Answered step by step

Verified Expert Solution

Question

1 Approved Answer

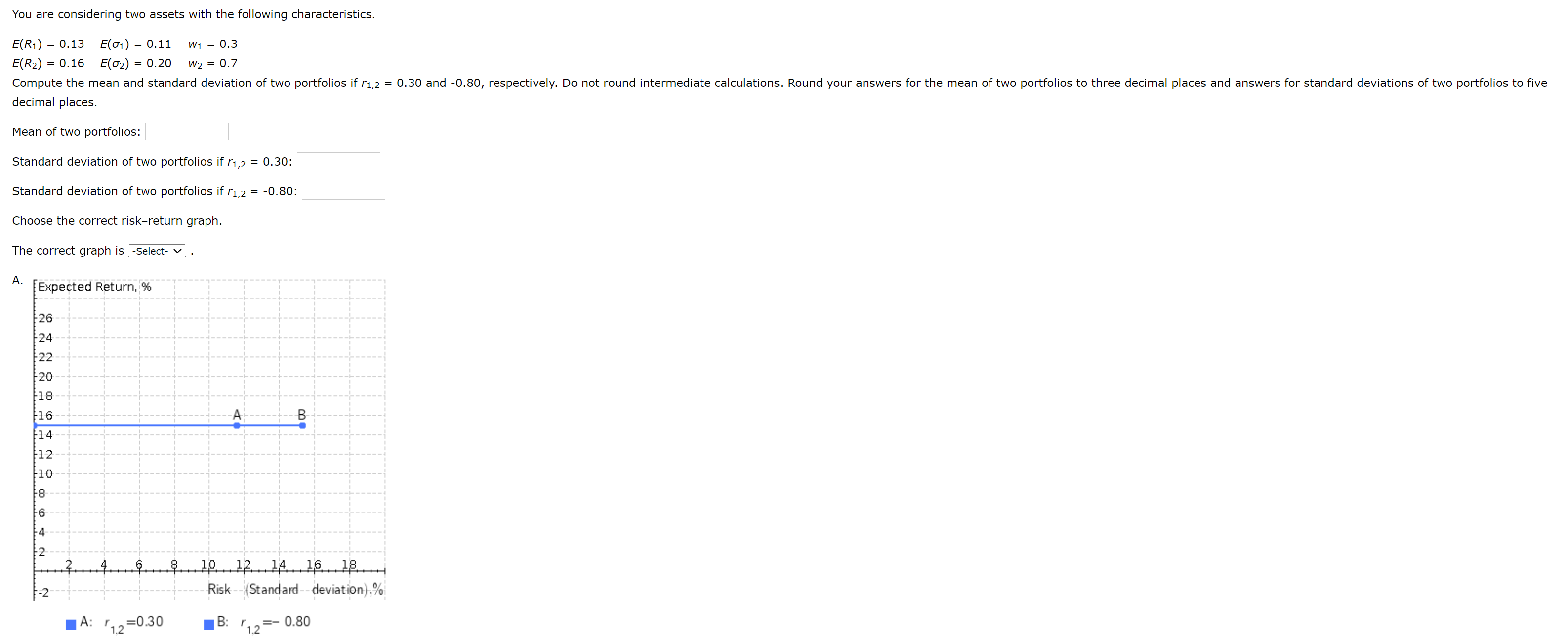

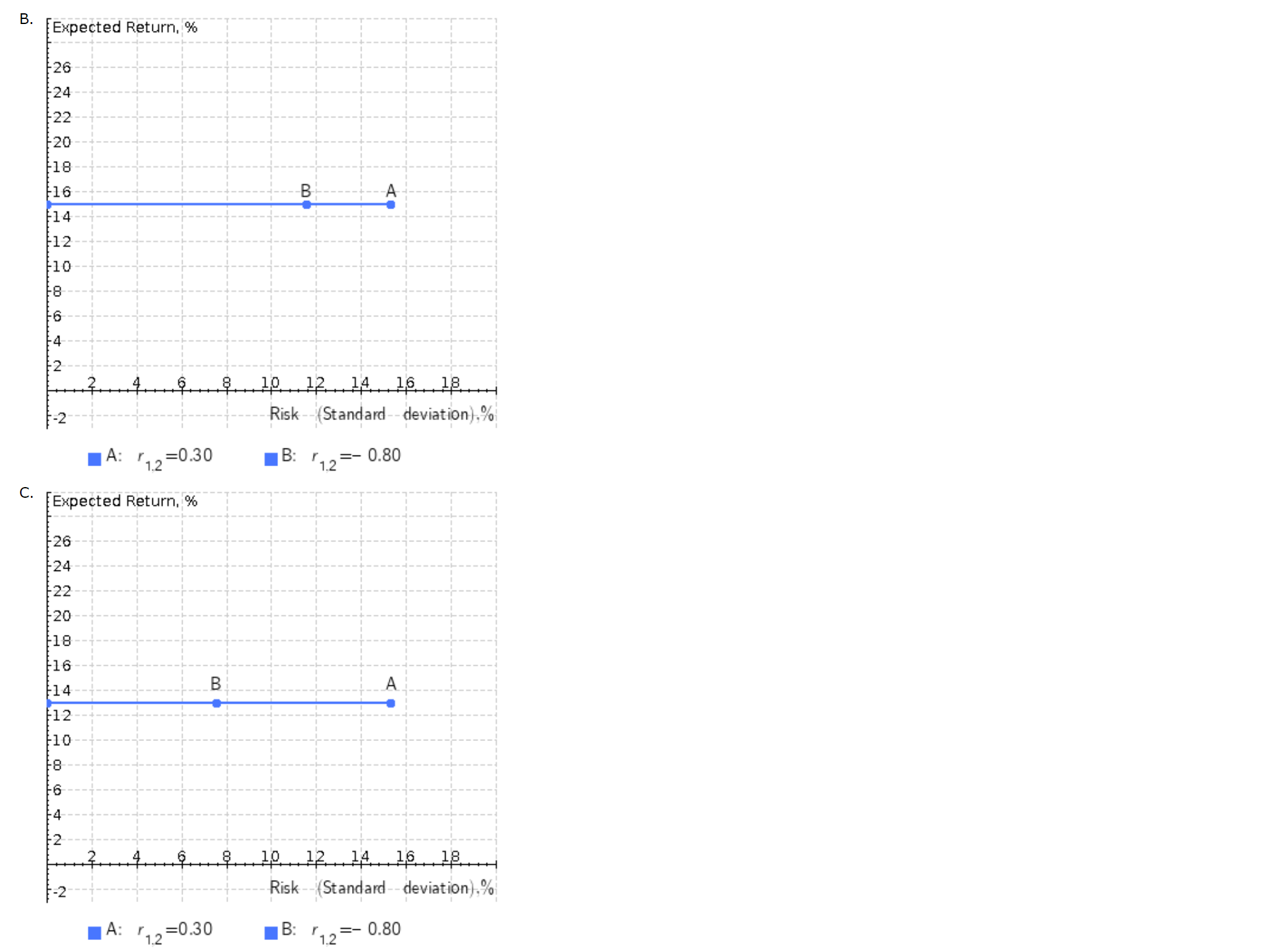

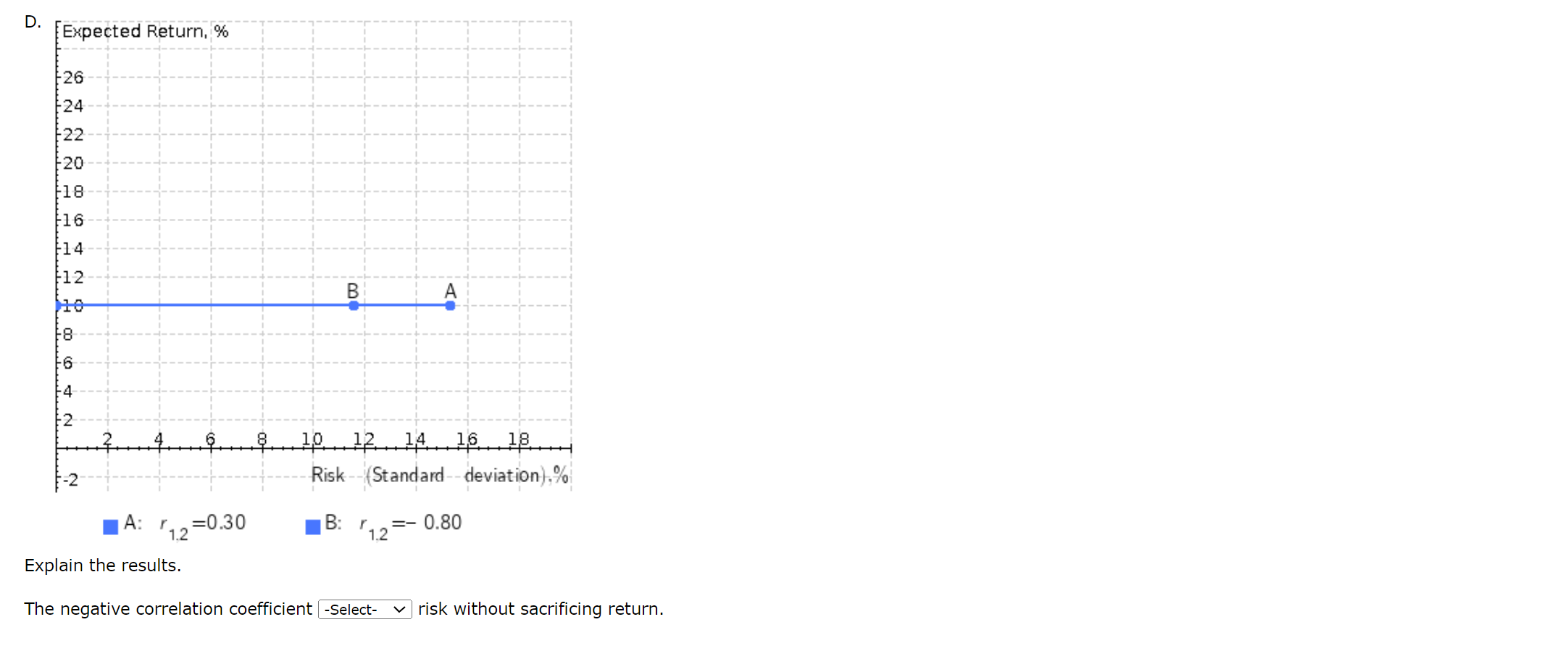

E(R1)=0.13E(R2)=0.16E(1)=0.11E(2)=0.20w1=0.3w2=0.7 decimal places. Mean of two portfolios: Standard deviation of two portfolios if r1,2=0.30 : Standard deviation of two portfolios if r1,2=0.80 : Choose the

E(R1)=0.13E(R2)=0.16E(1)=0.11E(2)=0.20w1=0.3w2=0.7 decimal places. Mean of two portfolios: Standard deviation of two portfolios if r1,2=0.30 : Standard deviation of two portfolios if r1,2=0.80 : Choose the correct risk-return graph. r1.2=0.30 B: r1.2=0.80 Explain the results. The negative correlation coefficient - Select- risk without sacrificing return. E(R1)=0.13E(R2)=0.16E(1)=0.11E(2)=0.20w1=0.3w2=0.7 decimal places. Mean of two portfolios: Standard deviation of two portfolios if r1,2=0.30 : Standard deviation of two portfolios if r1,2=0.80 : Choose the correct risk-return graph. r1.2=0.30 B: r1.2=0.80 Explain the results. The negative correlation coefficient - Select- risk without sacrificing return

E(R1)=0.13E(R2)=0.16E(1)=0.11E(2)=0.20w1=0.3w2=0.7 decimal places. Mean of two portfolios: Standard deviation of two portfolios if r1,2=0.30 : Standard deviation of two portfolios if r1,2=0.80 : Choose the correct risk-return graph. r1.2=0.30 B: r1.2=0.80 Explain the results. The negative correlation coefficient - Select- risk without sacrificing return. E(R1)=0.13E(R2)=0.16E(1)=0.11E(2)=0.20w1=0.3w2=0.7 decimal places. Mean of two portfolios: Standard deviation of two portfolios if r1,2=0.30 : Standard deviation of two portfolios if r1,2=0.80 : Choose the correct risk-return graph. r1.2=0.30 B: r1.2=0.80 Explain the results. The negative correlation coefficient - Select- risk without sacrificing return Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Affordable Housing Finance

Authors: K. Hawtrey

2009th Edition

0230555187, 978-0230555181