Answered step by step

Verified Expert Solution

Question

1 Approved Answer

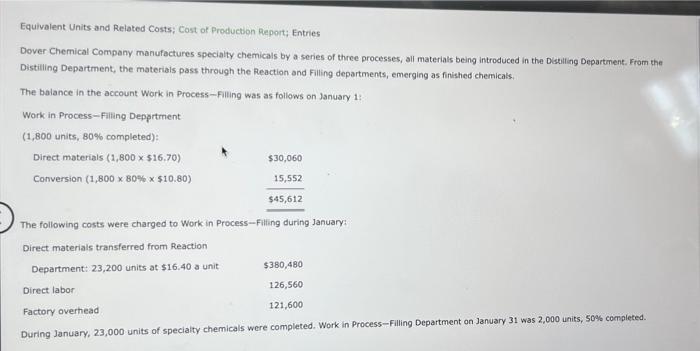

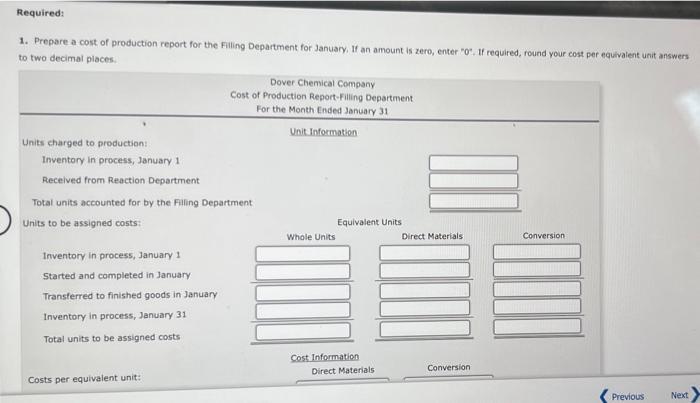

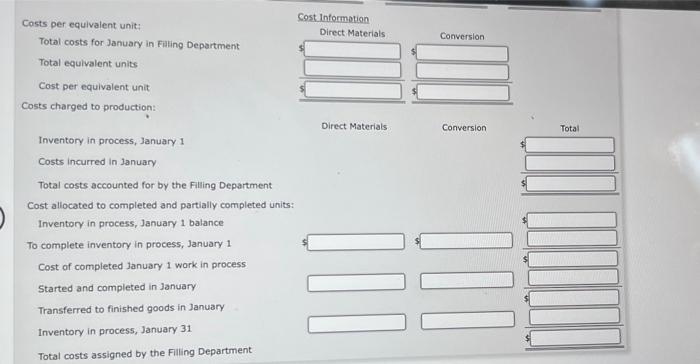

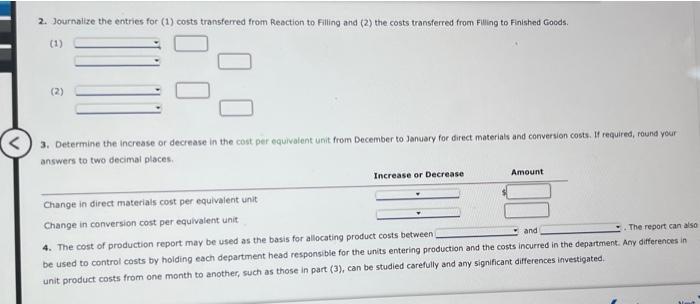

Equivalent Units and Related Costs; Cost of Productbon Report; Entries Dover Chemical Company manufactures specialty chemicals by a series of three processes, all materials being

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Leadership Style At PT Tekstil Bandung A Management Audit Investigation Following The Prolonged Economic Slowdown In Indonesia

Authors: Samuel P.D. Anantadjaya, Irma M. Nawangwulan

1st Edition

3659328979, 978-3659328978