Eloise Moore was elated as she put down the phone. She had been talking with Bob Studz, vice president, data processing at Excelerite Integrated Systems

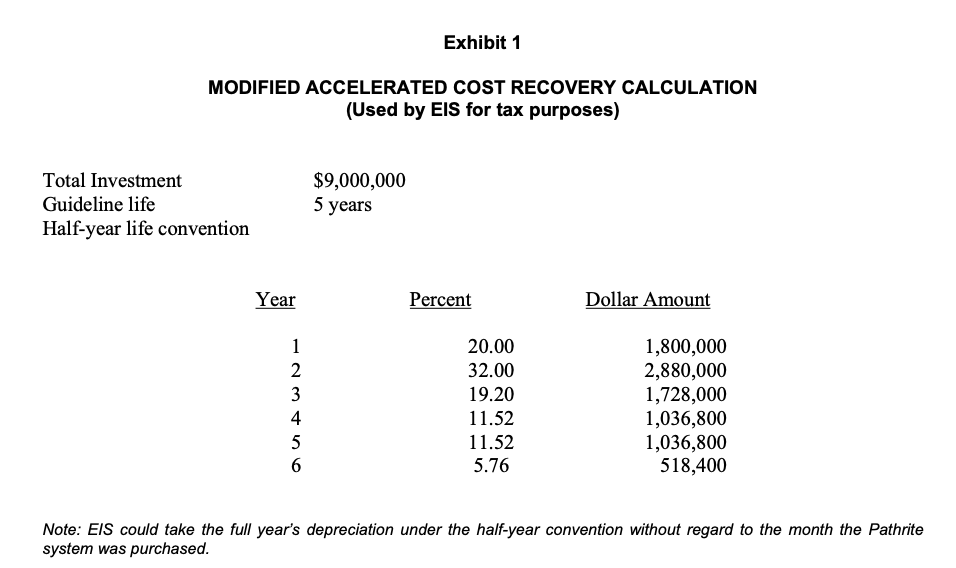

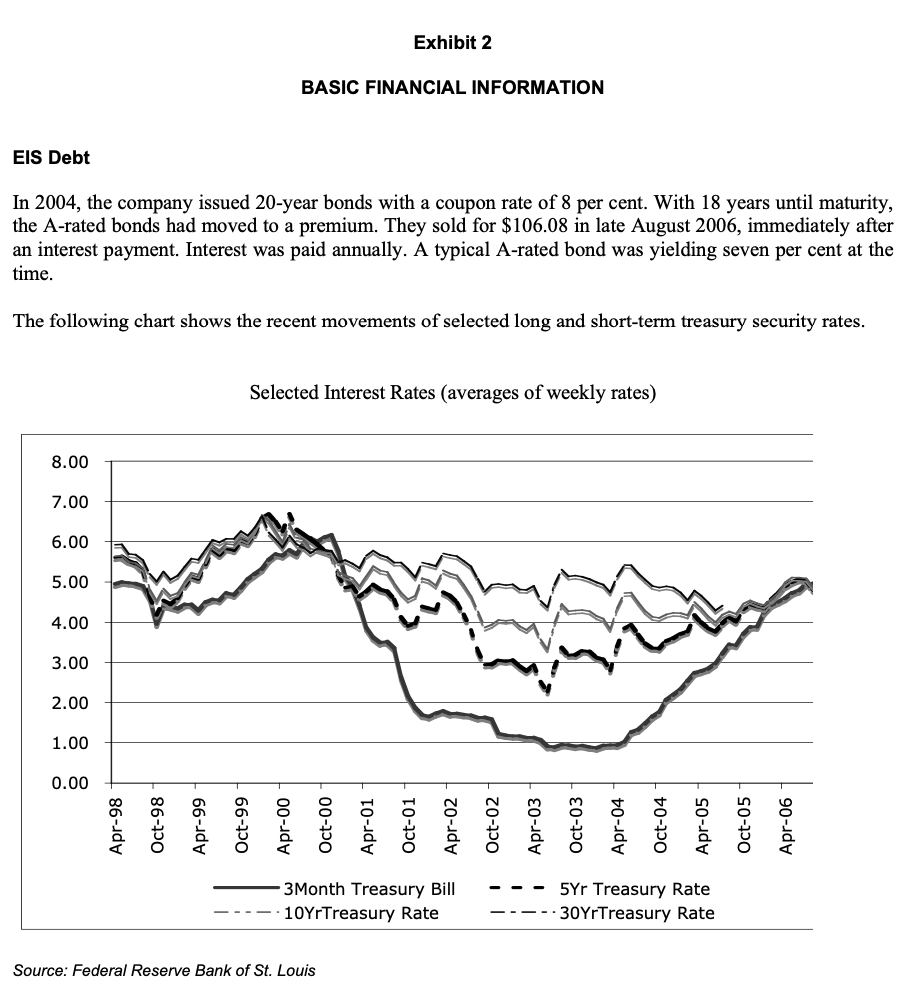

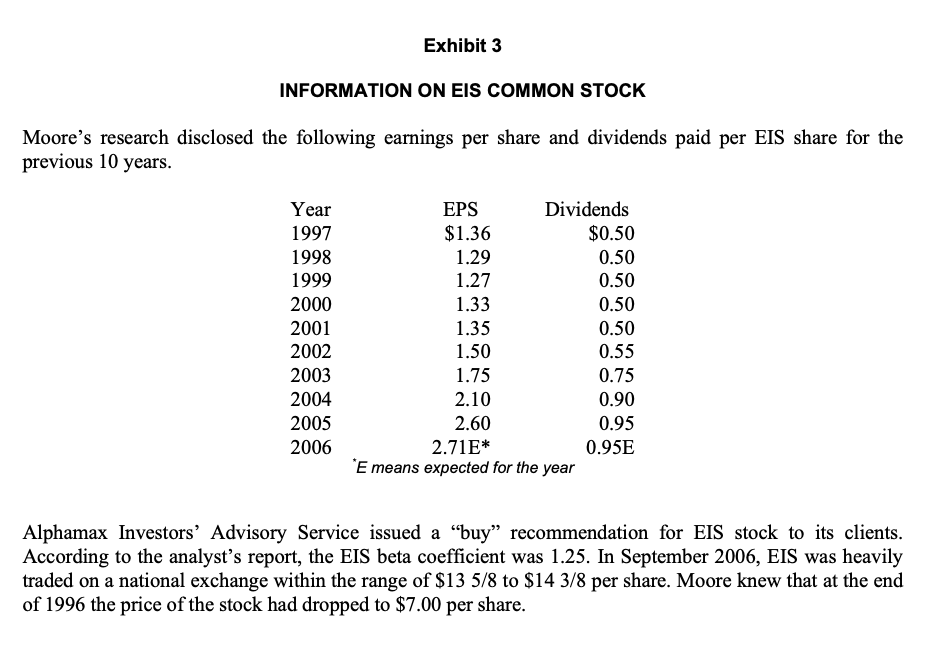

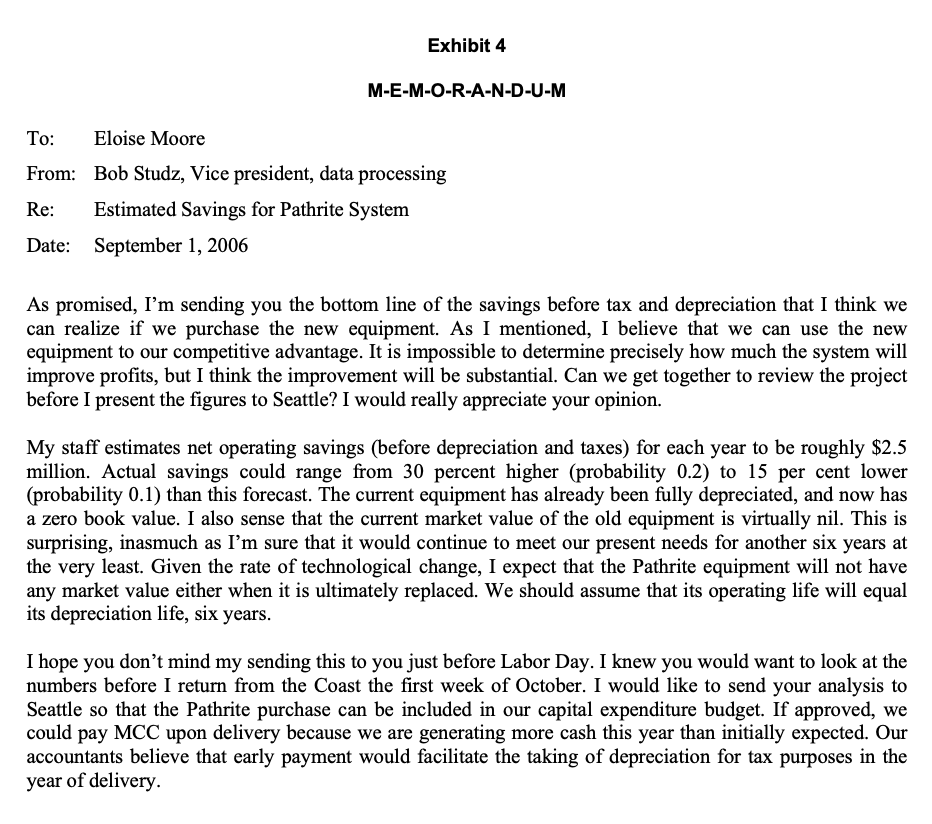

Eloise Moore was elated as she put down the phone. She had been talking with Bob Studz, vice president, data processing at Excelerite Integrated Systems Inc. (EIS), who had just returned from a company- sponsored management development program in late August, 2006. Studz had said: Eloise, we had a terrific session on capital budgeting last week. I can now see the utility of projecting operating savings 'om the Pathrite system as a way of persuading Seattle to provide us with the needed funds. I'm developing tentative savings numbers and will email them to you as soon as I'm finished. Could you take a rough cut at the kind of analysis that will make sense to the Seattle financial mavens? Moore was a sales representative with Monster Computer Corporation (MCC). A 12-year veteran, she was assigned to large accounts, those whose purchases were expected to exceed $2 million. Working from her ofce in Phoenix, Arizona, Moore was assigned customers in the western half of the United States. MCC was the largest provider of hardware and software in the data processing eld and had recently expanded to provide consulting and data processing services. Moore saw a golden opportunity. Seattle was the home ofce for E13 and the source of all EIS corporate capital funds. If she could help Studz sell the system to his top management, she would enhance her standing among the sales staff. Moore sketched out the system that she and Studz had been discussing. It included a supercomputer, data storage and a set of peripherals to allow corporate data to be accessed via the Web and by mobile users in EIS