses as post retirement income by using: - i Capital liquidation method. ii. Capital preservation method. (15 marks) [Total: 30 marks] Edward, 55 years old is single. As vice-associate of a listed company, he is earning a net salary of $11,400 a month. His work, which includes various financial decisions in short deadlines, is extremely demanding and very often he needs to work late up to 10pm in the evening. Being subjected to such tremendous pressures, his health has been affected badly and he is concerned whether his ability to earn an income would be affected. For the past five years, his blood pressure has been very high. Besides, his panel doctor has been advising that he needs to slow down his pace and have some good rest. As of today, he has been able to accumulated $14,210 in current account and $17.850 in the fixed deposit. After having working hard for so long, he has managed to accumulate $1,382,920 in pension scheme. Besides, he just received a letter from the lawyer mentioning that he would be inheriting a land from his demised grandparents. The lawyer told him that the shop-lot would be transferred in his name by the end of this year. According to the financial institution, the land is worth $800,000 at the current market value. Edward needs to travel out-station every month, thus the average monthly petrol expenses is $1,850. Due to his tight schedule, Edward is left with no choice but to put his parents in an old folk home. The total monthly expense for the old folk home is $4,600. Last month, he made the decision of taking retirement and submitted his Voluntary Retirement Scheme (VRS) application seeking early retirement. Recently, the human resource verbally told him that his VRS application had been approved with the formal approval arriving in end of the months. Once approved, he plans to leave the company immediately and he expects to get a $526,000 lump sum payment under the VRS scheme. Though he has made this decision, he would like to plan and ensure that he has sufficient funds to manage his post retirement life well. Thus, he would like to engage you, a financial planner, to advise him about his financial planning. He wants to make sure that once he retires, he can be financially independent and not be a burden to anyone. Below are the cash flow statements and net worth statements: Cash flow statement Inflow S (per annual) Outflow S (per annual) Salary Dining out 16,260 Dividend income 380 Grocery 8,270 Others income 1,780 Electricity bill 1,810 Water bill 720 House maintenance 9,600 Car petrol Car maintenance 5,280 Personal use 10,160 22.810 8,280 House loan repayment Car loan repayment Old folk expenses Other expenses Total outflow 3,270 Total inflow S Liabilities 820,170 Housing loan 38,210 Car loan S 502,360 20,340 Net worth statement Assets Double-storey house Car Current accounts Fixed deposits Pensions scheme Saving account Common stocks Total assets 7,170 8,140 Total liabilities Assumptions: Monthly salary received is net salary (after pension contribution and tax) Edward does not receive any yearly bonus. Risk tolerance assessment indicated Edward belongs to medium risk level. The rate of return of the current investment portfolio is 8.27%. The current average inflation rate is 4.53%. Edward's projected age is till 75 (20 years from the current age). . . 2) During the fact finding process, Edward agrees to use target replacement ratio (TRR) for her retirement fund calculation. He also foresees his post retirement expenses to be down to 75% of his last withdrawn salary. a) Determine the post-retirement expenses for Edward. b) Calculate the retirement fund needed for post-retirement using the amount of post retirement expenses as post retirement income by using: - i Capital liquidation method. ii. Capital preservation method. (15 marks) [Total: 30 marks]