Answered step by step

Verified Expert Solution

Question

1 Approved Answer

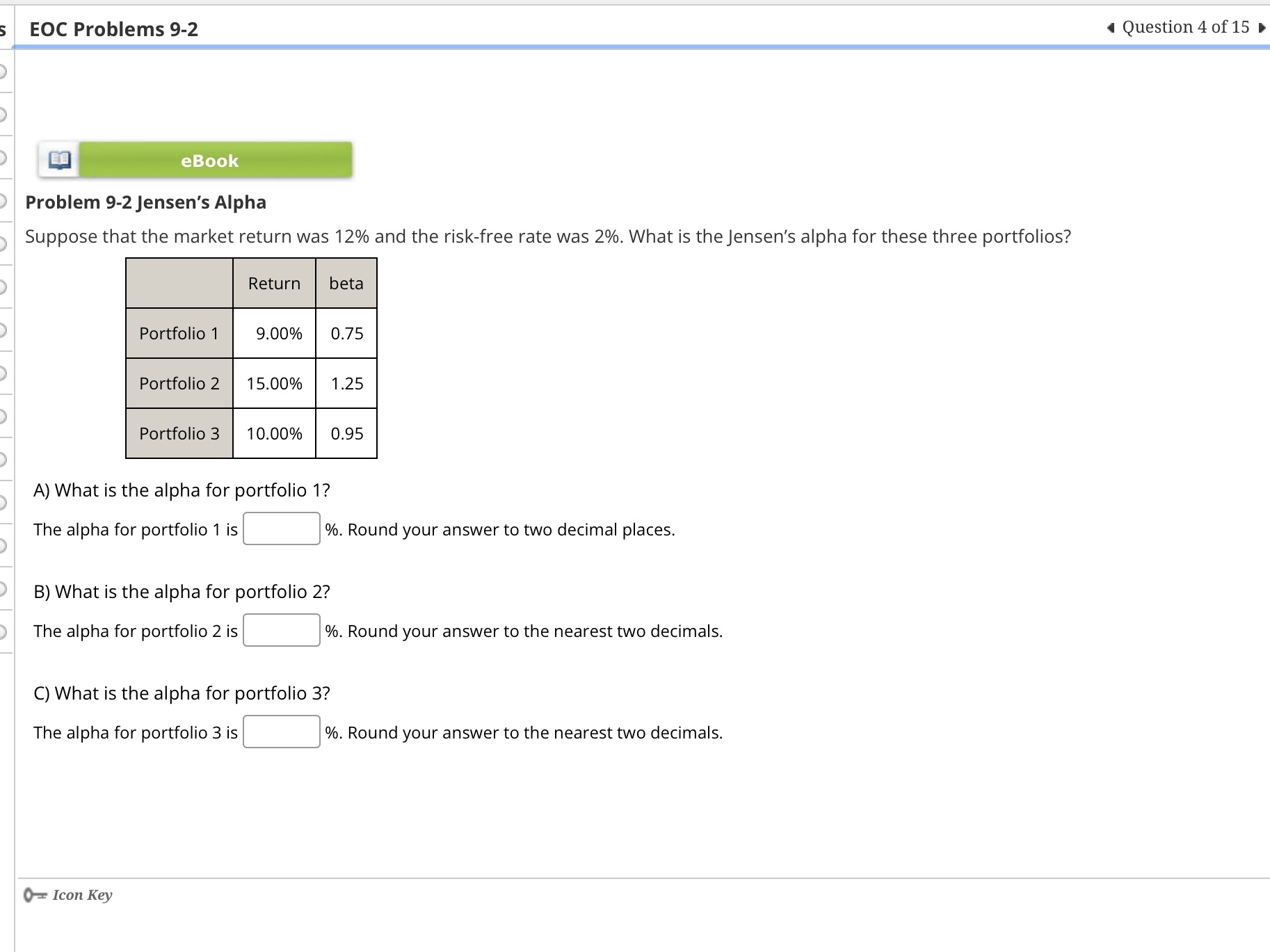

EOC Problems 9 - 2 Question 4 of 1 5 eBook Problem 9 - 2 Jensen's Alpha Suppose that the market return was 1 2

EOC Problems

Question of

eBook

Problem Jensen's Alpha

Suppose that the market return was and the riskfree rate was What is the Jensen's alpha for these three portfolios?

tableReturn,betaPortfolio Portfolio Portfolio

A What is the alpha for portfolio

The alpha for portfolio is Round your answer to two decimal places.

B What is the alpha for portfolio

The alpha for portfolio is Round your answer to the nearest two decimals.

C What is the alpha for portfolio

The alpha for portfolio is Round your answer to the nearest two decimals.

Icon Key

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Computational Intelligence In Economics And Finance Volume II

Authors: Paul P. Wang, Tzu-Wen Kuo

2007th Edition

3540728201, 978-3540728207