district offices around the country. The total cost for the system was $9 million. Because of the lead time for assembling components, delivery and payment could be in late 2006, so Moore decided to use a January 1, 200'? operating starting date. She anticipated that the expected marginal tax rate for EIS would be 40 per cent (federal and state taxes) and that the modified accelerated cost recovery scheme for depreciation would be used for tax purposes (see Exhibit 1). 7. Sensitivity AnalysisMoor did not know the target capital structure of EIS or the hurdle rate used by Seattle (i.e. the EIS home ofce) in evaluating their capital commitments. Accordingly, she decided to estimate them using publicly available nancial data (see Exhibit 2). She assumed that EIS management sought to maintain a mix of 30 per cent long-term debt and 70 per cent common equity (book value), which was consistent with industry averages. Furthermore, she knew that EIS management would be reluctant to sell shares at the depressed market price of 80 per cent of book value (see Exhibit 3), and that the average return on large company stocks had exceeded the return on risk-free securities by 6.6 per cent over a 18-year period. She estimated that ination would average 2.5 per cent each year for the foreseeable future. A week or so after her conversation with Bob Studz, Moore received a memorandum from him indicating the expected savings from the installation of the equipment (see Exhibit 4). She knew that EIS would expect her analysis to be based on the application of discounted cash ow techniques to determine both a net present value and an internal rate of return. Her next task would be to prepare an analysis for Studz, based on the information available to her. Exhibit 1 MODIFIED ACCELERATED COST RECOVERY CALCULATION (Used by EIS for tax purposes) Total Investment $9,000,000 Guideline life 5 years Half-year life convention