Answered step by step

Verified Expert Solution

Question

1 Approved Answer

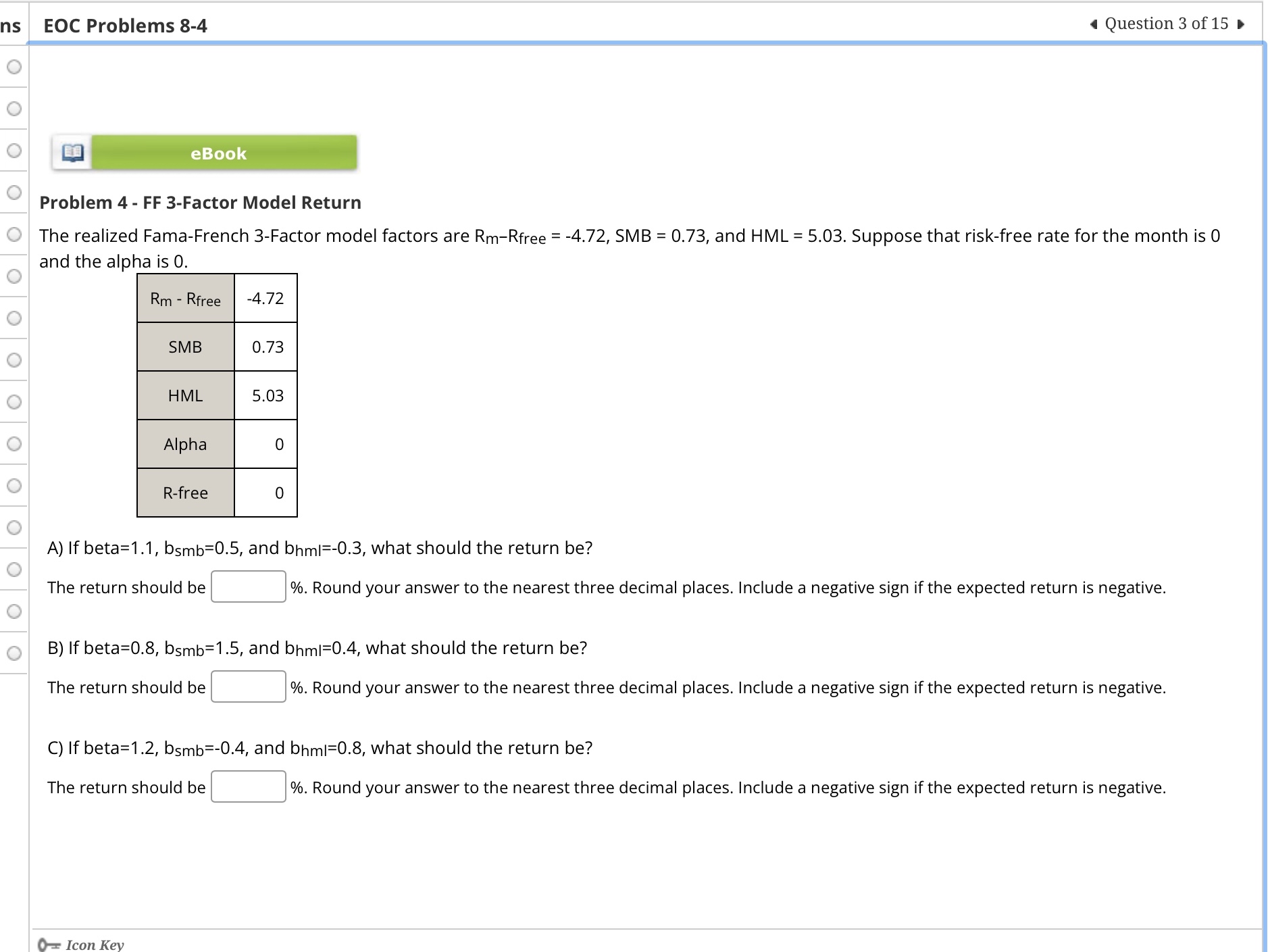

EOC Problems 8 - 4 Question 3 of 1 5 eBook Problem 4 - FF 3 - Factor Model Return The realized Fama - French

EOC Problems

Question of

eBook

Problem FF Factor Model Return

The realized FamaFrench Factor model factors are and Suppose that riskfree rate for the month is and the alpha is

table Rfree,HMLAlphaRfree,

A If beta and what should the return be

The return should be Round your answer to the nearest three decimal places. Include a negative sign if the expected return is negative.

B If beta and what should the return be

The return should be

Round your answer to the nearest three decimal places. Include a negative sign if the expected return is negative.

C If beta and what should the return be

The return should be

Round your answer to the nearest three decimal places. Include a negative sign if the expected return is negative.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The International Handbook Of Public Financial Management

Authors: Richard Allen, Richard Hemming, B. Potter

1st Edition

1137574895, 978-1137574893