Answered step by step

Verified Expert Solution

Question

1 Approved Answer

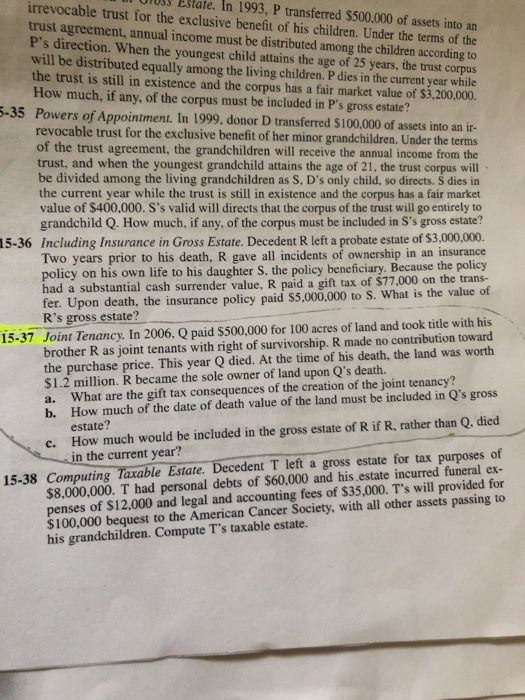

Estate. In 1993, P transferred $500,000 of assets into an irrevocable trust for the exclusive benefit of his children. Under the terms of the trust

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Comprehensive Audits Of Radiotherapy Practices A Tool For Quality Improvement, Quality Assurance Team For Radiation Oncology

Authors: International Atomic Energy Agency

1st Edition

9201037074, 978-9201037077