Year Percent Dollar Amount 20.00 1,800,000 32.00 2,880,000 19.20 1,728,000 aUAWNE 11.52 1,036,800 11.52 1,036,800 5.76 518,400 Note: EIS could take the full year's depreciation under the half-year convention without regard to the month the Pathrite system was purchased.Exhibit 2 BASIC FINANCIAL INFORMATION EIS Debt In 2004, the company issued 20-year bonds with a coupon rate of 8 per cent. With 18 years until maturity, the A-rated bonds had moved to a premium. They sold for $106.08 in late August 2006, immediately after an interest payment. Interest was paid annually. A typical A-rated bond was yielding seven per cent at the time. The following chart shows the recent movements of selected long and short-term treasury security rates. Selected Interest Rates (averages of weekly rates) 8.00 7.00 6.00 5.00 4.00 3.00 2.00 1.00 0.00 Oct-05 Oct-04 Oct-00 Oct-02 Oct-03 Oct-01 Oct-99 Apr-01 Apr-06 Oct-98 Apr-00 Apr-04 Apr-99 Apr-02 Apr-05 Apr-98 Apr-03 3Month Treasury Bill - - - 5Yr Treasury Rate 10YrTreasury Rate . 30YrTreasury Rate Source: Federal Reserve Bank of St. LouisExhibit 3 INFORMATION ON EIS COMMON STOCK Moore's research disclosed the following earnings per share and dividends paid per EIS share for the previous 10 years. Year EPS Dividends 1997 $1.36 $0.50 1998 1.29 0.50 1999 1.27 0.50 2000 1.33 0.50 2001 1.35 0.50 2002 1.50 0.55 2003 1.75 0.75 2004 2.10 0.90 2005 2.60 0.95 2006 2.71E* 0.95E '5 means expected for the year Alphamax Investors' Advisory Service issued a \"buy\" recommendation for E18 stock to its clients. According to the analyst's report, the EIS beta coefcient was 1.25. In September 2006, E13 was heavily traded on a national exchange within the range of $13 52'8 to $14 3.8 per share. Moore knew that at the end of 1996 the price of the stock had dropped to $7.00 per share. Exhibit 4 M-E-M-O-R-A-N-D-U-M To: Eloise Moore From: Bob Studz, Vice president, data processing Re: Estimated Savings for Pathrite System Date: September 1, 2006 As promised, I'm sending you the bottom line of the savings before tax and depreciation that I think we can realize if we purchase the new equipment. As I mentioned, I believe that we can use the new equipment to our competitive advantage. It is impossible to determine precisely how much the system will improve prots, but I think the improvement will be substantial. Can we get together to review the project before I present the gures to Seattle? I would really appreciate your opinion. My staff estimates net operating savings (before depreciation and taxes) for each year to be roughly $2.5 million. Actual savings could range from 30 percent higher (probability 0.2) to 15 per cent lower (probability 0.1) than this forecast. The current equipment has already been fully depreciated, and now has a zero book value. I also sense that the current market value of the old equipment is virtually nil. This is surprising, inasmuch as I'm sure that it would continue to meet our present needs for another six years at the very least. Given the rate of technological change, I expect that the Pathrite equipment will not have any market value either when it is ultimately replaced. We should assume that its operating life will equal its depreciation life, six years. I hope you don't mind my sending this to you just before Labor Day. I knew you would want to look at the numbers before I retum from the Coast the rst week of October. I would like to send your analysis to Seattle so that the Pathrite purchase can be included in our capital expenditure budget. If approved, we could pay MCC upon delivery because we are generating more cash this year than initially expected. Our accoLmtants believe that early payment would facilitate the taking of depreciation for tax purposes in the year of delivery

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance